Weekly Roundup, 29th November 2016

We begin today’s weekly roundup in the FT, with the Chart That Tells A Story. This week it was about the UK’s housing shortage.

Housing shortage

Gemma Tetlow looked at ONS data on changes in housing stock and population in England, and four locations within it – Sunderland, Newham, York and the Isles of Scilly.

- This was census data, comparing 2011 with 2001.

England as a whole did okay, with 7% population growth and 8% more houses.

- But there was a lot of variation around the country.

Newham’s population grew by 25%, while new homes grew by just 10%.

- It was a similar – though less extreme – story across lots of London.

- Up in Sunderland, the population fell by 3%, while the number of houses went up by 3%.

Overall, owner-occupation is declining, falling from 71% in 2003 to 64% by 2014.

- This is because younger first-time buyers can no longer afford the high asking prices.

- The situation is made worse by tighter lending regulations, and by the low growth in wages for young people since the 2008 financial crisis.

Building more houses is the key to sorting out the UK housing market, but they need to be in the right places.

- We need to build around London, with good transport links into the city.

- And we need to link the Northern cities (Liverpool, Manchester, Leeds, Sheffield) and unlock the cheaper housing stock we already have up there.

Trump

It was another thin week for financial news in the aftermath of the Autumn Statement (which we covered here), and so I am forced to return to the subject of Trump more quickly than expected.

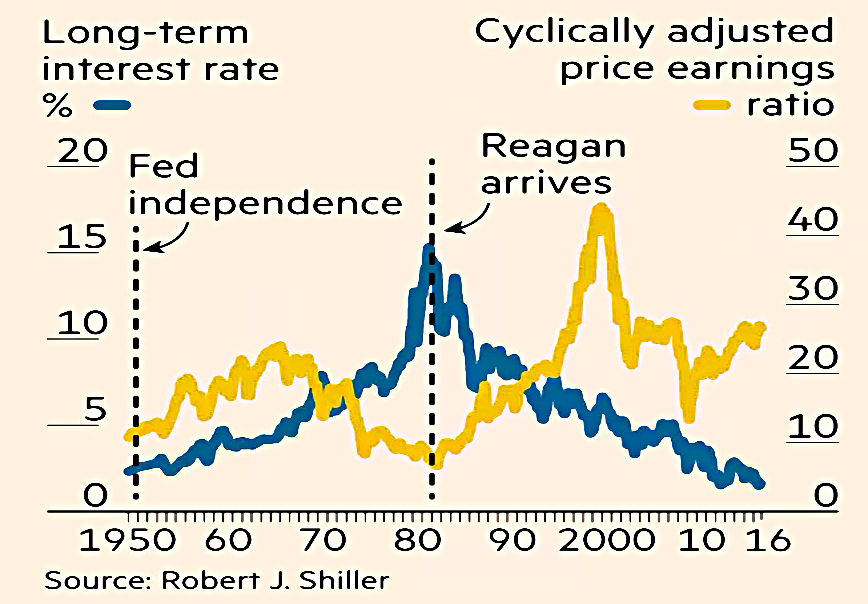

In the FT, John Authers critiqued the parallels with Reagan, and looked at other historical omens.

- Reagan cut taxes and boosted the economy (and the deficit), kick-starting an 18-year bull market in US stocks.

But things were different then:

- Bonds were very cheap, yielding 12.5%

- And stocks were close to historic lows (in terms of the Schiller Cape, which I have some issues with)

- The CAPE value was around 8.

Now we have bond yields of 1.6%, CAPE is at 26.5 and we are about to raise interest rates.

For Reagan, the long-decline in bond yields supported the increase in equity valuations, but we will have no such luck this time around.

- Keynesian stimulus today could lead to inflation, higher interest rates, and lower stock multiples.

John instead draws a parallel between Trump’s election and the rally that followed George (HW) Bush’s invasion of Kuwait in 1991.

- The market had fallen during the Kuwait crisis, and everyone thought it would fall more.

- But everyone who would sell had already done so, and when the war started the market went up.

The same thing happened again when the other President Bush invaded Iraq in 2003.

- The problem with the Trump rally is that unlike the other two, it doesn’t follow a recent prolonged fall.

The other possible parallel is with the 1950s, when the Fed regained independence after the war, and began to raise interest rates once more.

- The 50s saw steady expansion with infrastructure spending on the interstate highways.

- 10-year bond yields were 2.5% when this began, but the CAPE was at 11.

So John concludes that fiscal stimulus will only provide a short-term boost to US stocks, before high valuations lead to a stall.

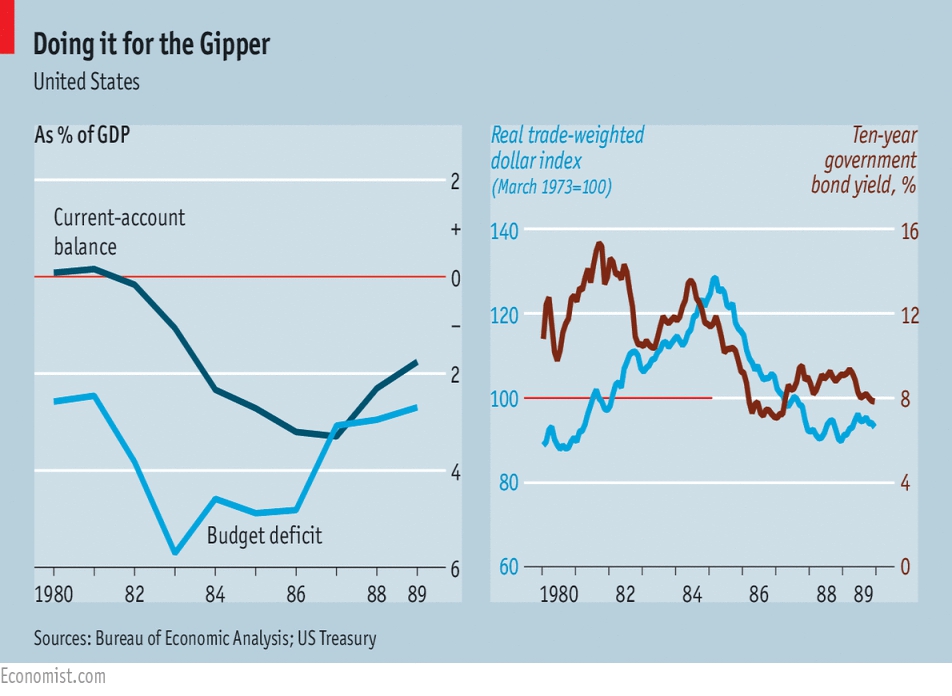

The Economist also compared Trump’s situation to Reagan’s.

- They expect the new tax cuts to reduce government’s receipts by 4% of GDP, compared to 3% back in 1981.

They have three main concerns:

- financial instability – a stronger dollar (from higher interest rates) could leave many emerging market economies with unserviceable dollar-denominated debts – though debts are lower these days

- the higher dollar will boost imports, and an exchange-rate war with China might follow

- tax cuts for the rich might not boost growth as much as expected, since rates are already much lower than in the 1980s, and the resulting increase in inequality could lead to domestic political tensions

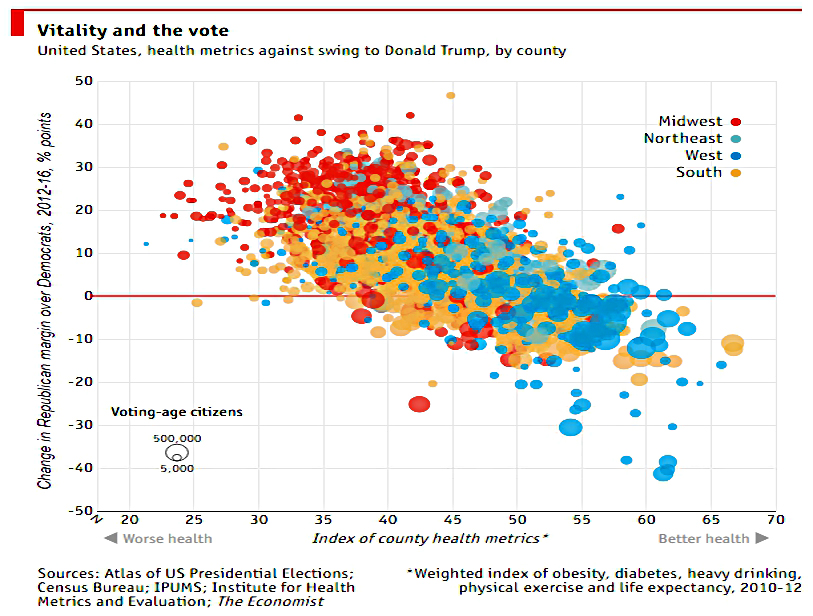

The Economist also looked at why Trump won.

- The initial reaction was that white voters without college degrees in the north of the US were responsible for his victory.

Inspired by a challenge from Patrick Ruffini to “find the variable that can beat % of non-college whites in the electorate as a predictor of county swing to Trump”, the newspaper has come up with public health metrics.

- They looked at life expectancy, obesity, diabetes, heavy drinking and lack of physical activity.

- Between them, these measures explain 43% of Trumps gains over Romney in 2012, compared to 41% for share of non-college whites.

There are two caveats:

- first, the two categories have a large overlap (though even after controlling for race, education, age, sex, income, marital status, immigration and employment, the health stats remain statistically significant).

- second, there’s a chicken and egg situation here – the health of uneducated whites is deteriorating just as that of other groups improves, and this is surely due to the deindustrialisation caused by globalisation.

High unemployment in a county predicts both votes for Trump and low life expectancy.

- Trump won because he picked up more votes than Romney in the communities that are dying as a result of globalisation.

- Free trade is the underlying cause, not a lack of education or poor health.

Over at MoneyWeek, David Stevenson looked at which stocks might do well under Trump.

- His big call was healthcare, based on Obamacare being mostly scrapped.

He went for the four main investment trusts that we’ve discussed previously:

- Polar Capital Healthcare (LSE:PCGH)

- Worldwide Healthcare (LSE:WWH)

- Biotech Growth (LSE:BIOG), and

- BB Healthcare Trust (listing in December).

He also liked:

- US regional banks, but chose an iShares ETF listed in New York to access them through – NYSE:IAT

- “unconventional” oil and gas, via “private equity focused” Riverstone (LSE:RSE), and

- US housebuilders, again through a New York ishares ETF – NYSE:ITB

Indian cash

The Economist provided an update on last week’s news that India has withdrawn its largest banknotes (and 86% of cash by value).

It’s not going well.

- People are being paid to queue to exchange old notes for new, and 16 people have died in the queues.

Most businesses have reported a drop in trade, since they are largely cash-based.

- But sales of luxury goods (eg, Rolexes) and gold have soared.

Supply chains have broken, with 30% less farm produce reaching markets.

- Road-tolls have been suspended.

- GDP will be 2% lower this quarter and next.

Let’s hope that the EU handles the planned phasing out of the €500 note a little more smoothly.

The one per cent

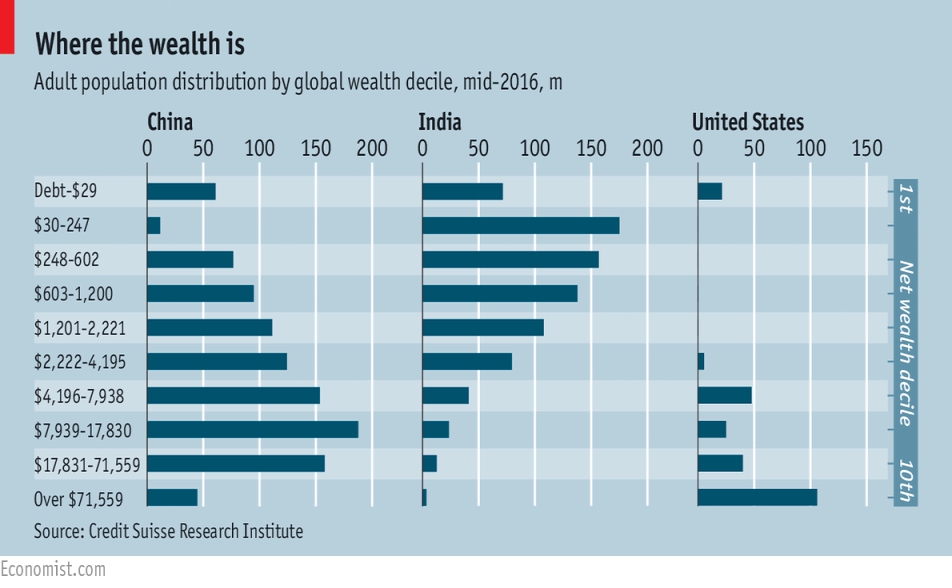

The Economist looked at this year’s Global Wealth Report from Credit Suisse.

- The bottom 50% of the globe now owns less than $2,220, and the top 10% own $71,560.

- The famous 1% elite now begins at $744,400, and includes 18M Americans.

Divided equally, the $256 trn of household wealth – 3.4 times global GDP – would work out at $52,918 per adult.

- But in fact the top 10% own 89% of the wealth.

The bottom tenth is a funny mix, with lots of people from poor countries who own nothing, and many from rich countries, who have a negative net worth.

Stamp duty

The Autumn Statement was a dull affair, but one detail escaped me in last week’s review.

The government has asked the Office for Tax Simplification (OTS) to look at whether stamp duty could be removed from all share purchases.

- Stamp duty is already not used for ETFs and for AIM stocks.

This would be good news – transaction taxes reduce liquidity and impact price discovery.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Hi Mike,

Thanks as always for the weekly round up – always interesting to read some of the things I had missed during the week.

I find the wealth inequality one fascinating (I had missed that!) – I don’t think it had clocked in the back of my mind that so many of the first world would be in the bottom due to excessive debt – just shows how warped it is that we are so reliant on debt.

What did surprise me was the band you needed to hit to get into the top 1% – thats going to be most people who manage to hit FI! I would have thought it would have been much much higher…. guess its time to aim for the top 0.1%! 🙂

FiL

Hi FiL,

Thanks for dropping by.

Inequality is always a tricky subject – you have to think about income vs net worth, country vs country, relative inequality vs absolute poverty. Things have generally been improving globally but getting worse in the richest countries, which is why you see both kinds of headline.

Access to credit is a double edged sword, and millions of people get it wrong.

You’re right that most people who become FI in the UK will be in the top 1%. I’ve no idea where the top 0.1% begins.

Mike

Hi Mike,

Always a pleasure 🙂 It is indeed – and you are spot on with the relative point – living in say Thailand is a lot cheaper so you can live on far less, but it is also a very different life!

And you are spot on it is double edged – no credit extension could hurt people who genuinely need it but sadly its been abused by various “modern” societies for demonstrating how wealthy they arent.

I did have a hunt around on google to see what I could find on the wealth definitions, but from what I have found the top 0.1% in the UK is above £5 million, globally they referred to £20 million – either way its a bucket load of money! When you compare such a small increase from 1% to 0.1% its a huge difference!

FiL