Irregular Roundup, 21st June 2023

We begin today’s Weekly Roundup with the Fed pause.

Contents

Fed pause

The Fed finally skipped raising interest rates, the first pause for more than a year, even as short-term bond rates hit new peaks.

- But the dot plot forecast now indicates a terminal rate of 5.6% (implying two more hikes before the end of the year) rather than the 5.1% indicated three months ago.

- And of course, two more hikes also mean no cuts this year.

This was a surprise, perhaps partly because the recent focus on the debt ceiling “crisis” meant that the Fed couldn’t signal that there were more hikes to come.

- Prior to that, the Fed had been signalling a pause this month, and a move to a more “data-driven” hiking policy.

A pause was also a sensible response to the banking crisis that began in March.

- But the strong labour market and high inflation persist, so it looks as though more hikes will be needed.

The bond market is predicting a terminal rate of around 5.1%, but that’s up 1% from last month.

- The underlying feeling is that we either get a recession (and the Fed stops hiking) or we don’t (and they don’t, at least until inflation is definitively conquered).

Real rates of 2% (that is, 2% higher than whatever they can get inflation down to) should be enough, though rates this high might be needed right through 2024.

Inflation

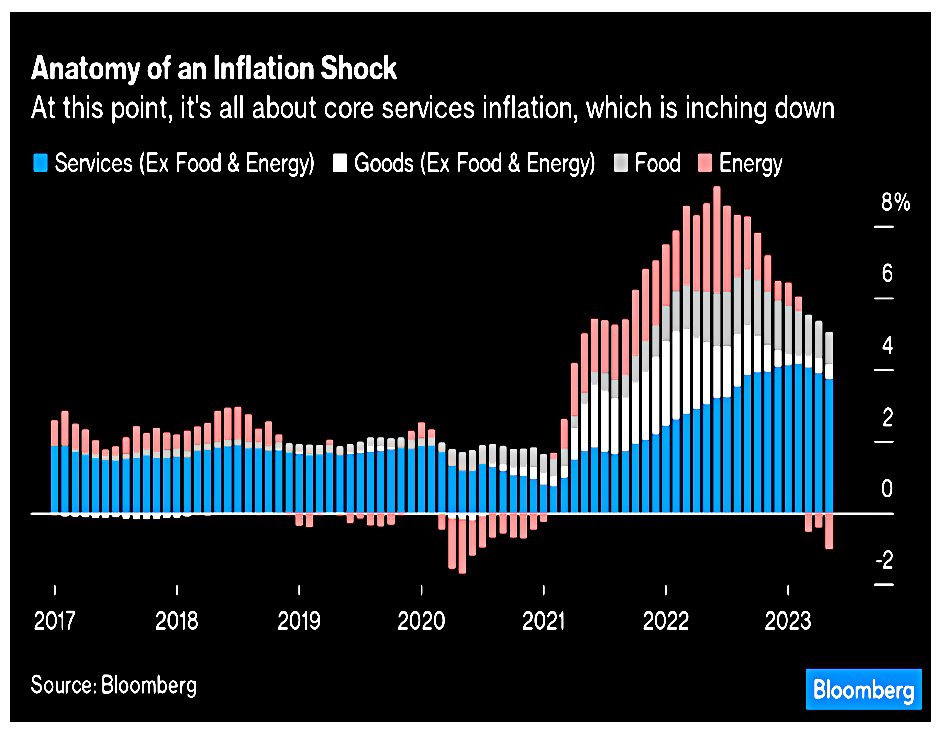

John Authers looked at the US inflation data for May.

- The headline rate dropped from 4.9% to 4% as energy inflation stayed negative, and goods and food inflation fell.

Services inflation is proving stickier, and the core inflation rate increased from 5.0% to 5.4%.

The main driver of services inflation is “owner equivalent rent”, which is a lagging indicator.

It is based on an average of all the leases currently in place, which is correct for gauging how prices have risen year over year, but doesn’t inform on the latest trends.

Monthly data from Zillow suggests the spike is over, and the “trimmed mean” measure of inflation (from the Cleveland Fed) supports this, running at a month-on-month rate of 3% annualized.

- “Sticky inflation” (from the Atlanta Fed) has turned down but remains high – but again, the primary driver is shelter.

This all supports the “higher for longer” argument, but the threat of a recession (and therefore rate cuts) remains high.

- The inverted yield curve (3-month vs 10-year, as tracked by the New York Fed) puts the risk of recession during the next 12 months at 70%, the highest for 40 years.

Nobody seems to have told the labour market, or indeed the stocks market.

Price caps

With UK inflation also proving sticker than politicians and central bankers hoped, and consumers moaning about supermarket prices and accusing retailers of “greedflation”, desperation measures are beginning to surface.

- The government is reportedly looking at capping the price of basic food items, which are up by close to 50% over the last year (if not quite back to 1970s levels yet).

It’s amazing that a Tory government would consider something like this, but then the last time they were introduced in the UK was by Ted Heath in 1973.

- This mandatory cap was in place just before the worst of the 1970s inflation, but it had little impact, and inflation above 10% pa lasted until 1982.

Similar efforts are currently in place in France, Hungary and Croatia.

The most likely effect of a voluntary cap on basics will be price increases on non-basics to make up for lost profits (this would just be an exaggeration of what food shops do already).

Costs

Regular readers will be aware that I think that three things outweigh all others when it comes to investment performance – diversification, costs and taxes.

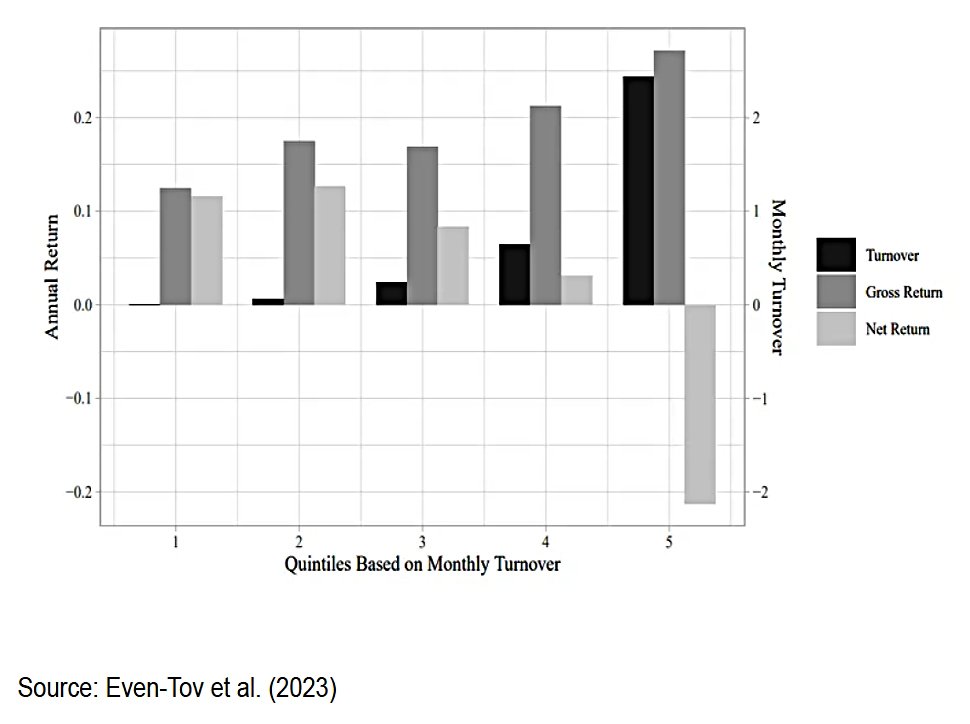

- Recently Joachim Klement looked at one of these – costs.

When investors don’t have to pay for transactions, their performance increases significantly, even though their investment behaviour doesn’t change.

The classic study in this area is a 1990s paper called “Trading is hazardous to your wealth” by Brad Barber and Terrence Odean.

- This showed that those who traded most had the worst results, with day traders losing money after fees.

Costs are a lot lower now, but the effect still holds.

The new study used eToro, a relatively low-cost broker.

Investors who trade more frequently still tend to generate higher returns before transaction costs, but once these costs are taken off, the net of fees returns decline and even become negative for the most active traders.

In 2019, eToro removed transaction fees (on unleveraged trades) for a month in certain countries.

While trading behaviour did not change materially, the performance net of fees of retail investors improved significantly. In fact, it improved by pretty much exactly the amount they would otherwise have spent on transaction fees.

As Joachim points out, returns are uncertain, but fees are known – the easiest way to improve returns is to keep costs low.

John Lee

In a change from his regular FT column, Lord Lee was interviewed in Money Week, looking back over 60 years of investing.

He’s a big fan of the ISA tax wrapper:

Friends from abroad are envious of its many tax advantages: free of income tax, free of capital gains tax, if you hold AIM shares for two years they are free of inheritance tax. And on death spouses can transfer the ISA benefit.

And he thinks that patience is a key factor in investing:

Patience is the thing most people don’t have. They chop and change which is not the way to invest. To make significant money you need to stay put in good quality companies whether they are large or small. And avoid the losses.

He only invests in UK companies, albeit ones which trade globally.

I don’t have the knowledge or expertise to invest directly in China, for example. And I steer clear of healthcare, exploration, bio tech, contracting. They are specialised areas for those with knowledge.

His largest holding is Treatt:

I first invested in them in 1999 when the share price was £1.50 and have bought on 34 different occasions. The more I’ve gotten to know them, the more I’ve liked them so I’ve built a substantial holding. Over the long-term it has been a winner, up by more than 500% in the past decade.

Stocks he described as interesting right now included Christie & Co, Manolete and Partners. STV, Goodwins and Brulines.

Pension funds

The Tony Blair Institute has proposed pooling public and private sector funds into huge “GB superfunds” which would invest in early-stage UK firms.

- Similar funds already exist in Canada and Australia.

The UK has a very large pension market, but foreign pension funds invest much more in our venture capital and private equity sectors.

- The proposal would use the Pension Protection Fund as the central consolidator, and the superfunds would invest 25% of their assets in startups.

The report comes on the back of government focus on reshaping pensions.

- The average allocation to UK equities within pension schemes has fallen from 50% in 2000 to just 2% today.

Instead, funds now mostly invest in “low-risk”, low-yield bonds to match their liabilities.

- Reversing this trend would likely boost the London Stock Exchange, quite apart from any impact on the unlisted sector.

So MPs from both main parties are interested in making pension assets work harder.

- These are interesting ideas, and I might look at them in more detail in a future post.

London listings

Sticking with the LSE, the FCA has proposed some regulatory changes aimed at making the market more attractive to early-stage companies.

- Revolut and ARM are the most recent examples of companies publicly stating that they won’t list in the UK.

THE FCA plans to drop the premium listing category and remove the requirement for a three-year record of accounts and earnings.

I’m not convinced the changes will make much difference.

- The new firms with the greatest potential are all tech companies, and tech will always find it easier to raise capital (and be rewarded with a higher stock valuation) in the US.

Tax on pensions

In FT Adviser, Sonia Rach reported that HMRC has repaid more than £1 bn in tax on pension withdrawals since 2015.

- I have a dog in this fight, as the taxman over-charges me every year and holds on to the money for around six months – I’m still waiting for my refund for 2022/23.

The 1Q23 numbers were £49M reclaimed by 16,000 people, a record for the first quarter.

- The average reclaim was £3K, which suggests that most people are withdrawing less each year than I do.

Canada Life technical director Andrew Tully said:

Eight years on from the introduction of the pension freedoms there must be a better way to administer the tax position around flexible pension withdrawals which would mean HMRC is not processing refunds to the tune of £1bn.

Former pensions minister Steve Webb, now of LCP, said:

This is an absolute disgrace. A system based on systematic over-taxing of pension savers cannot be right. There is no good reason why citizens who access their pension should have to go through the hassle of claiming back excess taxation which they should never have had to pay in the first place.

He recommended making an initial withdrawal of £100, to produce a more accurate tax code before the main withdrawal.

- If you withdraw once a year (as I do), you end up being taxed at 40% and have to claim a refund at some point after your year-end Self Assessment.

Unfortunately, making two withdrawals would double the paperwork (and I mean paperwork – you can’t withdraw electronically from most SIPPs) at the front end.

- So it really depends on how urgently you need the cast mistakenly withheld as tax.

Quick Links

After last week’s catch-up, I have just three for you this week.

- The Economist reported that Britain’s economy may grow by more than expected, but inflation is stickier

- And said that The American credit cycle is at a dangerous point.

- UK Dividend Stocks asked Is it time to buy shares in Robert Walters?

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.