Weekly Roundup, 4th September 2018

We begin today’s Weekly Roundup in the FT, where Terry Smith was busting the myths of investment.

Busting myths

We’re into September now, but the UK’s financial journalists don’t seem to have made it back from their summer holidays, so this will be another short report.

The two myths that he had his eye on were:

- you need to take more risk to get a higher return, and

- asset allocation is the most important contributor to performance.

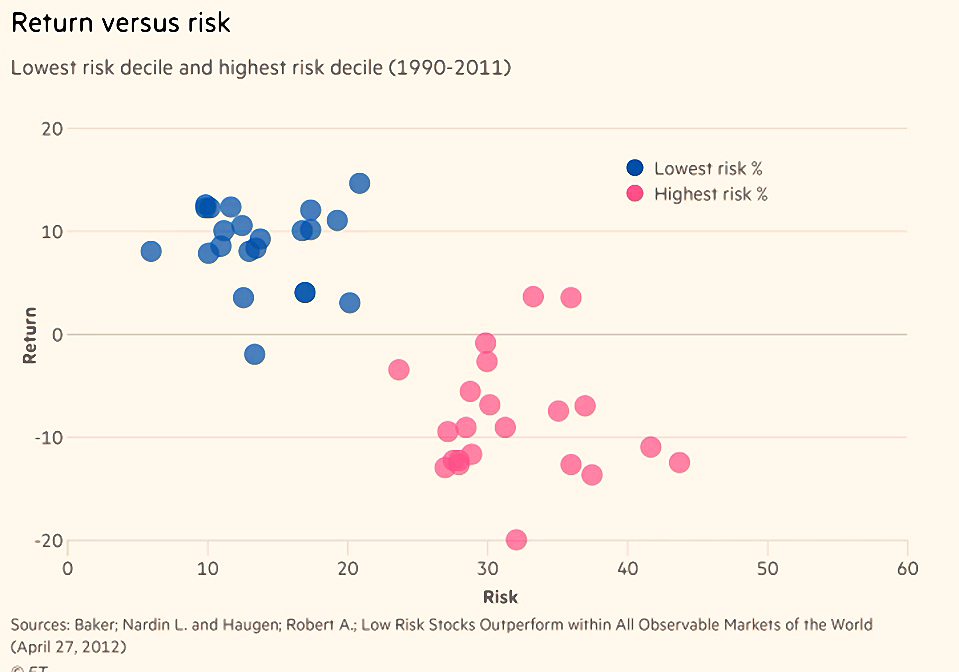

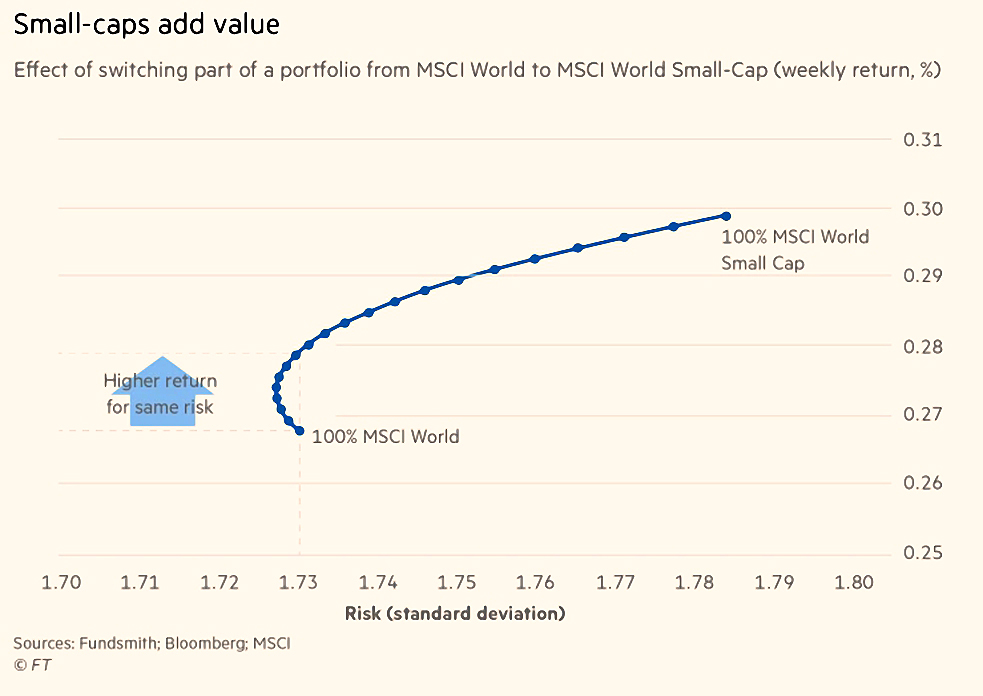

For the first one, Terry’s point was that low risk (low volatility stocks outperform).

- We’ve looked at the Low Vol Anomaly previously, and we try to make use of it.

The anomaly is clearly a blow for the Capital Asset Pricing Model (CAPM) which says that riskier stocks should have higher returns.

- But it’s still the case that between asset classes, the relationship between risk and return still holds.

Stocks have the highest returns, but they are also the “riskiest” (most volatile) asset class.

- If they weren’t, we would also hold 100% equity portfolios.

Terry also has a go at asset allocation, but for me he doesn’t quite convince.

- He makes a good point that business is more global than it used to be, and so geographical diversification might be less effective than previously.

This leads him to the conclusions that global funds are better than regional ones.

- Each to his own, I suppose, but I won’t be swapping my US, European and Asian funds for global ones.

Terry correctly stresses the importance of investing outside the UK, and in emerging markets in particular.

- And he identifies developed market small caps as the most useful third group to allocate to.

Add 35% of small caps to an MSCI World portfolio leads to a higher return for the same level of risk.

- This is good news, but I will be sticking with my own strategy, which uses allocations to rather more than just three segments.

Peak passive

John Authers wondered whether the US has reached peak passive.

- Passive index funds should always beat the average active because both groups sum to the market and passives have lower costs.

But a market that was all passives would have no price discovery or capital allocation (and indeed, no trades).

John points out that not much work has gone into finding out what point further increases in passives would make the market inefficient.

- This is strange, since inefficiencies created by passives should be exploitable – active funds could profit from them.

John draws a parallel with the Laffer curve (of tax receipts against tax rates).

- This has endpoints fixed by maths (both 0% and 100% tax rates would raise no tax), but nobody really knows the shape of the curve in between.

Vincent Deluard of INTL FCStone suggests that the US (which has more passives than anywhere else) may have reached the point where inefficiencies appear.

Since the are more indices than stocks, stocks – particularly large ones = are usually in more than one index.

- After controlling for size, valuations relative to book value increased with the number of index memberships.

- The effect on valuation relative to earnings and dividends was weaker.

Deluard also found that until 2017, more index memberships meant higher returns.

- But as more money has flooded into passives, the relationship has now reversed.

Similarly, stocks excluded from the S&P 500 (for limited free float, for example) used to underperform the index.

- Since 2016, they have outperformed.

Goodwill

The Economist looked at goodwill – the intangible balance sheet asset that covers the gap between the price paid for an acquisition and the book value of the acquired firm.

- Global goodwill totals $8 trn, compared to $14 trn of physical assets.

- Half of the top 500 US and top 500 European firms have more than a third of their equity in goodwill.

Goodwill can currently be written down if the acquisition is subsequently assessed as having suffered an impairment.

- Companies tend to splurge at the top of the business cycle and then do write-downs later.

A new value is assigned based on future estimates of cash flows and the difference hits in the income statement (as a loss).

- Cumulative write-off over the last ten years total $690 bn.

But now the International Accounting Standards Board (IASB) is thinking of changing the rules.

Current problems include:

- The difficulty and subjectivity of assessing the value of merged acquisitions

- The long delay before impairment shows up in accounts

- The lack of comparability between similar firms with and without a large amount of goodwill

The IASB has noted that lots of smart beta funds (factor funds) don’t account properly for goodwill.

One option would be to add all intangible assets on to balance sheets.

- But this (subjective) valuation of companies is the stock market’s job, not an accounting problem.

- Letting companies update their own value would be very messy.

A second option is to return to the old practice of depreciating goodwill over time (say with a percentage of a declining balance).

- The problem is that brands deteriorate at different (and unknown) rates.

- And since goodwill is not cash, the cash flows and the profits would diverge.

The Economist thinks that the IASB should leave things a they are.

If the objective is to assess a company’s prospective ability to service debts or create value for its shareholders, goodwill does not matter much at all and should be ignored.

Italian tax break

Earlier this year we look at Portugal’s Non-habitual Resident scheme.

- It’s a tax break for retirees who relocate to the country.

This week the Telegraph reported that Italy is considering a similar scheme.

- Southern regions of Italy suffer from chronic population decline.

The scheme would offer no taxes for 10 years.

- Initially it would only apply to Sardinia, Sicily and Calabria.

- You would have to live in Italy for at least six months per year, in a village of less than 4,000 people.

I’m still in the process of finding out about Portugal (which I’ve never visited) but I’ve been to southern Italy many times and I know I would like it there.

- So I’ll be watching the progress of this proposal with interest.

Quick links

I’ve got seven for you this week.

The first four are from FT Advisor:

- The Lib Dems want to create a secondary annuity market

- Hargreaves Lansdown are gunning for customers of financial advisers

- The Pensions Regulator has asked troubled schemes to cut their transfer values

- Opt-outs from workplace pensions have stayed low despite recent contribution increases

The next two are from the UK Value Investor:

And finally, Fortune Financial Advisors looked at The Inflation Advantage of Equal Weights.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.