Weekly Roundup, 20th March 2023

We begin today’s Weekly Roundup with banks.

Banks

We’ve now had three banks “saved” in a couple of weeks.

- First SVB, then Signature, and now Credit Suisse (CS), which has been sold to UBS for CHF 0.50 per share (valuing CS at $3.25 bn).

Twenty-five years ago, UBS merged with Swiss Bank, which means that the latest deal leaves Switzerland with just one major bank.

- It’s also the largest financial institution collapse/takeover since the 2008 financial crisis.

The deal is underwritten by the Swiss government to the tune of CHF 9 bn, though UBS has to lose CHF 5 bn itself before this buffer is triggered.

SVB was brought down when bond yields went up (ie, bond prices fell).

- It had taken deposits from tech firms that were cash rich and invested them in long-term US Treasuries.

Interest rate hikes hit confidence in the tech sector and started outflows from SVB, forcing sales of the long-term assets at a loss.

CS has been brought down by an old-fashioned bank run, where depositors (personal and corporate) withdrew cash and investors sold CS shares.

Despite reasonable financial ratios and a big, diversified balance sheet, confidence in CS has been low for years.

- There have been a number of scandals including the collapses of Greensill Capital and the Archegos hedge fund.

More recently, the Saudi National Bank (CS’s largest investor) said it would not be investing more.

One interesting aspect of the CS deal is that the AT1 (Additional Tier 1) capital of CS is being wiped out.

- The major holders of these bonds (known as CoCos, or contingent convertible bonds) are believed to be in Asia, where the risk of contagion is now focused.

These AT1s sit higher in the capital structure than equity, but CS equity holders will receive a little money from the merger/takeover, which seems strange.

- CoCos can be written down/off if a lender’s capital ratios fall below a certain pre-determined level, but normally the equity would be worthless is such a situation.

Other types of CoCos can be converted into equity, but CS only has writedown CoCos.

Thus the CS deal has implications for existing AT1 capital/cocos in other European banks, and for the prospects of raising more of this type of funding in the future.

The track record of deals like this is mixed:

- Lloyd’s will regret having taken over Halifax Bank of Scotland, and Bank of America didn’t do well out of acquiring Merrill Lynch.

- The unforced merger of Citicorp and Travelers was also difficult.

- But JP Morgan did well from its acquisitions of Bear Stearns and Washington Mutual, and Wells Fargo prospered from taking over Wachovia.

The key issue around bailouts like this is moral hazard:

- Knowing that failure will lead to a rescue can easily encourage excessive risk taking.

Of course, CS’s shareholders and bondholders won’t feel like they’ve been bailed out right now.

- And the consequences of a major bank failure could be even worse.

In his Bloomberg newsletter, John Authers had an interesting take on the implications of the deal:

The number of big commercial or universal banks in any jurisdiction tends toward one. Banking is reaching the point where it can be called a natural monopoly, which economists define as a situation where the costs of adding a competitor would exceed the benefits.

in similar sectors (eg, water utilities) there is a lot of regulation.

The new UBS is nothing if not big. If we can tolerate banks of that size, it looks as though we have to tolerate a system in which governments have a much bigger role.

John notes that bank runs used to part of the system:

If we’re prepared to live without deposit insurance, then the system needs to be policed by depositors themselves, and bank runs become the crucial form of discipline. Banks will behave themselves because otherwise their depositors will pull out money en masse.

This was the arrangement in the 19th century, but we can’t go back:

With information flowing so fast and without a filter, via social media, and with internet banking enabling very swift movements of money out of an institution, such a system would now be unworkable.

Indeed, the smaller banks in the US are now asked for a move in the opposite direction:

A coalition of medium-sized banks has asked for the government to introduce deposit insurance on all their accounts for two years. (( In the US, insurance applied to accounts smaller then $250K ))

This is a step closer to bank nationalisation, but how else can bank runs be prevented nowadays?

Another angle on the situation is that the recent increases in interest rates from central banks have started to break things, raising the question of whether the hikes will continue.

- A 50 bps rise from the Fed was expected this week, but now we might get nothing.

Of course, a creaking banking sector means tighter financial conditions in any case, which means there is less of a need for the Fed to hike.

- The Bank of England will also hold a rate-setting meeting this week, and could also pause its sequence of hikes.

Inflation targets

Joachim Klement looked at the impact of central banks missing their inflation targets.

- Until recently, inflation has undershot expected inflation (as calculated from break-evens on Italian and German bonds).

This difference between implied and actual inflation impacts the amount of interest that governments pay on their bonds.

If a government issues new debt, it must pay interest that implicitly covers the expected inflation rate for the duration of the bond.

If inflation undershoots this expected inflation rate, the interest costs for the government are higher than if the central bank had managed to meet its inflation target. If the inflation rate overshoots, the government was able to borrow funds at a lower cost of debt than if the central banks had managed to meet its inflation target.

The more inflation undershoots, the bigger the government interest bill.

- The longer the maturity (or duration) of the bonds, the higher the bill also.

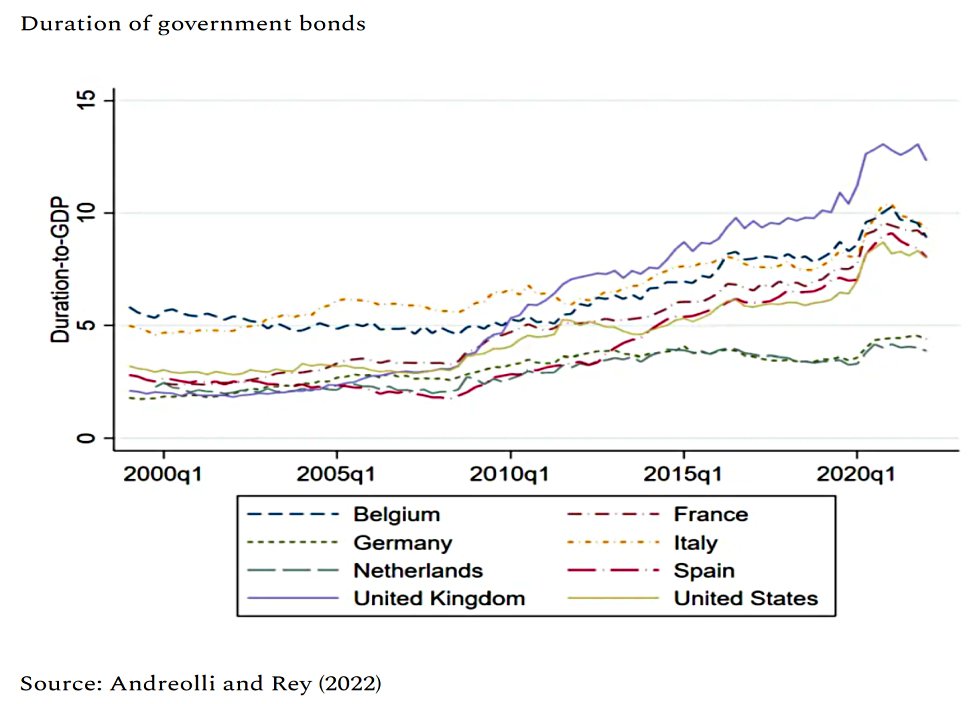

The UK has much longer duration bonds than most countries.

In early 2022 the duration of UK Gilts was 12.3 compared to 8.0 for the US and 4.4 for Germany. Italy boasts the highest duration in the Eurozone at 9.3.

This means that if the BoE undershoots its inflation target, the British government pays a particularly high price.

- The converse is also true – in 2021 and 2022, inflation has missed spectacularly to the upside, providing a much bigger windfall.

But as mentioned earlier, for most of recent history, inflation undershot.

Since 2002, the US government has paid 2.2% of GDP too much in interest to bondholders. The German government paid about 1.1% of its GDP too much over the same period. One can guess that the cost to the UK government was some 3-4% of GDP.

Adding back the savings from the last couple of years cuts the cost for the US and Germany to 0.6% of GDP.

LTA

For a couple of hours last week, I thought I was done writing about the LTA, which Jeremy Hunt kindly abolished in Wednesday’s budget.

- But Labour immediately promised to reinstate it if/when they win the next election, so I have to think about it once more.

In fact, Labour plans to provide an exemption for doctors only, so as a comment on my Budget commentary put it “all animals are equal, but some are more equal than others”.

My understanding is that pension contributions have legal protection as deferred pay, so although Labour is free to reinstate the penalty, they will find it more difficult to directly penalise any actions taken by savers in the interim.

- Some form of fixed protection will need to be offered.

On that note, it appears that the existing fixed protections (( Of which I have one flavour )) will no longer be voided by adding further contributions to your pension pot.

If Labour still look like winning in twelve or eighteen months from now, I would expect articles to appear detailing the best strategies to cope with the re-introduction.

- By that point, Labour’s position on the 25% tax-free lump sum should be clearer.

The worry is that in the absence of a clear strategy, people will max out their contributions in the next three tax years and then crystallise their pensions immediately before the election.

- Which is pretty much the opposite of what was intended by the abolition of the LTA.

Crypto

The Treasury has announced that a crypto section will be added to the self-assessment tax return from 2024-25, with aim of nudging taxpayers into declaring crypto gains.

- The timing coincides with the shrinking of the CGT allowance down to a paltry £3K pa.

Given the performance of crypto over the last year, it could be argued that the measure has come too late, and that there will be few crypto gains to declare.

Quick Links

I have four for you this week, the first three from The Economist:

- The Economist looked at What the loss of Silicon Valley Bank means for Silicon Valley

- And asked Is the global investment boom turning to bust?

- And noted that A battle royal is brewing over copyright and AI

- Alpha Architect analysed Research and Development, Expected Profitability, and Expected Returns

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Footnote 2 is interesting!

Does this mean you could (in theory at least) add 3*40k +60k ie 180k in the next tax year OR are their some further wrinkle(s) around carry forward?

I think that the amnesty doesn’t begin until the LTA is abolished on 6th April. So 60 + 2*40 for 23/24 and then another 60 in 24/25 (total of 200K before the election)? You need to be earning that much as well, though – don’t you?

Thanks.

Take your point re earnings.

I assume the above only applies if you have not already flexibly accessed your pension. If you have flexibly accessed your pension then the MPAA (now £10k again) applies – and in this scenario could you use carry forward (albeit of £4k PA) too?

I would assume so. The tweet I saw only said that from April, new contributions won’t void existing protection limits. Though I’m not really clear in what sense the limits exist if the LTA penalty (and then later the LTA itself) is abolished.

I would have thought that if Labour get in we start again from scratch with a new protection system, but it seems that pensions are different and some kind of grandfathering will apply.

And presumably if you have accessed it and not been working then the non-earners limit (AFAICT unchanged by Hunt) applies?

Some more details re protection limits at:

https://www.ftadviser.com/pensions/2023/03/17/budget-reprieve-for-clients-with-lifetime-allowance-protection/