Weekly Roundup, 22nd September 2015

We begin today’s Weekly Roundup with Merryn’s column in the FT.

Contents

Fed holds interest rates steady

Merryn’s article was mostly about Gillan Tett’s new book, The Silo Effect.

[amazon template=thumbnail&asin=1844087573]

The book is essentially about the dangers of not talking to people you disagree with. Apparently careful positioning of the coffee machines and toilets can help with this, as people from different teams and departments will bump into each other more often.

Merryn wonders whether silo thinking – and possibly an executive washroom – was behind the Fed’s decision not to raise interest rates.

Merryn is right to worry that keeping rates too low for too long might inflate a new bubble that leads to the next financial crisis, just as keeping rates too low before 2008 was a contributory factor.

But there is no sign of inflation, and thanks to the commodities crash we are closer to deflation at the moment.

Indeed, a BoE economist announced after the Fed decision that the next move in the UK might be to lower rates even further.

It’s completely possible that within a year (when the commodities crash falls out of the inflation numbers) that China will have recovered somewhat, and inflation might start to rise.

But that’s an argument for raising rates in a year, not now.

John Authers also looked at the Fed’s decision not to raise rates. Though stock markets like cheap money, they have fallen since the decision. This is down to the way that it was explained.

The Fed delayed increasing rates because of worries over deflationary pressure from China. What this amounts to is more uncertainty, which markets don’t like.

China is still growing, but more slowly than before. Last month the government devalued the currency and tried to prop up the stock market.

The US doesn’t export that much to China – Australia, Brazil and Germany are more directly affected. But the Chinese slowdown hits demand for commodities and oil.

The low oil price hits US shale producers and lowers US inflation, so that higher interest rates aren’t needed. So the previous focus on US employment figures will be replaced by a focus on Chinese GDP.

John also wrote about FX reserves, and the huge piles of dollars – more than $10 trn – built up by China and other central banks.

The effect of this was similar to QE – the PBoC printed domestic money and used it to buy foreign bonds. This pushed up prices of US Treasuries and kept yields low.

This now seems to have peaked, and China has started to sell its FX reserves to support the renminbi. Deutsche Bank calls this “quantitative tightening”. US bonds yields may rise without the help of the Fed raising rates.

Special dividends

Maike Currie wrote about looking for income from stocks. She said that dividend growth matters as much as the absolute level of the dividend.

A lower but more sustainable yield may be better than a higher but unsustainable one.

But under recent low interest conditions, most of the good income payers have low growth rates, and they are dangerously concentrated.

Most of the UK’s dividends are issued by half a dozen large payers (Shell, HSBC, utilities like National Grid and Scottish and Southern Energy).

And the gap between dividends and earnings is closing: National Grid can only afford its dividend because so many shareholders take advantage of the ‘scrip’ option (taking their dividend as more shares).

Maike recommended instead looking at companies with regular special dividends.

ITV is a good example – the yield is 2%, but special dividends lift this above 4%. Next yields around 5% when special dividends are included.

Discount airlines like Easyjet and Ryanair are also of interest. Even IAG may reinstate its dividend this year.

Maike also likes motor insurers and house builders. Crest Nicholson, Galliford Try, Taylor Wimpey and Barratt Developments have current yields of around 3%, but Maike sees the potential for this payout ratio to double.

Charity donations

Judith Evans had more on the fallout from the Kids Company scandal, including the story of a pensioner who sold her house to donate £200K to the charity. When the charity couldn’t account for the money, she asked for it back, but she didn’t get it.

There are 160,000 charities in the UK, receiving £10 bn a year in donations from individuals. Total income is around £40bn.

The bigger charities (income more than £5M, only about 1.2% of the sector by number) have almost 70% of the sector’s assets.

The Kids Company story is not an isolated example:

- BeatBullying collapsed last year

- the Halo Trust, a landmine clearance charity supported by Princess Di is under investigation after Angelina Jolie left its board over payments to other trustees

- the Cup Trust, which raised £176M in donations was found to have given only £55K to good causes while claiming Gift Aid of £46m

- the Melton Arts and Crafts Trust, was shut down after the Charity Commission found “no evidence of charitable activity”

The real problem is that the commission lacks the resources to monitor all charities.

Most donations are made on emotional grounds, with little due diligence. Things to look for include:

- does the charity have a “theory of change” that explains what is the difference it wants to make, and how it will achieve it?

- does the money go to front-line services, or it a lot spent on lobbying (for example, Oxfam spends £20M a year on political campaigning)

- what proportion of income goes on fundraising and administration (15% is felt to be reasonable)?

- what is the level of the company’s cash reserves (low reserves were a key problem at Kids Company; 3 to 6 months of reserves is usually about right)?

- look out for “founder syndrome” – a charity that is organised around one charismatic figure

- large donors should visit charities in person, and ask for impact reports on how their money is spent; phasing larger gifts over time is also a good idea

[amazon template=thumbnail&asin=1783350490]

William MacAskill, author of Doing Good Better, suggests five key questions to be asked:

- how many people benefit, and by how much?

- is this the most effective thing you can do?

- is this area neglected?

- what would have happened otherwise?

- what are the chances of success, and how good would success be?

This often leads to supporting health and sanitation projects in the developing world. Two good examples are:

- the Against Malaria Foundation, which distributes mosquito nets, and

- the Schistosomiasis Control Initiative, which supplies medicine through schools to treat neglected tropical diseases

This downside of this approach is that it ignores the following types of charity:

- arts and cultural

- rich world medical

- animal

- local

So in the end each donor will have to decide for themselves.

End of the corporate golden age

In the Economist, Schumpeter suggested that the golden age was over for the Western corporation. A new report by the McKinsey Global Institute (MGI) looks at data for almost 30,000 firms between 1980 and 2013.

- Corporate profits more than tripled during the period, rising from 7.6% of global GDP to 10%

- Two thirds of this went to Western companies

- US after tax profits are at their highest share of national income since 1929

But MGI think the good times are over. Globalisation and the resulting reduction of costs produced this one-off windfall:

- the global labour force has expanded by 1.2 bn since 1980, largely in emerging markets

- corporate tax rates have fallen by up to half across the OECD

- most commodity prices have fallen in real terms

But now competition is increasing:

- there are more than twice as many multinationals as in 1990

- margins are falling and volatility of earnings increasing

- corporate profits are expected to fall back to 8% of global GDP over the next 10 years

- emerging market share of Fortune 500 companies is up from 5% pre-2000 to 26% today

- the 50 largest emerging market firms have double their foreign earnings to 40% of the total

- the current troubles in emerging markets may force them to globalise even more quickly

A second factor is the increasing role of high-tech companies, which can switch their territories more quickly and easily.

The political environment is also becoming more hostile, with populists highlighting “corporate greed” and tax loopholes, and minimum wages rising everywhere.

MGI recommends a focus on ideas, which are more resilient to foreign competition than labour and capital-intensive work.

- The “idea sector” – media, finance and pharmaceuticals, but also logistics and luxury cars – now returns 31% of Western company profits, up from 17% in 1999.

They also foresee a move away from public companies – listings are down from 8,000 in 1996 to half that now – towards private equity and dominant founders.

This may have positive effects – a focus on long-term benefits rather than quarterly earnings, for example – but it may make it harder for outsiders to share in wealth creation.

High valuations

Meanwhile, Buttonwood looked at high valuations. Deutsche Bank has analysed the prices of equities, bonds and residential property in 15 countries back to 1800.

Average valuations are higher than in 2007, and close to an all time high.

Since the three asset classes don’t move in tandem, the aggregated value stays within the 20% to 80% range. For example, during the dotcom bubble of 2000, houses and bonds were both quite cheap.

- Bonds are currently the priciest. Real yields averaged over five years have been lower only 17% of the time.

- Using a GDP proxy for historic profit numbers, equities have been higher only 23% of the time.

- House price data only goes back to 1970. Prices peaked in 2007 and are now at average levels.

The current peak is driven by very low yields on safe assets – the hunt for yield has sent prices of riskier assets higher.

The obvious conclusion is that future returns will be low, particularly for bonds. If inflation reappears, bonds yielding 2% at present may show negative real returns.

Equities have very little headroom – profits, especially in the US, are close to record highs, and valuations are also steep. A return to historical norms would see negative real returns from equities over the next 10 years.

And the same goes for property.

This all bodes particularly badly for US pension funds, which generally assume historic gains of 7.5%+ pa can be projected forward.

The rest of us should take note, and act accordingly.

Hedging market declines

A second Buttonwood article looked at whether market declines could be successfully hedged.

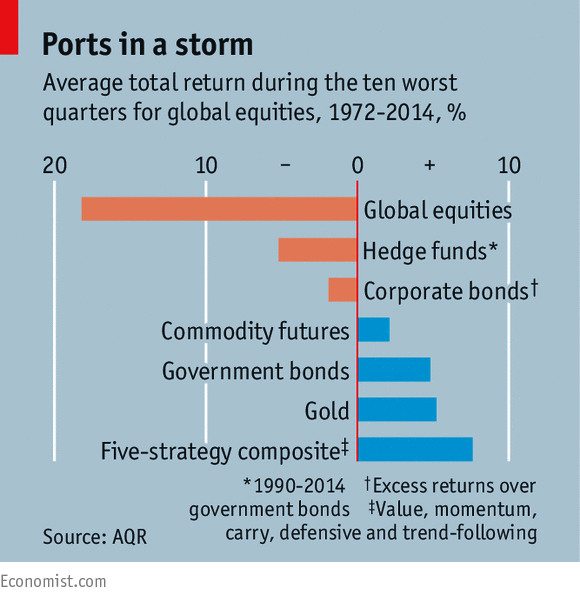

Fund manager AQR looked at the 10 worst quarters for global equities and government bonds between 1972 and 2014.

- On average, equities lost 18% per bad quarter

- Government bonds were a good hedge for equities, returning 4.8% in the average bad equity quarter

- Commodities and gold also produced positive returns

- Corporate bonds were a poor hedge, falling slightly

- During their own bad quarters, bonds lost a lot less on average – only 3.9%

- Equities were an inconsistent hedge here, rising on only 6 out of 10 occasions; the mean result of 3.5% is flattered by a stellar performance in 2Q2009

- Commodities also gained ground, as did cash ((Though cash currently returns almost nothing, and so is less of a hedge ))

Hedge funds could not be tested before 1990, but lost 5.2% on average during 8 bad equity quarters – many are significantly exposed to stock.

AQR suggest that five “factor” strategies used by hedge funds would have done better:

- value

- momentum

- carry

- defensive

- trend following

Even is this is true, applying the hedge is easier said than done. If the signs of an imminent plunge were obvious, investors would just sell everything. It may be simpler for long-term investors to simply ignore short-term falls.

The real-fear is of a Japan-style multi-decade decline – Japanese equities are still at half their 1989 level.

Even worse, the diversification available then to the Japanese may have disappeared – deflationary conditions are now appearing across the developed world, and even emerging markets are in trouble.

The options for investors are disappearing.

Risk-weighted capital

The Economist also looked at risk-weighted capital for banks.

After the 2008 crisis, regulators made banks use more capital from their shareholders and less of their own borrowings. Their next plan is to work out how risky each bank is, and so how much total capital it requires.

A bank’s level of capital significantly affects its profitability, and it’s ability to lend. Debt is currently very cheap, but equity costs banks around 10% pa (since shareholders lose money in every crisis).

The way to settle the dispute between banks and regulators is to attach different weights of capital to different risks:

- government bonds need no capital held against them

- residential mortgages have a 3% requirement

- lending to risky corporations needs more

So risk-weighted assets (RWA) has become an important measure for banks. RWAs as a percentage of their assets – known as ‘RWA density’ – has been falling.

This could be because the banks are making safer loans, or it could be that they are assessing the risks too favourably. ((Historically the risk models came from regulators, but under Basel II – adopted just before the financial crisis – banks are encouraged to come up with their own models, since they should know their own loan book best ))

The risk models are complicated, and the average bank has dozens to deal with different types of assets. They are vetted by regulators, but it can be difficult to spot bias.

Studies have found that putting the same group of assets through the models from different banks produces quite different results. This suggests that the banks are optimising for their own assets.

So regulators are starting to tighten things up:

- In the US, the Fed is starting to focus on the annual “stress test” which subjects a bank to a range of hypothetical problems, using the regulator’s own ‘black box’ risk models.

- The ECB is reviewing 7,000 RWA models at 123 banks for consistency and conservatism.

- The Basel Committee of global regulators is considering using a benchmark model (the “standardised approach”); internal models that differ too much from the benchmark would be rejected.

This sounds good, but there’s no guarantee that a regulator’s model is the best.

The new model might require an extra 10% of capital (€137 bn) across the biggest 35 banks in Europe. This will mean reduced dividends and / or lower levels of lending.

And even the standard model encourages lending to the riskiest borrowers in each category (since they can be charged more for the same amount of capital).

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Interesting stuff about the ‘silo effect’ as we suffer from that a lot in our business. Never mind talking to the team of people who sit right next to us, the teams on the other side of the office (but on the same floor) are practically on a different planet.

Charities – I’m getting increasingly disillusioned with them in the wake of the likes of Kids Company and some charities’ unethical ways of trying to bully people into donating.

Perhaps when I no longer need to work, I will donate my time by volunteering.

Hi Weenie,

I think silos are a bit problem, but I don’t agree with Merryn that interest rates should have gone up last week.

I used to work for big charity and it really put me off them. I hope all the current scandals will lead to some useful reforms.