Weekly Roundup, 29th September 2015

We start today’s Weekly Roundup in the FT, with the Chart That Tells a Story.

Contents

Lifetime taxes

Adam Palin looked at the annual taxes paid by the average taxpayer, across their lifetime ((Using today’s tax regime at all ages, and prices adjusted for inflation ))

The Institute for Fiscal Studies published a report this week based around tax payers born between 1945 and 1954, so aged 65 on average today – baby boomers.

Most tax is paid between the ages of 43 and 56, when the total paid per year is more than £10K.

Income tax is the main culprit between 25 and 54, after which VAT takes over as earnings decline sharply, but spending falls more slowly.

The IFS estimates that by the age of 70, people will pay more VAT than income tax. ((Note that in reality this age group will have paid less VAT because rates were lower in the past ))

The IFS also looked at benefits and concluded that boomers become net beneficiaries of the system around age 65. ((With no children, I exclude myself from this calculation ))

The report concluded that the tax and benefit system is much less redistributive over a lifetime than it appears in a single year.

For the mythical average citizen, the system takes at one age and gives back at another, leaving lifetime income little changed. ((This does of course assume that you have average earnings, an average number of children, claim your share of benefits and have the average – ie. dubious – level of health as you grow older; prudent readers of this website are less likely to break even ))

Cashless society

Claer Barrett looked at the problems with moving to a cashless society, as suggested last week by Andy Haldane, the Bank of England’s chief economist.

This would would make it easier to introduce negative interest rates, which in turn should get us to spend more, boosting the economy.

Cashless is also great for retailers – coins and notes are expensive to handle, and the automatic personalised transaction data is missing.

It would also make black economy transactions more difficult, perhaps with unseen side effects.

Claer herself has started to use a contactless debit card, and so is one of the advance troops in this revolution.

So am I as it happens, and we are not alone. Contactless payments rose by 255% in the year to August, and the transaction limit has just been raised from £20 to £30.

The introduction of Apple Pay in July means that even fanbois can join in. But make sure your phone battery will last the length of your tube journey, or you’ll be forever trapped Underground.

Claer has also swapped black cabs for Uber, and worries that it’s becoming too easy for her to spend money.

This is a real issue, as the behavioural psychologists have demonstrated – handing over cash is much more painful for us than virtual payments.

- For an alternative take on the issues with getting rid of cash, have a look at this piece from Alasdair Macleod on the Finance and Economics blog.

Premium Bonds

Paul Lewis, the presenter of MoneyBox on Radio 4, tried to convince us that Premium Bonds are a good idea.

They aren’t. They pay an average (mean) of 1.35% pa in interest, though the small number of larger prizes makes the median return a little lower at around 1.2%. Bonds are instant access, and returns are tax free.

With UK inflation currently arround zero, the Bonds aren’t as stupid an investment as they used to be. But they still aren’t great.

And there is a £50K limit per person – up from £30K a couple of years ago – which means that they can’t play too large a role in the plans of anyone making serious provision for retirement.

Paul may be wrong, but he’s not alone. More than 845,000 people have £30K in Bonds, 340,000 have £40K and 100,000 have the maximum £50K. This lot hold £31bn in premium bonds — more than half the total.

Paul famously keeps all his own savings in cash/ near-cash, which to me makes him as suitable for his job as the vegan that Jeremy Corbyn has made shadow minister for farming.

Cooking the books

Terry Smith took another of his periodic looks at dodgy accounting. This time his focus was the pharma groups who use their own measure of `core’ earnings, excluding many charges.

Back in 1992, I worked at UBS “alongside” Terry ((On the same massive dealing floor, but in a different department entirely )) when his book Accounting for Growth was published.

It’s a great read (if you like accounts!), and probably the first of its kind to show how companies bent the rules to flatter their performance.

Unfortunately some of the companies featured in the book were UBS clients, and he came under pressure from UBS bosses to pull its publication. In the end he was fired and the book did very well.

Terry said in this week’s article that he is often asked to write another book on the subject, but he doesn’t for two reasons:

- the Accounting Standards Board have since stamped out many of the abuses

- he doesn’t think that many people study company accounts anymore

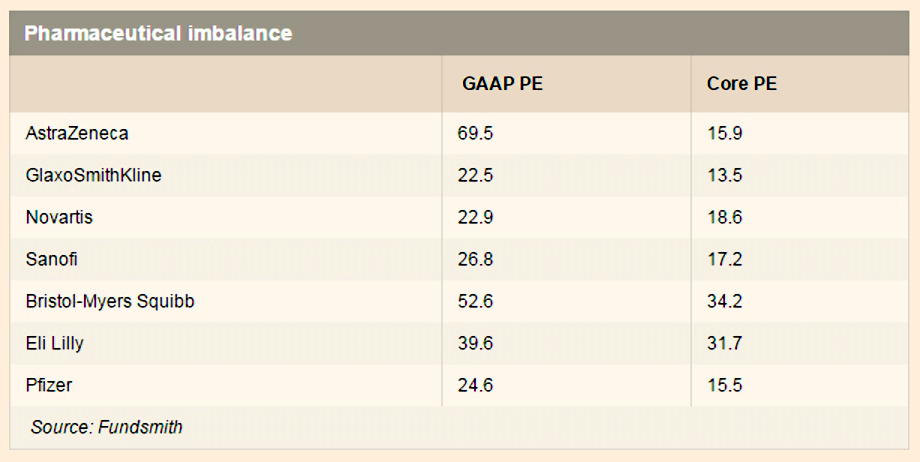

His particular beef is relying on management numbers for “adjusted”, “core” or “underlying” earnings or profits. This is why his fund doesn’t own any pharmaceutical stocks.

The demographics for the sector are favourable – ageing first world populations should increase demand for healthcare – and patents should offer price protection.

But Terry doesn’t trust the numbers. Around 2010 the pharma companies started to report “core” earnings.

These remove “exceptional” items from the standard GAAP (generally accepted accounting principles) numbers:

- Restructuring costs, even though they are common (GlaxoSmithKline has not had a quarter without any since 2008

- Legal charges – patent disputes, regulation and product liability lawsuits are constant features

- Intangible asset amortisation / impairment.

Drug companies (and individual drugs) cost a lot more to buy than the tangible, “hard” assets used to make them, and the difference goes in the balance sheet as an intangible asset (“goodwill”).

Under GAAP, this value is gradually reduced as a patent expires, and cancelled if a new drug fails a trial.

Many (including Buffett) say these charges should be excluded as they are “non-cash” but Terry argues that the cashflow statement will provide the cash flow, and the P&L should include them.

- AstraZeneca currently excludes a £1.6bn annual charge.

- Excluding these numbers has supported a recent industry buying spree of biotech firms ($80bn in 2014).

Management incentives have also been realigned to the new numbers, which means that things are getting worse.

GAAP EPS has gradually reduced as a proportion of “core” EPS:

- AstraZeneca has gone from 84% in 2010 to 23% in 2014

- more and more bad stuff is being excluded

- ratings are now extraordinary on a GAAP basis

Recommended funds are mediocre

Judith Evans looked at the funds recommended by the UK fund supermarkets.

Only half (52%) have outperformed their sector averages over the past five years, according to Boring Money. Only 48% outperformed over three years.

That sounds about right to me, but I suppose investors might be assuming that the supermarkets have above average predictive powers.

Laith Khalaf of at Hargreaves Lansdown countered that three-quarters of their Wealth 150 list funds outperformed over 5 years, by an average of 19%.

Hargreaves’ use data that includes funds that have closed or moved sector. which brings down the sector averages slightly.

Dividends are just returned capital

Neil Collins looked at the high dividends being paid by commodities companies.

Shares in BHP Billiton yield 7.8%; Shell returns 7.9%. Both firms have pledged to keep paying their dividends. Yet despite the general desperation for income, their shares remain depressed.

Commodities prices mean that projects which looked fine a couple of years ago now need to be shelved. And the dividends are being paid out of the cash released from this, rather than from earnings.

A dividend yield is only worth something if it is sustainable, and the market thinks that these aren’t.

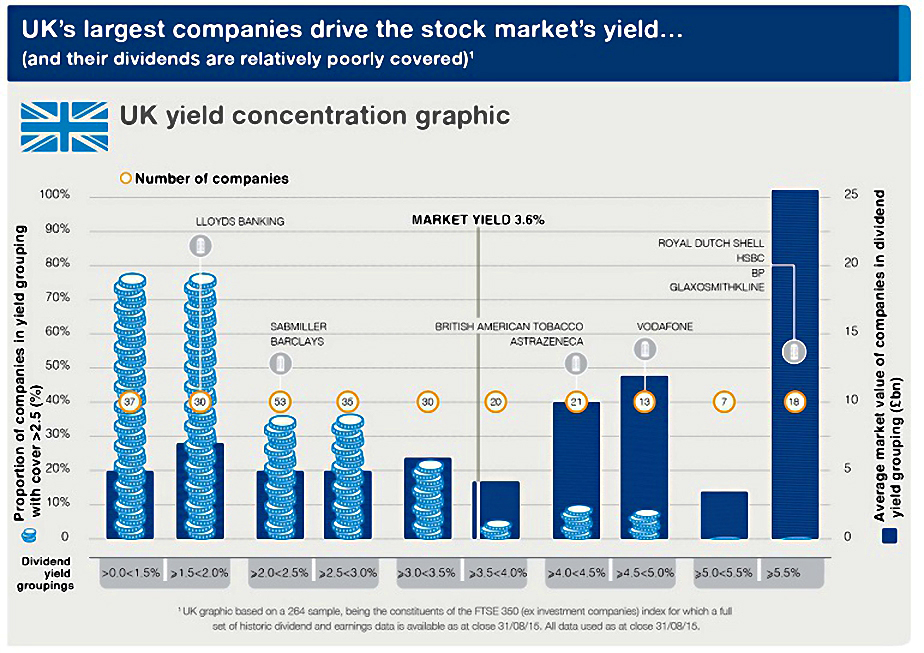

- For more on the concentration of yield in the FTSE-350, take a look at this article from Algy Hall in the Investors Chronicle.

Replacing the inflation rate target

The Economist looked at the possibility of replacing the inflation rate target used by Western central banks with something more suited to the times that we live in.

The usual relationship between inflation and unemployment appears to have

broken:

- low unemployment should push inflation up, by raising wages

- high unemployment should reduce inflation

In the 2008 crisis, unemployment rose sharply but inflation came down gradually. Now that unemployment is generally low again, inflation is weak to non-existent.

And so it has proved impossible to date to raise interest rates.

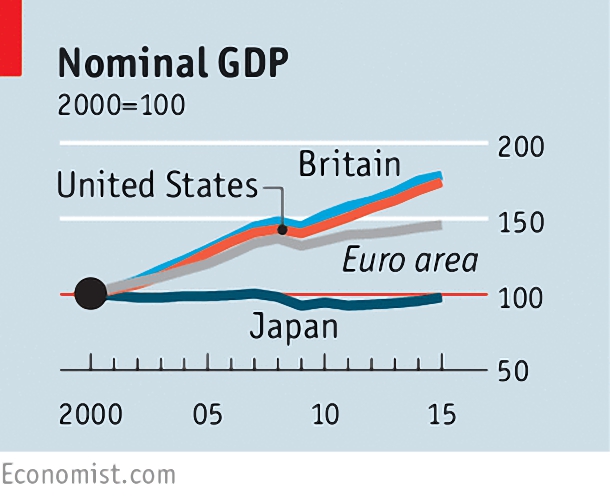

The newspaper suggests targeting nominal GDP (NGDP) instead of inflation. NGDP copes better with cheap imports, which boost growth, but depress prices.

But as we have seen, GDP is hard to measure, full of errors and omissions, subject to revision, and not a number that the public is used to watching.

The Economist suggests rebranding NGDP as “growth in income.” Growth in national income might be even better.

The newspaper also points out that the indicators of slack in the labour market that are currently used by central banks – alongside inflation – suffer from most of the same problems.

Most economies are now well short of their pre-recession trend in NGDP:

- America is 16% below the norm

- Britain is 15% short

- the euro zone and Japan are even further behind

These are big gaps to make up, and doing so quickly would mean high inflation. The paper suggests targeting a 5% catchup, from a combination of better productivity, more hiring and faster inflation.

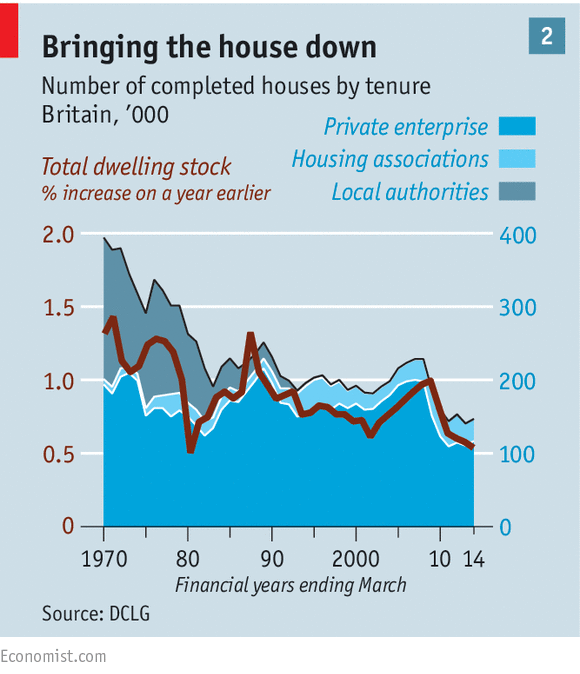

House prices

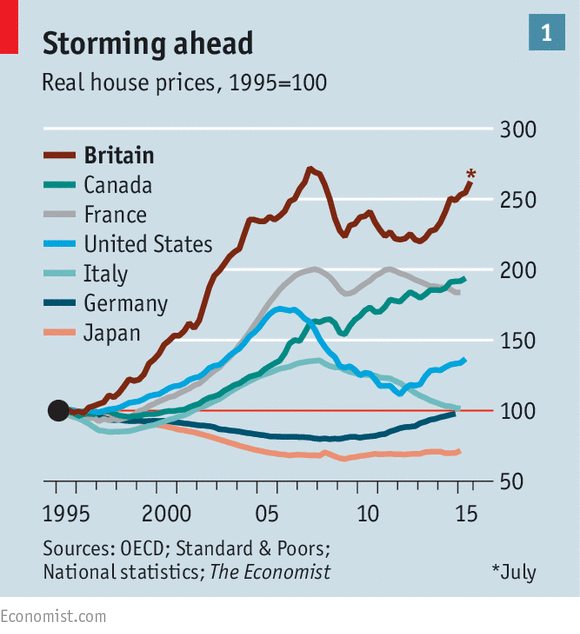

The Economist also looked at Britain’s booming housing market.

The past 20 years has seen the best growth in the G7, and British property – particularly in the south-east – is arguably the most expensive outside Monaco.

This pushes people out to London to less productive towns, or makes them waste time on long commutes. Mortgage debt for 35 year olds has increased by 50% over the 20 years.

One factor is offshore money coming into London, but that’s just the central prime areas.

- There’s a bit of a ripple effect as UK buyers are pushed out to Zone 2, but probably not much impact on the outer boroughs or the rest of the south-east.

A bigger issue is the growing population, up 11% over the past 20 years.

- Later marriages and earlier divorces mean even more households than that.

Interest rates are at historical lows in nominal terms, and have been below average in real terms for more than a decade.

- Loans to income are up from 1.8 in 1981 to 3.2 in 2014.

- Buy to let loans are £190bn, twenty times the 2000 level.

And against all this demand, there is little supply.

- Local authority builds are down from 130K per year in the 1970s to 2K now.

- Green belts cover 13% of England, restricting private development. And nobody wants a new house in their own neighbourhood.

New builds seem stuck at 10% of turnover, perhaps because they are priced to hit that top decile of the local market. So as transaction levels drop, so do builds.

Stamp duty is also a problem. The average London property (£430K) now has a tax of £11K, but things are much worse at the top end of the market.

Council tax works in the opposite direction, with bands compressed below average prices in London. ((My council tax in London runs at around 0.2% of the property’s value; the problem is that property prices are so high that moving it up to a theoretically reasonaable 0.5% would make the annual charge £7,500 – which is a lot for a retiree to find ))

Things ought not to get too much “worse” – loan multiples are high, and interest rates must rise in the end – but there’s no good reason to think they will get much better, either.

Biotech pops

Sometimes bubbles burst in unexpected ways.

Biotech has been in a boom market for a decade, but last week that all came to an end when the price of an obscure medicine went up.

Martin Shkreli – a biotech entrepreneur who runs Turing Pharmaceuticals – bought the US rights to Daraprim.

This long out of patent drug treats toxoplasmosis – a parasitic infection particularly dangerous to those with weak immune systems, such as AIDS and cancer patients.

He decided to increase the price $13.50 a pill to $750. Presidential candidate Hillary Clinton called this “outrageous”.

Shkreli agreed to rethink the price rise (without giving any details), but the bull market was over.

In theory there is nothing to stop another firm making the drug under its generic name, pyrimethamine. But the market for Daraprim is so small, and the process for getting permission so difficult, that it may not be worthwhile.

In Britain, GSK sells Daraprim for 67¢ a pill. There’s a lot wrong with the NHS in my opinion, but let’s not replace it with the American health system.

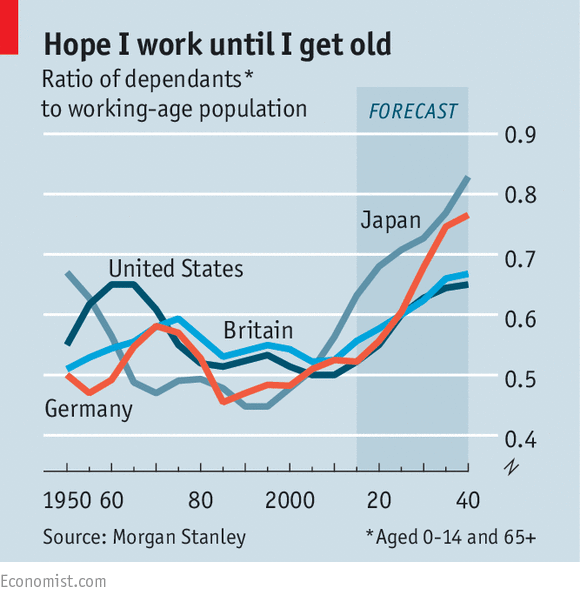

Demographics

Buttonwood looked at the potential economic impacts of demographic change.

A new paper suggests that an ageing population may reverse three long-term

trends:

- the decline in real interest rates

- the squeeze on real wages

- widening inequality

The idea is that these things were caused in the first place by an earlier set of demographic changes:

- the entry of the baby boomers into the workforce after 1970

- the doubling of the global workforce as China and eastern Europe became capitalist

This pushed down wages and reduced productivity improvements. It also reduced the costs of imported goods, as manufacturing relocated to cheaper countries.

This in turn produced deflation, which allowed monetary easing (low interest rates). This pushes up asset prices and that in turn increases inequality.

But now the working age share of the developed world population is falling. Together with the potential for increase demand for care workers, this should push real wages higher, reducing inequality.

Interest rates should balance savings with investments.

- The old naturally save less and spend more.

- But the paper argues that even the middle-aged will now not save enough.

- This is partly because they underestimate the amount required, and partly because others expect to depend on the state.

The paper says that although investment will fall, it will fall more slowly than savings, allowing interest rates to rise.

- This is because most household investment takes the form of housing, and the old are reluctant to downsize.

Firms will also be encouraged to invest by higher wages – they will try to swap labour for capital.

A potential problem is an increase in the labour force from immigration, or increased participation from women or the old.

But skills are also a factor. The old and unskilled find it difficult to work, and the low-skilled will be the first to be displaced by robots.

So the overall picture is complicated, and we may not see the improvements we would hope for. But we can be confident that things are about to change (again).

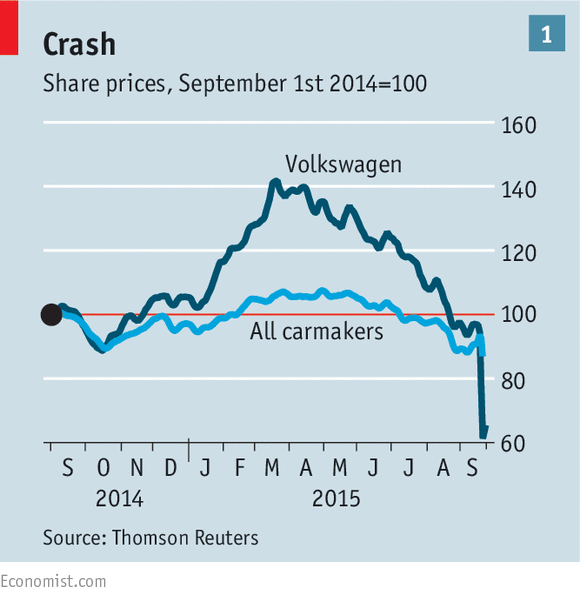

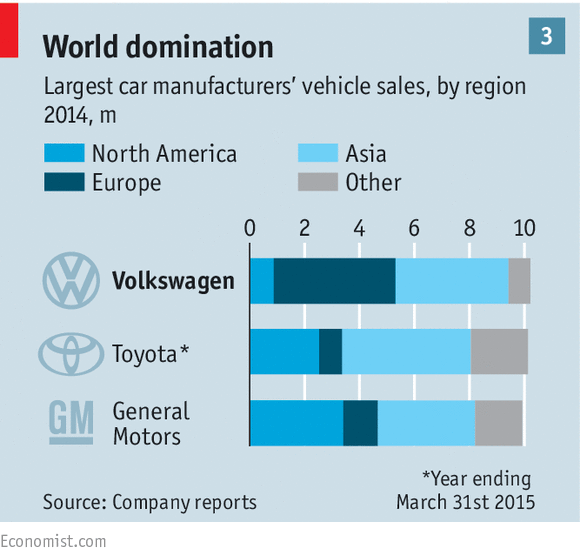

VW cheats the emissions tests

I’ve left the biggest story of the week until last. VW was caught fiddling its diesel emissions tests in the US.

Merryn looked at the story from the trust angle. According to the polls, the pecking order is, starting with the most trusted:

- the family doctor

- the BBC

- journalists on “upmarket” newspapers

- MPs

- trade union leaders

- “people who run large companies”

Already bottom, Merryn thinks the bosses 23% approval rating will have collapsed after this week.

She blames two things for bad behaviour by management. The first is the agency problem:

- despite statutory requirements to act in the interests of shareholders (owners), managers don’t

- it’s hard to organise small shareholders, who are more inclined to sell and move on when things don’t go their way, and fund managers are largely passive

We’ve tried aligning manager interests with stock options, but it doesn’t help:

- using company assets for your own benefit still trumps sharing the rewards with (other) shareholders

- it also encourages short-term thinking to hit share price targets

VW has one huge family shareholder, so this shouldn’t be a factor.

The second problem is money. The disgraced CEO earned €16M last year and leaves with a €28.5M pension.

At these salary levels, nothing else matters. Everyone has a price, and for most people it’s a lot less than €45M.

Merryn sees one silver lining – the compensation payments from the mis-sold diesels are likely to be mostly spent, boosting the economy as surely as helicopter money.

The Economist looked at the likely impacts on the car industry. The initial impacts were to VW: the CEO has gone, and the share price fell by a third, or €26bn.

The newspaper thinks that the time has come to prosecute individuals responsible for corporate crimes. American authorities are making the same noises, but have yet to deliver.

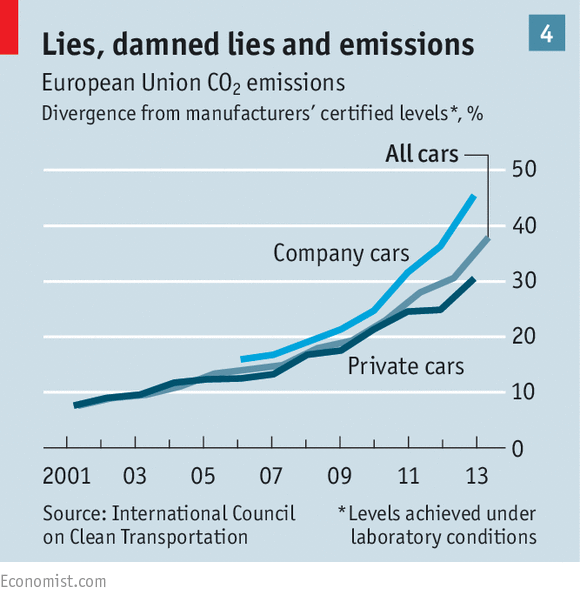

Questions remain on the other side of the Atlantic:

- were VW cheating the European tests as well?

- have Mercedes and BMW been up to the same trickery?

And so the doubts spread – from firm to firm, market to market, manufacturing country to country.

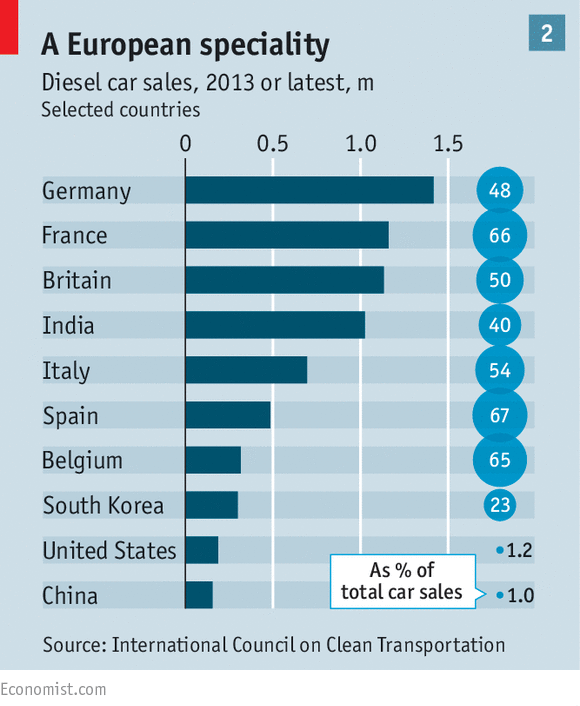

A new testing regime will probably be needed, and it’s possible that this could be the end of diesel (never that popular outside Europe).

It could also be a new opportunity for methane, hydrogen, electricity and hybrids, not to mention ever-cleaner petrol engines.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.