Weekly Roundup, 4th February 2016

We begin today’s Weekly Roundup in the FT, with the Chart That Tells a Story.

Contents

British Shopping

Paul McClean looked at British retail sales over the past 20 years.

The amount spent has increased steadily, but in recent years, goods have become cheaper and they have been bought in greater quantities.

It’s not just the oil price fall. There’s a continuing trend for discounters to gain market share from incumbents, in both food and non-food markets.

- The supermarkets in particular have been forced to reduce their own prices.

Online retailers have also reduced prices through low overheads and the ease of making comparisons across sites.

- Multi-channel retailers often keep their shop prices as low as their online offer.

There are also too many shops.

- Ease of entry online means that the equivalent of 65 London Westfield centres have been added over the past 10 years, against a much smaller increase in demand.

It’s interesting to note that people spend more as prices fall. Consumers just can’t keep the cash in their wallets and purses.

- There is a slight recent trend downwards in shops, but this is countered by increased spending in restaurants and on days out.

With price deflation or at best lowflation set to stay, is there a ceiling on how many things people can buy?

- If so, we can expect casualties over the next few years.

UK dividends

Maike Currie reported on the threat to UK dividends.

The average yield on the FTSE 100 is around 4%, but a lot of companies look as though they pay more than this, and four – Anglo American, Glencore, Standard Chartered and BHP Billiton – have trailing yields above 10%.

- Shell, Rio Tinto and Aberdeen Asset Management aren’t far behind (> 8%)

- BP, Pearson, HSBC and Centrica all have trailing yields above 6%

But dividend cover is at its lowest for 6 years, and commentators are predicting the first fall in total dividends paid since 2010.

- So far Anglo American, Glencore and Standard Chartered have announced cuts or suspensions.

So you have to weigh up whether the fortunes of beleaguered sectors will recover.

- For miners and oil firms, 2016 doesn’t look rosy.

- Aberdeen and Pearson also have their own individual problems.

Of course, the larger firms – especially the oil majors – have cash piles from which to fund their dividends for a year or two.

- So look out for public statements of intent.

Retirement risks

Don Ezra looked at the risks involved in saving for retirement, and how to deal with them.

He began by pointing out that most people don’t save enough (15% to 20% of earnings) to have the retirement income they would like.

- The more you fall short of the 20% target, the more risk you will need to take on to close the gap.

Before we talk about these risks, we need to re-state the usual disclaimer that volatility is not risk.

- If you are saving for a retirement that begins in 20 years, or even if like me, you are starting a retirement that you hope will last 30 years, short-term wobbles in prices are not the big issue.

Once more with feeling: volatility is not risk.

The big risk is that over the long-term, your investment returns won’t match your expectations.

- For much of my investment life, I thought that extremely unlikely.

- But since 2008, returns have been propped up by QE and the like.

- I now have quite a lot of highly rated property exposure that I can’t easily get out of.

- And company earnings don’t look to be growing rapidly.

- So maybe this is a big issue after all.

Luckily, I have enough saved already to scrape through on a baked beans and economy carrots lifestyle, so perhaps all I have to do is hope there isn’t a meltdown.

Back to Don. He references a book by William Bernstein called Deep Risk.

[amazon template=thumbnail&asin=0988780313]

Shallow risk is that we might be forced to interact with the market at a bad time (buy when it’s gone up or sell when its gone down).

- We can fix this (see below).

Deep risk is the one I’m worried about – that the economy, and therefore the stock market, doesn’t perform. ((Note that there is quite some evidence that the economy – GDP growth – doesn’t drive stock market returns, but that’s an issue for another day ))

- It’s a bit harder to deal with this.

Bernstein has four causes of the deep risk doomsday:

- inflation – most likely

- Inflation is the big problem, which is why most diversified portfolios include global equities, property, commodities and index-linked gilts.

- deflation – unlikely

- Deflation is hard, too. Global equities, long-dated gilts, fixed-term deposit and gold can help, as can cash under the mattress.

- confiscation (taxation) – possible

- The only thing you can do about confiscation (taxes, financial repression) is to go global with your investments, and perhaps keep some real assets (a house, gold coins).

- devastation (wars and natural disasters) – unlikely

- For devastation, we have to hope that it’s localised, and invest globally.

So the basic plan for deep risk is a portfolio diversified across assets and geography.

- Plus an eye open for which of the four horseman seems most likely at the moment, so that you can adjust accordingly.

Shallow risk is more closely related to volatility, but it’s easy to avoid.

In the accumulation phase, it’s nothing to worry about.

- Pound cost averaging means that you’ll actually benefit if you make regular (monthly) savings.

In decumulation, just keep a few years of money in cash or fixed-term deposits.

- Make sure you can ride out a bear market in equities, and don’t have to sell anything at a low price.

- As you spend the money, check each year for a recovery in prices, and when it arrives, sell some stock to top-up your liquid reserves.

This is my personal strategy, and I think you should consider it too.

- The only thing you have to decide is how many years of shallow risk you want to – and can afford to – insure against.

Money manager capitalism

Merryn mourned the passing of old-fashioned share ownership by individuals, which has been falling for decades.

- Thatcher gave things a boost in the 1980s when she abolished dividend controls, cut dividend taxes from 98% to 40%, introduced ISAs (as PEPs), deregulated the stock exchange (Big Bang) and privatised a lot of stodgy state firms.

- There was also a nice 18-year bull market to keep people interested until 2000.

- The number of individual shareholders rose from 3M to 8M.

But now we have “money manager capitalism“.

- In 1969, 47% of the UK market was owned by individuals and 30% by institutions (funds, pensions, insurance companies).

- Individuals are now down to 12%.

The problem with this is that middle-men have different incentives.

This is part of a bigger problem than undermines capitalism generally – the agency problem.

- Unless you run your own business, you have to hand things over to a manager.

- Aligning the incentives of a management team with those of the owners is extremely difficult.

Here are a few problems with money managers:

- They get paid for short-term performance, which makes them too focused on today’s prices offered by Mr Market.

- They don’t want businesses to invest too much and depress their profits.

- Or to move into new businesses that will probably be loss-making initially.

- They don’t care too much about excessive pay for executives.

- They prefer debt to equity as it costs less (the interest payments are offset against profits).

- They will accept almost any offer for a company that is higher than the current share price.

- This in turn leads to fewer, larger companies.

- New IPOs haven’t entirely replaced the smaller merged firms since companies are coming to market later and larger.

- For one thing, debt has been easy and cheap in recent years.

- For another, private equity, VC and now crowdfunding have been competing with listed equity.

- And tech firms don’t need that much capital anyway.

This is bad for a number of reasons:

- big firms don’t listen to anyone, not even to the money managers

- if the public doesn’t own shares directly, it won’t be sympathetic to business, or to those who do own shares

- and with company growth happening off market, wealth is more concentrated

Investors can buy private equity and VC funds to counteract this (and they have – witness the popularity of Woodford’s Patient Capital fund).

- I can’t recommend EIS or equity crowdfunding as Merryn does – they are far too risky for most people.

But in the wider sense, there’s no prospect of turning back the clock, sadly.

Care homes

Izabella Kaminska looked at the cost of children’s homes, which are “three times Eton College fees” according to the BBC.

- Eton is £12K a term or £36K a year, suggesting a place in a care home costs more than £100K.

- Amazingly, this seems to be true – it’s £3K a week for a place in a care home.

Eton can undercut the care homes because it gets nice kids with no behavioural problems.

- They need less supervision, which means lower staff ratios.

- Eton has an 8 to 1 pupil to teacher ratio, while state schools average 17 pupils per teacher.

In care homes there are between one and four staff members per child.

- Yes, that’s right – 1:4, not 4:1.

- More staff than children.

There’s also a smaller issue around whether the companies who run care homes make excess profits.

- More than 500 firms operate 1,719 home between them.

- Competitive bidding is used, but it doesn’t seem to be getting the prices down.

There’s obviously reputational risk to operating the homes (witness the retirement homes and young offenders scandals), so firms will want to make decent money.

Fostering is much cheaper than a care home.

- £800 per week per child, though some costs of screening foster parents are excluded.

So we need to do something to incentivise fostering, even if it pushes up the costs a bit.

- And we need to do something else to dis-incentivise children in the kind of families that lead to kids being taken into care.

Google tax

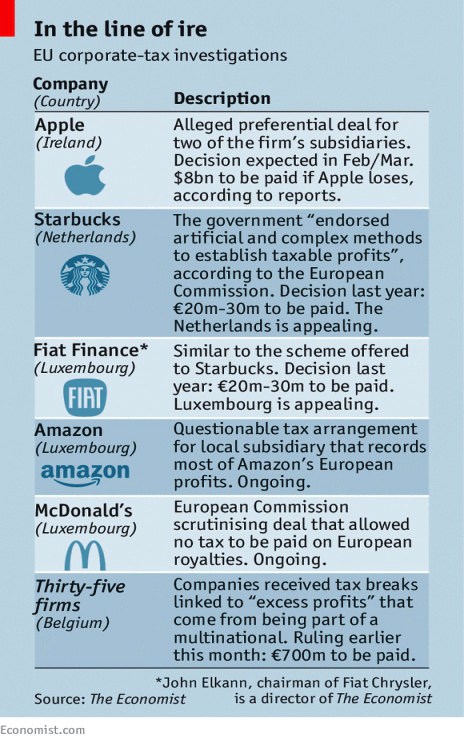

The big story of the week was Google tax, which attracted two stories in the Economist (1 and 2) and one in the FT.

It’s clear that George Osborne made a PR mistake in claiming that the UK Government’s agreement with Google – over £130M in back taxes (over a decade) and slightly tougher rules on future taxes – was a “major success”.

- France and Ireland (or rather the European Commission) plan to be a lot tougher on tech giants – $8bn in the case of the EC.

But the real problem is the lack of international coordination on corporate tax dodging.

Corporate taxes are not a great idea in principle.

- They are passed on to citizens (investors, employees and consumers) and it would be more efficient to tax people directly.

- A company making small profits and paying little in tax could be investing for the future, or paying high salaries to its staff (who will pay the tax instead themselves).

- But people think that companies exist in another economic universe, and they like the idea of punishing their masters.

A second issue is that if companies pay less tax than people, people – especially rich people – will hide behind companies.

So a compromise position is to make the system neutral between people and companies, and difficult to avoid.

- For small companies in the UK, there has been a lot of travel in this direction over the past 20 years.

- For larger, and especially multi-national firms, there hasn’t been so much progress.

International corporate tax law includes dozens of bilateral treaties from decades ago, and designed around manufacturing firms.

- Intellectual property (IP) is intangible, and easy to re-locate into a low tax regime.

- Charging the rest of the firm to use the IP moves the profits there as well.

The OECD is trying to tie tax to activity, but it insists on seeing a multinational as a collection of national firms – the bottom up approach.

- Toughening up “transfer pricing” rules means more rules and more loopholes.

A better approach would be to go top down, working out the overall tax first and then splitting it across countries according to sales, employees and assets etc.

- This transparency would help to convince the public that corporate tax was fair.

Robots vs humans

The Economist reported that jobs in poor countries may be more vulnerable to automation than those in rich countries.

- A 2013 study from Oxford University found that 47% of jobs in the US were at risk.

- A follow-up report now says that the threat is bigger in poorer countries 69% in India, 77% in China and 85% in Ethiopia.

Rich countries have more jobs that are harder for machines

- creative jobs, complex interactions like arguing a case in court, and a blend of analysis and dexterity like heart and brain surgery.

In poor countries the jobs are less skilled, but there is also less capital tied up in existing solutions.

- A new city in China can leap-frog human taxis and go directly to driverless ones, in the same way that poor farmers in Africa missed out desktop computers and went straight to smartphones.

Cheap labour for manufacturing is no longer a way out of poverty for developing nations, as robots can repay their costs in less than two years.

- There is a worry that Africa and India have reached “premature de-industrialisation”, where a country’s growth stalls at low levels of income.

They can fight back (delay the inevitable?) by loosening labour laws, but the only real defence against automation is consumer preference.

- Customers in the rich US will still pay for valet parking and human cashiers in the supermarket. But will the rest of the world?

Corruption

The newspaper also reported that contrary to popular belief, higher wages make corruption worse.

In 2010 Ghana doubled the pay of police officers, and everyone hoped that they would stop extorting money from drivers at roadblocks.

- Two economists surveyed 2,100 truck drivers during the period, and found that the cops became more corrupt after the salary increase, both in absolute terms and relative to officials from neighbouring Burkina Faso.

Economic theory would predict the opposite:

- corruption is risky, and if you are caught you lose your salary – a high salary gives you more to lose

- theory assumes that people have an income target, and if this comes from your salary, you don’t need the bribes ((This is the argument used during the UK MPs expenses scandal, that MPs earn less than people of similar “quality” ))

In fact rich world employees don’t work less when their pay goes up, so perhaps there is no income target after all.

The economists suggest lottery winner syndrome as the explanation for the Ghana cops:

- corrupt superiors or greedy relatives might have asked for more money.

Alternatively, it could be the “I’m worth it” theory:

- higher pay means that cops think more of themselves, and ask for bigger bribes.

There’s also the possibility that the risk of being caught is so low in Ghana that loss of the higher salary is not a dis-incentive.

- Higher pay and stiff have stopped corruption in Singapore.

But in Ghana at least, more money on its own is not enough.

Wage insurance

Also from the Economist, a left-wing idea – from Obama of all people – that is a good one for a change.

As technology advances, there are casualties – people whose skills are no longer in demand. ((Just ask the Luddites ))

Obama wants the government to provide wage insurance.

- A worker who loses his job and gets a lower-paying one will have half the shortfall made up by the government for the first two years after he loses his job.

- There are exclusions for jobs paying above $50K pa, and a $10K cap on the payouts to a single worker.

- It will cost $3bn to $bn per year, which amounts to an insurance premium of $25 pa per worker.

- This kind of insurance isn’t available in a free market because only those at risk will take it up.

- Apparently something similar already exists in the US for workers over 50 who lose their jobs because of foreign competition.

Of course the extension to all workers is not popular with Republicans and won’t become law in the short-term.

The proposal reminds me of how the dole was first conceived in the UK – a short-term payout to workers with a track record who had hit bad luck.

- A hundred years down the line, welfare is now a lifestyle choice.

Credit yields

Buttonwood looked at credit yields – a story of “the have-yields and the yield-nots”.

- Around €65 bn ($71 bn) of European corporate bonds are trading on negative yields – investors pay money to hold them.

- But rates on junk (low-quality) bonds are rising.

- The spread over government bond rates is up 3.5% from March 2015.

- It’s now close to the gap at the time of the euro crisis in 2011.

- But it’s less than half as big as after Lehman Brothers collapsed in 2008.

The stock market’s wobbles have made investors look for safely.

- Big safe firms like Nestlé track towards local (Swiss) government bonds, which are already negative out to ten years.

The historical average recovery rate on defaulted unsecured bonds is 40%, so avoiding junk during dodgy times can pay off.

Once the spread of a junk bond over Treasuries hits 10%, the bond is labelled “distressed”.

- Almost 30% of junk bonds are now distressed.

- This is up from 13.5% in a year, and the highest since 2009.

- Oil and gas firms account for 30% of the total.

- The default rate has doubled to 2.8%, but is still below the long-term average of 4.3%.

The driver for all this is the end of global QE and the Fed’s December interest rate rise.

- The ECB and the BoJ are still buying bonds, but China and other emerging market central banks are selling.

- The monetary stimulus hasn’t led to an improvement in the real economy, so a correction is possible.

- Bad news (the fall in commodity prices, the slowdown in emerging markets, falling profit forecasts) has more impact now.

Regulation means that banks don’t hold so many bonds these days, and sales of illiquid issues to meet fund redemptions can force prices even lower.

- This can trigger more withdrawals and lead to a vicious circle.

The bond market is waiting to hear some good news for a change.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.