Weekly Roundup, 18th November 2016

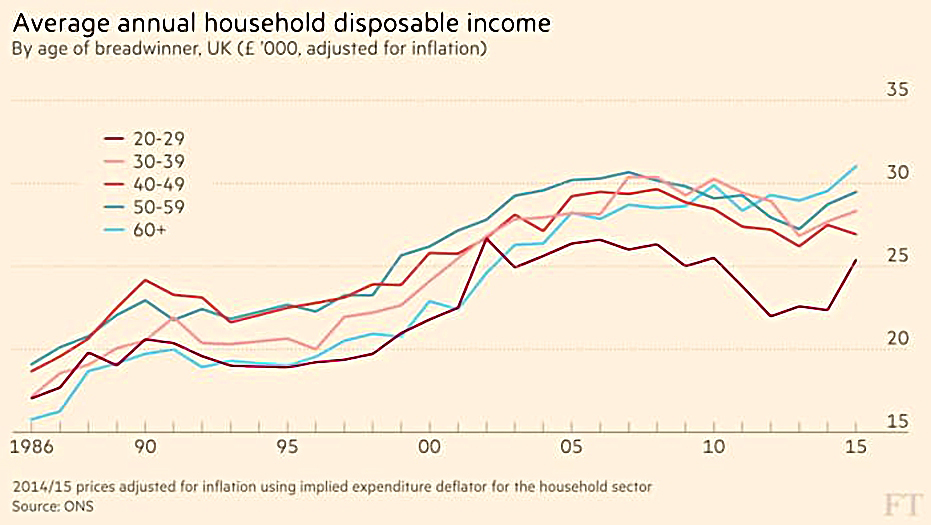

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about the distribution of household disposable income by age.

Household income

Lydia Ellis (( I couldn’t find a picture )) looked at ONS data on disposable income by age over the last 30 years.

- This means after-tax income, but before housing costs.

The focus (and headline) of the article was as usual the terrible plight of the millennials, although things didn’t look that bad to me.

Since the chart covers 30 years of data, we aren’t following particular generations through time, but rather looking at a series of snapshots of how people of particular ages were doing.

- The millennials are the current 20 – 29 age group, which has never had much money.

- Back in the 1980s they had more money than people over 60, but less than everyone else.

- Occasionally they overtake people in their 30s, but rarely.

Disposable incomes have risen for all – for example a 20-something household had disposable income of £17K, but now they have more than £25K (inflation-adjusted).

All that has happened over the past 30 years is that oldies have moved from the bottom of the pile to the top, for several reasons:

- the state pension has been restored to its former “glory” (it’s still less than a third of average earnings, and barely half the new minimum wage) after falling way behind wages in the 1980s

- many oldies (though not as many as people think) have the “gold-plated” DB company or public sector pensions

- old people have paid off their mortgages (though low interest rates limit the impact of this)

- many young people have large student loan debts

LISA

The FT put a panel together to chat about the Lifetime ISA (LISA).

Chaired by Josephine Cumbo, it included three familiar faces:

- Ros Altman

- Michael Johnson

- and Tom McPhail.

The new face was Iona Bain, who runs the YoungMoney blog (also known as Y Money Y).

- Sadly I didn’t receive the call myself – maybe next time.

Michael is the guy behind the LISA, and is not a fan of pensions (partly because the kids aren’t fans either).

- He wants to “reframe the language” so that Generation Y will participate.

- He also wants to redistribute the government’s contribution (currently tax relief, but in the LISA, a bonus) from the richest 15% in income terms.

Ros is anti-LISA, worrying that it it will deflect savings from workplace pensions.

- She’s also worried about mis-selling, with people opting out of workplace pensions or giving up higher-rate tax-relief in a SIPP to fund a LISA instead.

- She also thinks that most people who open a LISA will be funded by rich parents, so Michael’s redistribution target won’t be achieved.

Tom thinks that ISAs are too complicated, and should be merged into one “Super ISA”.

- He would like to see the current tax-relief system replaced with a flat tax rate for all.

- He also thinks that building more houses would be a better way to get young people on the housing ladder.

Iona seems to agree with Michael that the LISA will appeal to the young, but is worried that it might be scrapped in future.

- Given that she links this to a Corbyn-led Labour government, I don’t think we need to worry about that in the short-term.

- Tax-relief doesn’t incentivise millennials as (i) they don’t feel they are paying too much tax, and (ii) they don’t have any more money to save.

- So a “bonus” approach – as in the LISA – could possibly work better (at least on the first point – I’m not clear how it addresses the second point).

- Iona is also concerned about confusion between the LISA and both workplace auto-enrolment and the Buy-To-Let ISA (which is being replace by the LISA).

My own view is closer to those of Ros and Tom than Michael and Iona:

- there are already too many savings options – the SIPP and the ISA are enough

- the LISA offers no advantages to anyone not planning to buy a house, and calling it “Lifetime” is misleading

- age-defined schemes are unfair, and Michael’s idea that reframing the language will persuade people to save is wishful thinking – saving isn’t suddenly going to become “cool” or “fleek”.

I think the LISA was a plan from George Osborne to further support the housing market, and it will be interesting to see what Philip Hammond makes of it in his Autumn Statement later this month.

- I can see flat rate pensions tax relief being introduced, but he will probably leave the LISA alone, or perhaps raise the annual contribution limit and / or the property price limit slightly.

AIM red flags

Over at MoneyWeek, Chris Boxall – who manages Fundamental Asset Management’s Aim service – listed ten red flags for AIM investors, using just two companies as examples:

- Superglass, an insulation manufacturer, and

- Stanley Gibbons, the stamps and coins group (( Which I was dozy enough to buy myself for the SmallCap AIM portfolio ))

First Superglass:

- IPO from private equity – these guys know when to sell, and they usually maximise their own profits, leaving little if anything for private investors in the IPO

- high debt – Superglass had £30M of debt against £1.6M of net assets, which is gearing of more than 15 times

- government incentives – Superglasses returns depended on government subsidies to reduce CO2 emissions, and these never last forever

- high profit margins (without a moat) – the strong growth and high margins attracted competitors who drove down prices

- underinvestment – high debts meant that most of the cashflow went to paying lenders

- from 2008 to 2010, £18.2M of plant was written down, but only £4.2 of new plant was bought, with £13.6M going to debt repayment

- move down from main market – Superglass originally listed on the main market, but a move downstairs won’t usually revive the fortunes of a struggling company

Six years after floating at 180p, Superglass was taken over at 5.6p.

Now for Stanley Gibbons (SG):

- changing business model – SG switched from being a broker that facilitated trading in collectibles to carrying its own inventory

- growing inventory – from 2009 to 2015, inventory grew from £9M to £54M, and debt ballooned

- lots of cash tied up in slow moving collectibles that are hard to value properly is a disaster waiting to happen

- negative cash flow – while revenues increases and SG was profitable until last year, it had several years of negative cash flow, indicating trouble was around the corner

- weak online offering – SG’s website took a long time to build, and was expensive; with a better website more of the inventory could have been shifted sooner, boosting cash flow and delaying or even avoiding problems.

AIM shrinking

Sticking with AIM, Katherine Denham over at FT Adviser reported that the AIM market is shrinking as more small firms choose crowdfunding instead of a listing.

- The market cap of the market is down to £81 bn in October, from £83 bn in September, which is not that much of a drop.

- The number of listings is down to 995, below 1,000 for the first time in 12 years.

Crowdfunding is cheaper and quicker for firms that only need to raise a small amount of money

- but the high valuations typically found in crowdfunding – plus the high risk of later dilution – mean that it’s not necessarily such a good deal for the investors.

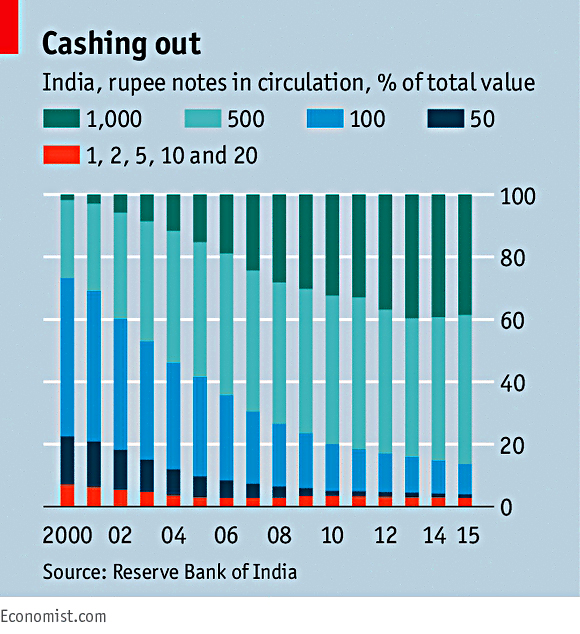

Indian banknotes

Finally, the Economist reported on the surprise decision by the Indian government to withdraw the country’s two highest denomination banknotes – worth 500 and 1,000 rupees (around £6 and £12) – with almost immediate effect.

- These two notes account for 86% of the value of currency in circulation, and for 22 bn pieces of paper.

- The announcement came with a new bank holiday and a three-day ATM-shutdown.

There were two objectives:

- to remove counterfeit notes (widely believed to be printed in Pakistan and dumped in India)

- to curb the black economy (known locally as “black money”), estimated at between 20% and 33% of total output

- notes are widely used in purchases of property and gold and even two-thirds of Amazon sales in India are cash on delivery

The notes will be replaced by new Rs500 and Rs2000 notes, so it’s not a direct attempt to push people towards electronic money.

- But notes have to be traded in by the end of the year, with a daily limit of Rs4,000 at present.

- People will need to explain how they came by them if they have more than Rs250,000.

- People are already buying Rs1000 notes at big discounts to launder through small savers.

The change should help banks, which will probably end up with higher deposits, but could dent property prices, and hence the collateral that banks lend against.

- It will also lead to delays in purchases of big-ticket items like white goods and motorbikes.

- This will reduce GDP growth in the short-term (three to six months), but may have little long-term effect.

I hope this is one announcement we can rule out from the Autumn Statement.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.