Weekly Roundup, 1st Jan 2019

We begin today’s Weekly Roundup in the FT, with Merryn Somerset Webb, who was writing about Bitcoin.

Bitcoin

After a break last week for Xmas Day, this week’s roundup is a catch-up edition.

In the FT, Merryn wrote about bubbles, and Bitcoin in particular.

The bitcoin bubble has been one of the most perfect. An exciting new technology arrived. A few people in the know bought in. Prices started to rise.

Huge claims were made about how the world was on the verge of being disrupted.technology. A mania began. Prices went berserk, then parabolic, and finally collapsed.

She uses this parable to recommend a few books:

- Extraordinary Popular Delusions and the Madness of Crowds – Mackay

- Dot.con: The Greatest Story Ever Sold – Cassidy

- The Myth of Capitalism – Hearn and Tepper

- Farewell to the Horse – Raulff

- Silver Shoals: Five Fish That Made Britain – Rangeley-Wilson

- Investment Trusts Handbook 2019 – Davis

I have read only the first, but will get to the last in the new year.

- My coverage of the 2018 edition is here.

Merryn points out that the internet did indeed eventually disrupt incumbent businesses (principally retail and media).

- So bitcoin / blockchain might yet have some long-term impact on the payments system.

Fed balance sheet

Michael MacKenzie wrote about the shrinking Fed balance sheet, which appears – rather than interest rate rises – to be the red line for Fed chairman Jay Powell.

- In the same speech where he reduced expectations on the number of 2019 rate increases, he confirmed that the monthly $50 bn contraction was on “automatic pilot”.

The subsequent fall in value of riskier assets could feed on itself. Selling is begetting selling as falling equity and credit prices compel capitulation by investors.

The general suspicion is there is more to go, particularly should fund redemptions early next year force more selling of equities and credit.

There are two problems for markets:

- Contraction implies loss of liquidity.

- Sticking to contraction come what may contradicts the stated “data-driven” policy.

Quantitative Tightening (QT) has negative implications for US stocks and bonds, and the stocks lead over the rest of the world has already shrunk.

Michael expects the Fed to relent eventually, but we’ll have to wait for the next meeting of the Fed (in late Jan) to see how likely this is.

Round tables

The new year is a good time for round table predictions and recommendations, and both Merryn and Michael featured in the FT’s debate, chaired by Claer Barrett.

Also present were Chris Giles, the FT#’s economics editor:

Moira O’Neill from Interactive Investor:

And Richard Buxton, CEO of Merian Global Investors:

CG noted that:

For the past two years, the general end-of-year sentiment has been horribly wrong.

After the Brexit vote and Trump’s election in 2016, economists and investors were pretty fearful about 2017.

Then, at the end of 2017, everyone was really optimistic about 2018 .

So the big question is whether FOMO (as valuations become attractive) will be trumped by FOLM (fear of losing money).

- Is this a real bear market (technically, for some indices it already is) or is it a correction that will so be over?

MM and MSW both cited QT as a big change, and noted that a lot of people are holding more cash than ever.

- Brexit is obviously another big factor here in the UK, where the market looks cheap.

MSW said than in the event of a no-deal Brexit, the UK would cut rates and add more QE.

We can also expect a new PM next year (though whether Tory or Labour is not clear, and thy have very different investment implications).

MM said that asset managers were much more worried about Labour than Brexit:

They’re all trying to get their money offshore so it will not be subject to capital controls. But their biggest problem, of course, is high-end property.

MSW was worried about the AIM IHT exemption being revoked (she mentioned the current government as well as Corbyn, but they have already ruled it out), and also about increases in CGT provoking a stock-market sell-off.

MM, CG and RB thought that there could be one last chance to buy the dip.

You could argue that what we’re seeing is not an end of the cycle, but a slowing of the really fast growth part of the cycle [CG].

The main global worries are China turning from lender to borrower, which could push up the cost of borrowing, and downgrades of corporate bonds to below investment grade.

MoneyWeek also held a round table, which didn’t include Merryn.

- The theme was what to invest in as the bear market kicks in.

Attendees were:

- John Stepek (chair)

- Max King

- Charlie Morris

- Tim Price

- Jim Mellon

- Jim Leaviss from M&G. and

- Alastair Mundy from Temple Bar.

They tipped:

- Lloyds (LLOY)

- RBS (RBS)

- Barclays (BARC)

- Carnival (CCL)

- Tesco (TSCO)

And amongst the trusts:

- Capital Gearing (CGT)

- Personal Assets (PNL)

- Worldwide healthcare Trust (WWH)

- BB Healthcare (BBH)

- JP Morgan Emerging Markets (JMG)

- Temple Bar (TMPL)

- BlackRock Smaller Companies (BRSC)

- BlackRock Frontiers (BRFI)

- Global X Argentina ETF (0IWO)

- M&G Credit Income Trust (MGCI)

JM and MK also recommended a few of NASDAQ-listed biotech stocks, and some other US and Japanese stocks were also tipped.

L&G

There were a couple of interesting snippets in an article by Oliver Ralph about L&G’s attitude to social care.

A care home can cost £1K per week, and the number of over-85s is expected to double over the next 23 years.

- But L&G don’t think that the problem can be fixed with insurance.

CEO Nigel Wilson said:

We are evolving our business model to meet the problems of today but it won’t be a classic insurance product. We are not trying to create long-term care insurance, which has been tried in the US and failed.

L&G wants to move into “rental solutions” for older people, which would allow them to deplete their home equity.

- In 2017, the company bought two firms that specialise in retirement villages.

I get how this fits into the firm’s strategic move towards “build to rent”, which in turn is the logical end-game of the government’s squeeze on small-scale buy-to-let landlords.

- But it only indirectly addresses how people will fund their own social care.

Those unlucky enough to need care, but lucky enough to have home equity after moving into one of L&G’s rentals can pay from that.

- But where’s the pooling of risk that insurance companies are supposed to provide?

Alternative assets

The FT had an article on how niche markets performed during 2018.

Amongst the things that had done well:

- Carbon credits

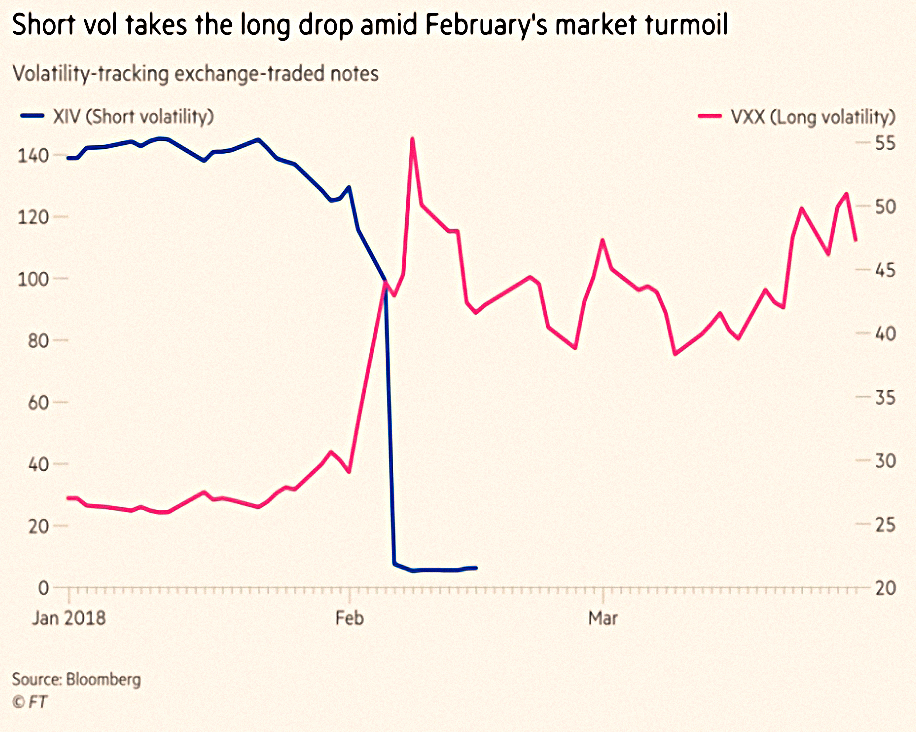

- Volatility (VIX)

- “Green” (environmental) bonds

- Burgundy wine

- Pot (cannabis) stocks

Things that have not done so well include:

- Catastrophe bonds

- Short volatility (XIV)

- Battery metal producers

- Ethanol biofuel licences (RINs)

In MoneyWeek, John Stepek had a similar article, based around the charts of the year.

He looked at

- Amazon

- Bitcoin

- Oil

- Gold

- The yield curve, and

- The US dollar index.

Unfortunately, I couldn’t find an online link to the charts in time for this post.

- But I’ll keep trying.

Quick links

I have four for you this week:

- UK Value Investor explained how to measure a company’s growth rate.

- And why free cash flows are important for dividend investors.

- Research Affiliates asked whether alternative risk premia are a crisis or an opportunity?

- And Flirting with Models asked what do portfolios and teacups have in common?

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Interesting in terms of alternative assets’ 2018 performance how diversification played its role- whilst the markets were down around the 10% mark, Infrastructure trusts ( despite Corbyn) were up around 5-10%, Gold was up 5% and Government Bonds up around 1% ( almost as good as cash but with more risk). Diversify or……