Weekly Roundup, 12th February 2019

We begin today’s Weekly Roundup in the FT, with Tim Harford. This week he was defending inflation.

Contents

Inflation

Tim wasn’t defending hyperinflation, which is relatively uncommon, but he thinks that low-level inflation can prevent the economic equivalent of a heart attack.

Hyperinflation does not strike at random, but must be manufactured by the relentless printing of money, generally as the last resort in the face of political dysfunction alongside a severe fiscal crisis.

If it ever does happen [in an advanced economy], it will be only one element in a far more comprehensive economic disaster.

Tim note that readers who complained about his recent defence of central banks were worried about the typical 2% inflation target, which will have the value of money in 36 years.

As we have seen previously, money has three functions:

- medium of exchange,

- stable unit of account, and

- store of value,

Low-level inflation has a limited impact on the first two functions, but will affect the third over time.

- That’s why cash is a bad long-term asset, and why indexed annuities are so much more expensive.

But a well-diversified portfolio should keep up with inflation.

Tim suggests that the inflation target provides the room to stimulate the economy in a recession (through interest rate cuts).

- But the experience of the last 10 years suggests this isn’t true anymore, with only the US have rates above the 2% target.

Perhaps we need a 4% inflation target.

Small cap ESG

Merryn Somerset Webb looked at how Generation Z reformers can best change finance along ESG principles.

Not that long ago we all assumed that if you wanted to change the structural make-up of society or economy you did so by influencing public policy one way or another.

Now you get the same sense everywhere: that the world’s problems can be solved, in fact should be solved, by corporates and the people running them rather than governments.

Merryn is worried by rising corporate concentration (monopolies and duopolies) and corporate control over public policy (via donations and lobbying).

- The effects are rising inequality and slowing productivity growth, according to a new report.

Once companies get so much larger than their competitors that it is hard for the latter to see how the gap can be closed, “the industry enters a ‘monopolistic region’ in which the follower does not invest due to a ‘discouragement effect’.”

After that you can get to a point where “even the leader stops investing in productivity enhancement as the perceived threat of being overtaken becomes too small”.

Merryn suggests that the youngers get back into public policy work, or that they join small companies with the potential to be disrupters.

- She also notes that the things we like as investors – barriers to entry, pricing power – don’t fit with this social justice agenda.

SJWs might prefer to invest in small caps.

- She suggests the Henderson Smaller Companies Investment Trust (HSL) which is trading on an 8% discount to NAV.

Redwood fund

John Redwood had another of his regular updates on the ETF fund he runs for the FT.

- There’s no table of holdings included with the article (which is unusual).

John says that some of the 15% cash he held at the turn of the year has been invested into China and Germany, countries he had previously sold out of on trade concerns.

- He also bought more tech after the 4Q18 sell-off.

He’s still worried about the prospects for German exports, but sees the EU budget deal with Italy as positive.

- There wa also a sell-off of German stocks following poor third-quarter GDP figures, which means that reflationary measures are now back on the agenda.

The Chinese purchase follows big stock market falls since the 2015 peak, tax cuts and increased infrastructure loans to local authorities.

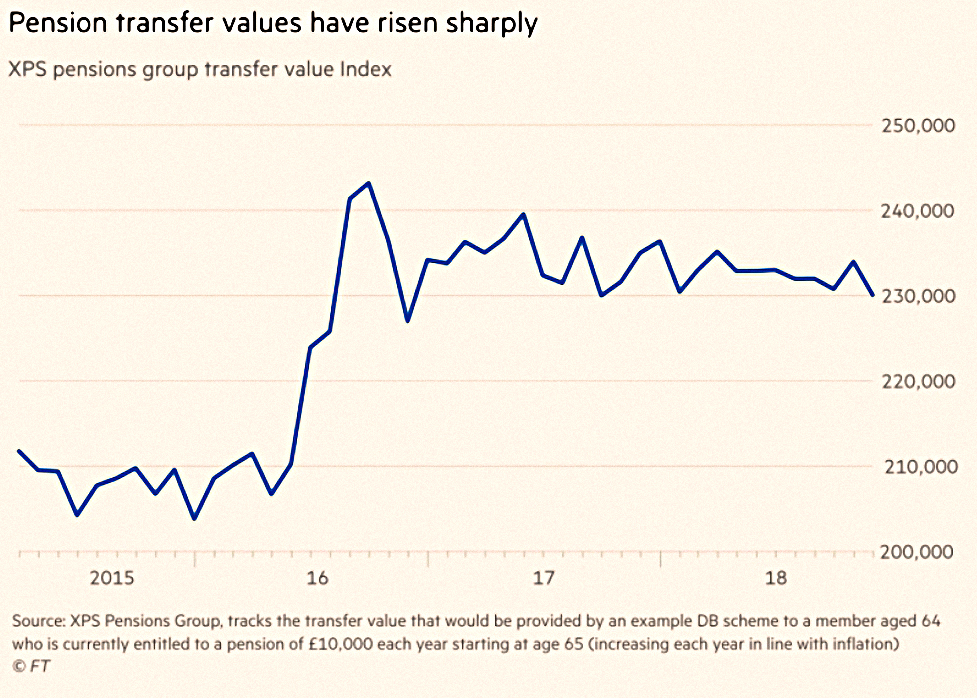

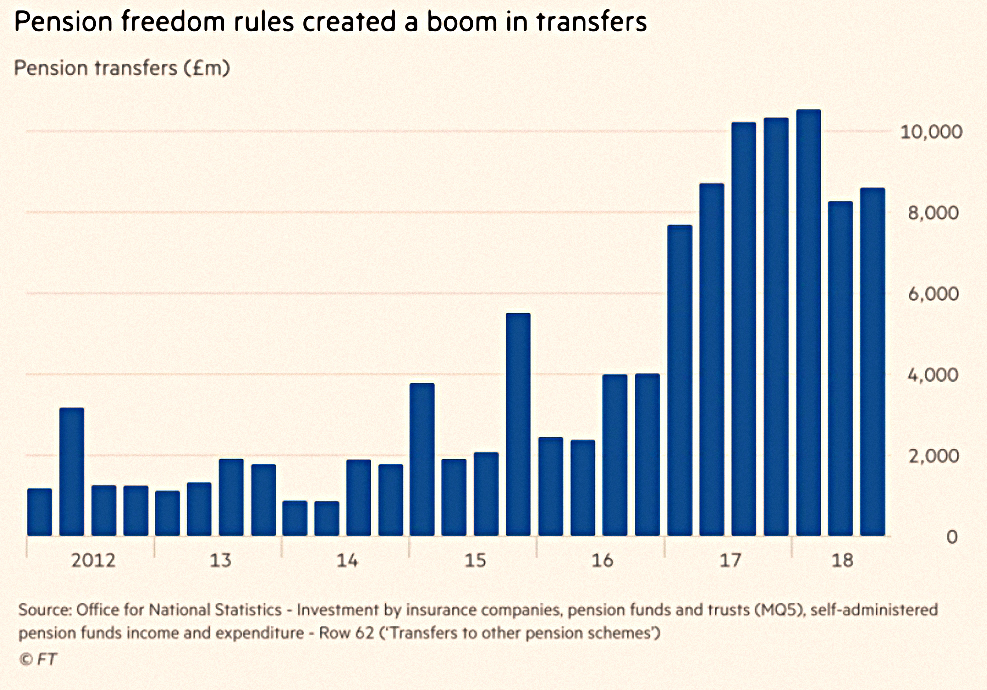

Pension freedoms

The FT had a bit of a scare story about the pension freedoms, and the 500K pensioners who have taken advantage – myself included – since April 2015.

- Kate Beioley cited the marshmallow test of deferred gratification, the implication being than anyone who “cashed in” their DB pensions has no self-control.

She notes the very transfer values on offer, but then says that many will have shifted money into stocks before a “sharp decline” in markets.

There are a few things wrong with this picture:

- Moving a DB pension into a DC pension is not cashing-in.

- Taking a good price on offer for one of your existing assets says nothing about your ability to defer gratification.

- Most stock indices are well up on their April 2015 valuations.

- Nobody has to invest 100% into stocks, and nor should they.

Pension assumptions

Sticking with pensions, The Economist reminded us that public pension plans in America are still making over-optimistic assumptions.

- They are also taking more risk, with 72% in risky assets (equities and hedge funds) compared to 62% of private pension portfolios.

Private plans are legally required to use a bond-yield as their discount rate in adequacy calculations, but public-sector schemes can use the expected rate of return on their investments.

- This provides an obvious temptation to exaggerate likely returns, and indeed, the average rate of return assumed by public plans is 7.4% pa.

This feeds back into their riskier asset allocation, but more importantly, allows them to minimise current contributions (since it appears that the schemes are more adequately funded than they really are).

- But even using their own accounting, the average deficit was 28% in 2017.

And poor returns in 2018 will only have made things worse.

Green New Deal

The Economist also looked at the Green New Deal (GND) a plan to tackle climate change from the bizarrely popular Democratic Congresswoman Alexandria Ocasio-Cortez (AOC).

The ambitious scheme will apparently not simply reduce CO2 emissions to zero (in ten years rather than thirty), but also:

- provide universal health care

- initiate a universal basic income

- protect workers from the impact of globalisation

- provide a job guarantee

The paper finally presented is a vague, low-tech, anti-capitalist measure (plant trees, reduce agriculture to family-sized farms) – which makes it also inefficient and resource-intensive.

The American people are promised “high-quality health care; affordable, safe and adequate housing; economic security; and clean water, clean air, healthy and affordable food, and access to nature”, “a job with a family-sustaining wage, adequate family and medical leave, paid vacations, and retirement security.”

This vision of American society is beautifully utopian. Yet each component of this paradise would require massive upheavals. Voters deserve a bit more explanation on how to get from here to there.

Noah Smith (@Noahpionion) tweeted his calculations that the GND would cost $6.6 trn per year (ignoring affordable housing and efficiency impacts).

- Thats 35 x the size of the Trump tax cuts.

- And 10 x the US’s military spend.

In fact, it’s more than one third of US GDP.

AOC is a fan of Modern Monetary Theory (MMT), a left-wing belief system that underpins closely related schemes like Corbyn’s “People’s QE”.

- So the GND would likely be funded by a massive deficit and spiralling debt.

- To be followed in due course by ballooning inflation and a loss of confidence in the dollar.

I think that we’ll have to come back to MMT in more detail at some point.

Factor returns

In a couple of articles from his Points of Return column on Bloomberg, John Authers looked at a report from Robeco Groep (a Dutch investment house) on asset returns since 1800.

As well as the assets themselves (stocks, bonds, currencies and commodities) they looked at six outperformance factors:

- momentum (winners vs losers)

- trend (absolute performance)

- value

- carry (high income / dividend)

- seasonality

- low vol (which they called “betting against the beta”)

This gives 24 asset/factor combinations, of which 19 proved to be effective over a two-century span.

- Trend following / momentum works best, which in turn implies that technical analysis hasmore to it than cynics would allow.

- Carry / high yield came second (remember though, that this is a negative skew factor)

- It some ways it’s a more successful version of a growth stock strategy.

- Seasonality also works – the summer is bad (and so is October) but Xmas and January are usually good.

- Low vol also works, at least in stocks.

- The opposite is true for bonds – riskier countries (even those which default the most) offer the best rewards.

The two competing explanations are rational risk avoidance, and behavioural weaknesses.

- The masses of risk events over the past two centuries don’t seem to affect the outperformance factors, and so the authors conclude that behavioural factors are the more likely explanation.

Quick links

I have a record-breaking nineteen links for you this week:

- Flirting with Models looked at Convexity & Premium in Trend

- The Economist wrote about what happens when your bitcoin banker dies

- And about the abdication of the bond king Bill Gross

- The FT looked at why the central bankers blinked

- Musing on Markets had part 7 of its data updates – on Debt

- And part 8 – on Dividends and Buybacks

- Enterprising Investor looked at Ensemble Active Management

- Alpha Architect looked at the Smart Money Indicator, which it described as a new risk management tool

- Cliff Assess looked for the intuition underlying multi-factor stock selection

- Portfolio Advisor reported on IFAs’ lack of basic investing knowledge

- CityWire said that a record £6 bn has been pulled from funds by nervous investors

- Wealth of Common Sense explained how to put 100% of your portfolio into the stock market

- The NY Times said that you need lots of stocks, whatever your age

- Then went further, saying that all of your nest egg should be in stocks

- Pragmatic Capitalism explained why banning stock buybacks is stupid

- And how the patient investor sees the world more clearly

- The Adventurous Investor explained that combining ESG and Value doesn’t work

- And Factor Research had the underlying paper – Can Value Investors Do Good?

- Finally, SSRN has the paper on Global Factor Premiums that John Authers was writing about.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.