Weekly Roundup, 31st May 2016

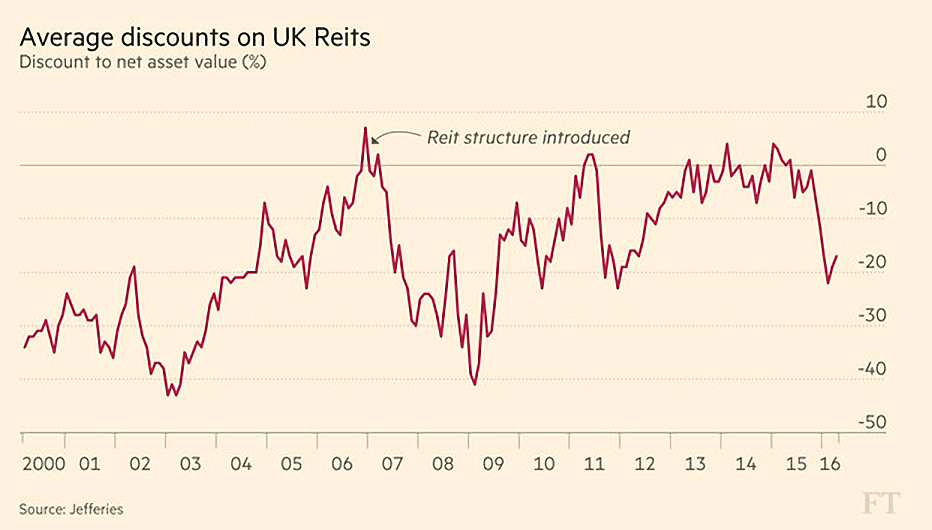

We begin today’s Weekly Roundup in the FT, with the Chart That Tells a Story. This week it was about the discounts on UK REITs.

Contents

UK REIT discounts

REITs are real estate investment trusts – ITs that hold property assets.

- REITs are allowed to avoid corporation tax on profits from rents, so long as the majority of these profits are paid out to shareholders as dividends.

Judith Evans looked at the size of their discounts ahead of the Brexit referendum.

The discount – between the price of the shares on the stock market, and the underlying assets (net asset value, or NAV) – is generally held to indicate how investors feel about the prospects for the company, and to a smaller extent for property in general.

- Back in 2003 after the dot-com boom, the discount peaked at more than 40%.

- The lowest discount was just before the REIT structure was introduced in January 2007, when the discount was almost zero.

Discounts grew again in 2008/09 after the credit crunch, but had slowly recovered until this year, when discounts grew to 20% once more.

- The size of the current discount is thought to be caused by worries over a post-Brexit property market.

- As Remain has pulled ahead with the bookies, the discount has eased a little.

Even with a Remain vote, the commercial property market has had a good last few years, and further growth is not so likely, though there might be a relief rally of post-referendum pent-up deal making.

P2P loan fund cuts dividend

P2P news continued to be bad, as Aime Williams reported that VPC speciality lending has cut its target dividend from 2p per quarter down to 1.5p.

- Even this will be funded by 0.19p of reserves, as actual returns have been just 1.31p.

The fund blamed leveraging and securitisation costs, and a drag from uninvested cash.

The funds (which also included P2PGI, Ranger Direct Lending, GLI Alternative Finance and Funding Circle) are less popular than they were in 2015, and are all now trading at discounts (from 3% to 13%).

- Investors are thought to be concerned about credit quality as the sector grows rapidly, and also the poor returns of the recent few months.

- P2PGI also had a particular problem with a significant number of additional shares being issued.

- The Lending Club scandal in the US probably didn’t help either.

Loans are still performing reasonably well, but question marks will remain until the sector has been through a full economic cycle.

Property – Supply or Demand?

Merryn attempted to persuade us that the problem with property in the UK was a lack of demand, not a lack of supply.

I’m not convinced, but she did have some numbers as evidence.

- The price-to-income ration for house prices had fallen from its peak of 6.2 in 2008 down to 5.2 by 2013, but now it’s almost back to the all-time high.

- This is 40% above the long-term average, so we can agree that something is wrong.

Merryn’s first point is that if there weren’t enough houses, rents should increase as fast as prices, and rental yields wouldn’t fall.

- But price inflation has been 2.3% pa higher than rental inflation since 2006.

There’s some truth in this, but government schemes like Help to Buy naturally push up the price to income ratio.

- Merryn points out that the average buyer under the scheme is aged only 31, rather than the national average first-time buyer age of 37.

- So this looks like future demand being pulled forward.

Rents have also come up against natural constraints, at least where I live.

- Renting a two-bedroom flat in my street now costs 90% of the average UK salary, so there isn’t much room for that to increase.

- That only provides a miserable gross yield of less than 3%.

- God only knows what the net yield after tax is.

Merryn also cites the average household size as evidence that people aren’t being crammed ever closer together.

- Though the number of households has increased by 7% since 2005, we’re at 2.4 people per household, the same as in 2003 and the same as the European average.

- I’d be quite interested to see the “people per square foot” version of that statistic.

- Flats are much smaller than they used to be, and I’m sure they are smaller than the European average.

Merryn also reminds us that there are 600K empty properties in England.

- This one is easier to deal with – they must be largely in the wrong places, or owned by people who can afford two houses.

A final factor is low interest rates.

- They make housing more affordable to buy, and more attractive to let (since the meagre yield can remain higher than the borrowing rate).

I’m far from convinced that renting out flats is the way to riches, but that doesn’t mean that I wouldn’t like to buy a Victorian maisonette in my area.

- Unlike the glass and steel monstrosities being built along the river, they aren’t making any more of these.

- Things will have to change a lot in London for the lifestyle provided by a good address to evaporate.

Whether you will make any money on the capital value is another thing.

- You might even lose a bit, especially if government schemes come to an end.

- And interest rates rise.

- And we build a load of houses in the green belt.

That’s a lot of ifs.

- And the people buying in my street don’t look like they are too worried about that.

Housing fraud

Sticking with property, Natalie Stanton in MoneyWeek warned about property fraud.

- This used to be more common thirty years ago, but I had the impression that the reform of the Land Registry had put an end to it.

- Apparently not.

Natalie wrote about Penny Hastings, wife of journalist and author Sir Max Hastings.

- The fraudster rented Penny’s buy-to-let property using fake ID.

- Then an associate changed her name by deed poll to Penny Hastings, and applied for a passport.

They then listed the house through a different agency than the one they rented it through, and sold it for £1.35M.

- The money ended up in Dubai, but the Land Registry refused to register the sale.

- So the Hastings still own their house, but the new buyer hasn’t got their money back.

So not something that is likely to affect anyone without a buy-to-let property, but worth knowing about in any case.

I’m still a bit baffled that this could happen.

- The fraudster managed to pass a credit test, and got away with paying for everything in cash.

- The selling agency said that the passport was genuine, so they couldn’t be expected to spot the fraud.

It seems that if you are registered at the Land Registry, you should be eligible for compensation if your property is actually sold.

You can also sign up for free property alerts on up to ten properties here, and you don’t need to own the property that you are monitoring. ((Annoyingly this uses a separate account from your Land Registry login ))

If you feel that you are at particular risk, you can enter a “restriction”.

- This would require a solicitor / conveyancer to confirm any activity on the title was being made by you.

Public mis-perceptions

Buttonwood looked at how to deal with the gap between reality and the public’s perception of it.

- And unsurprisingly for the Economist at the moment, he managed to drag Brexit into it.

For example, Americans think that 33% rather than 14% of the population are immigrants.

- Britons think that 24% rather than 5% of the population is Muslim.

People get spending wrong, too.

- 26% of Britons think that foreign aid is a big department – more than picked education or pensions – when it only takes up 1% of government spending.

It’s partly down to innumeracy – only 25% of Britons know that the odds of two consecutive heads is 1 in 4.

And it’s partly down to anecdotal evidence, and the things that people are afraid of.

- Crime and teenage pregnancy are regularly over-estimated (Americans think 24% rather than 3% of teenage girls get pregnant each year).

But it’s also because people don’t trust the government.

- Some Britons simply said their immigration figure was right and the official one was wrong, others said the government ignored illegal immigration.

This makes it difficult for mainstream politicians to fight populists with numbers.

- And it means that Brexiteers don’t care what fat cats and bureaucrats (the IMF, the OECD, the BoE) say about us leaving the EU.

Bringing it back to personal finance, Americans show a poor understanding of mutual funds, lottery odds and compound interest.

Americans underestimate life expectancy by more than five years.

- 77% were confident they were ready for retirement, but only 63% had saved any money whatsoever.

Investment products are tricky, since their “price” – their lifetime cost – is difficult to work out in advance, and depends on assumptions that can be manipulated by sellers with an information advantage.

- Further, the problems often surface years after the original salesman has done a runner.

Education is the long-term answer, but what about the here and now?

Brexit times four

We’re getting closer to peak referendum, and the claims about what would happen if we left the EU become ever more crazy.

- When you’ve played the “World War Three” card with a month to go, who know what comes next?

This week the Economist had four Brexit articles, all firmly in the Remain camp.

- Personally, I’ve had about all the propaganda I can take, and I’m heading off for a nice lie-down by the Med next week.

In the meantime, here’s as much of the discussion as I could bring myself to digest.

The regular Brexit briefing was about red tape.

- There has been much talk of bananas, and how bent they can be.

- There’s also the 48-hour working week, and the power rating of kettles, vacuum-cleaners and hair-dryers.

- The annual cost of the most expensive 100 rules is put at £33bn a year.

The government counters that the benefits of regulation are £59bn a year, but even the Economist thinks they are exaggerating.

There’s obviously an argument for standardisation across markets, though cost-benefit analysis of things like straight bananas would be helpful, as would some system of compensating the losers from the winners’ gains.

- It also true that Britain introduced a lot of its own rules, and often votes in favour of those from Brussels.

- And it’s clear that by global developed country standards, Britain remains lightly regulated.

- And Brussels is less active in terms of regulation than in decades past.

But standardisation by a committee of close to 30 countries is a bad idea.

- Perhaps EU champions could be allowed to choose “best of breed” regulations for us all, on a per-industry basis.

And why do the 90% of UK firms that don’t export have to comply with 100% of EU regulations?

- Why can’t there be “home” and “away” products?

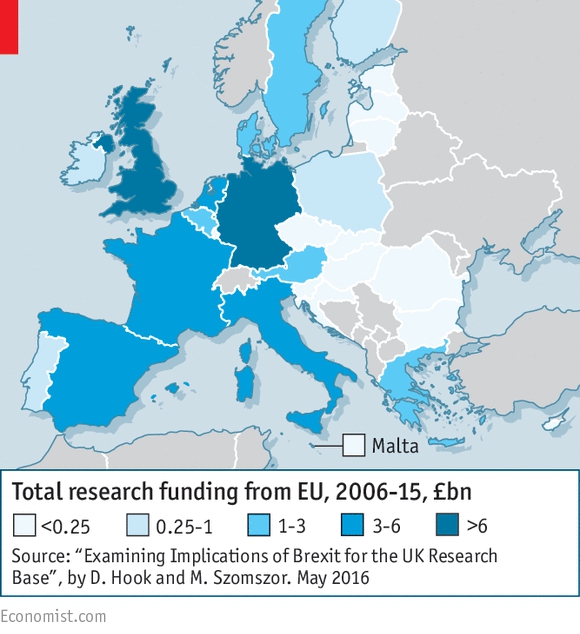

The second article was about science.

- Scientists tend not to be too political, but 80% support Remain.

- With 1% of global population, Britain produces 16% of the best (most highly cited) scientific papers.

- So the sector wants to remain connected.

This is partly about money.

- The UK government has cut funding over the past four years and 10% of research cash now comes from the EU.

- This also makes cross-border collaboration easier.

But Brexit could lead to more Commonwealth scientists (eg. from India) coming to Britain, and some EU regulations on clinical trials get in the way.

The third article was by Bagehot, who claimed that Brexit would be a betrayal of Britain’s past as well as its future.

- He began by describing the “Love Europe, Hate the EU” wing of the Brexit camp, who feel that Britain is “shackled to a corpse”. ((I count myself a loose member of this wing ))

Bagehot doesn’t buy it, worrying instead about the underlying forces of “nationalism, fragmentation and demagoguery” that are part of continental Europe’s history.

He thinks that we can’t abandon our neighbours in their hour of need.

- He says that withdrawing now would be like “spotting your neighbour’s house on fire and resolving to put a better lock on your door”.

I’ll leave you to dig deeper if you are so inclined.

The final piece was about the effects of Brexit on banking.

- The world’s biggest banks count London as a home and would have to decide how much business to move away.

Already under cost pressures, they are mostly adopting the ostrich approach.

- Little is being spent on contingency plans, and the money won’t be used until it has to be.

Instead they are treating the referendum as a market event, with volatility and liquidity impacts, but a known date for resolution.

The EU’s “passport” rules – which allow UK subsidiaries to operate throughout the EU – will likely force greater action if Brexit were to happen.

- This could be good news for Paris or Frankfurt, or even for Dublin.

But they said the same thing about Britain’s decision not to join the euro.

- People like living in London, and the auxiliary industries like accountants and lawyers are very strong.

They could be crying wolf again.

Dating

To rid ourselves of the taste of referendum hogwash, let’s turn to the economics of dating, and a new book by Moira Weigel called The Labour of Love.

[amazon template=thumbnail&asin=0374182531]

The rules have changed a lot over the past 100 years.

- Men originally visited eligible women under family supervision, and had to be prepared to marry.

Industrialisation meant that many working women lived in conditions unsuitable for gentlemen callers’ visits, so “dating” in restaurants and dance halls allowed better-paid men to entice their targets with a “free treat”.

- Initially this was treated as a branch of prostitution, but by 1910 it had caught on.

- It led first to the cosmetics industry (1920s) and eventually to the singles bar, which allowed in women without men (1960s).

As birth rates fell, children were better cared for, and co-ed colleges introduced the sexes to one another in the US from the 1920s.

- Cars were also more widely available across the Atlantic, and “romantic drives” became common.

After the Second World War, a shortage of men encouraged women to “go steady” at the first opportunity.

Dating services developed in the 1980s, the fore-runners of today’s apps.

- Now people date into their 40s before using fertility treatments to get pregnant.

But the basic transaction hasn’t changed that much.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.