Weekly Roundup, 6th August 2019

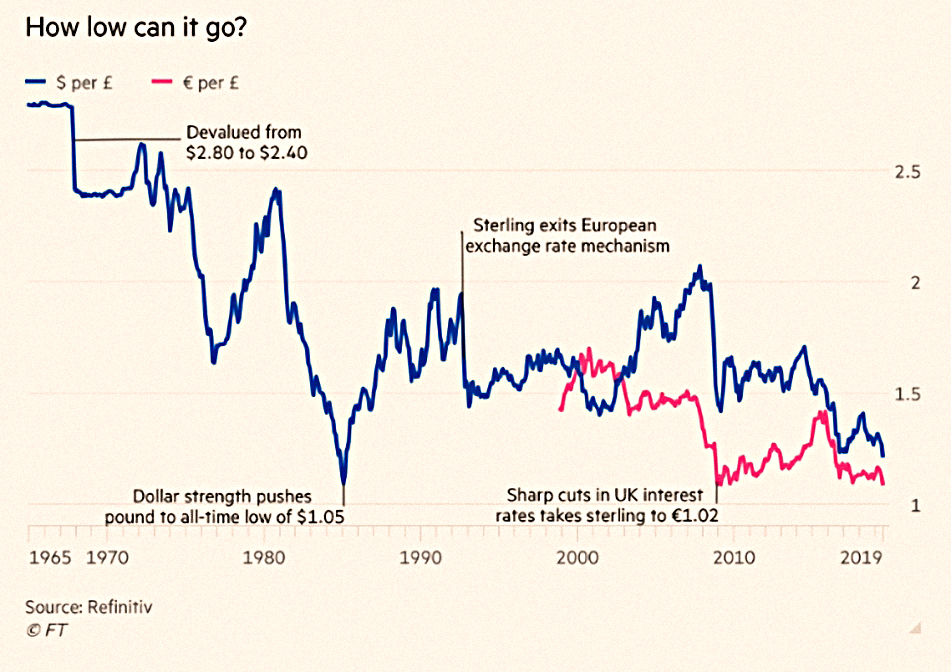

We begin today’s Weekly Roundup in the FT with the Chart That Tells A Story. This week it was about the exchange rate.

Sterling

It was another quiet week for financial news.

Claer Barratt (and a couple of her colleagues) wrote that sterling is taking a pounding.

- The prospect of a no-deal Brexit has led to a multi-decade low against the dollar.

The rate was lower in the 1980s, and lower against the euro as recently as 2009.

People get pretty worked up about this stuff, but as you can see from the chart, sterling has been weakening for my entire life, and I’m still here to tell the tale.

- I live in the UK and intend to continue to do so, barring Corbyn government.

So I spend in pounds, and how many dollars or euros they buy really only matters when I’m on holiday (with terrible timing, next month, as it happens).

- There’s also a bit of temporary inflation from more expensive imports, but we can live with that at the moment.

Despite my best efforts, my net worth is still 65% denominated in pounds.

- But that leaves 35% of foreign assets to cushion the blow of any devaluation.

Oil

Ken Fisher was back in the FT with his regular puff piece for stocks.

- This time he was discounting the potential impact of any oil price spike.

That would be down to Middle East tension, but equally, the trade war between the US and China could cause global growth to slow, pushing down the oil price.

In the last year, we’ve had four big swings in the price:

- up 26% in the autumn on US sanctions on Iran

- then down 40% in the winter as the global stock market correction led to recession and demand fears.

- then back up 48% by April, on more US-Iran tensions

- then down 20% on more demand weakness fears.

Ken thinks that Iran can’t impose a Gulf embargo on its own, and notes that even during the Iran-Iraq war only 2% of traffic was affected.

Nowadays we have shale production to take up the slack.

- And our service-industry driven economies use less energy in any case.

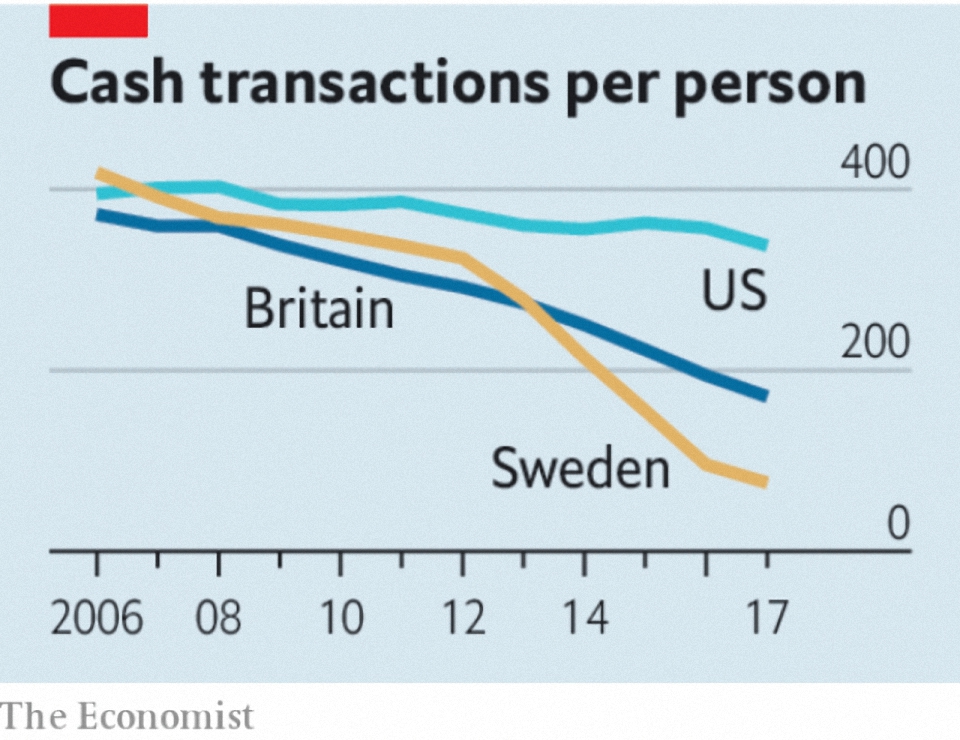

Cash

The Economist looked at the dash from cash.

- The move to digital payments will make economies more efficient but comes with problems.

Minting, sorting, storing and distributing [cash] is estimated to cost about 0.5% of GDP.

Electronic payments are cheaper in theory, but they allow banks and tech firms to charge fees as well as extract data.

- On the plus side, there should be less theft and tax evasion, and fraud should be easier to detect.

Cashless payments also make international trade easier.

- And transactions create credit histories for buyers, allowing them to borrow.

The downsides include hacking and cyberattacks, and the difficulty of including poor, old and rural citizens.

Rate cut

We finally got our rate cut last week, and John Authers wrote about it in his Points of Return email.

- The Fed made it clear that it was looking at the global economy as well as the US jobs market and inflation.

The next day, Trump duly obliged with a tweet signalling more tariffs on Chinese imports.

- Trump had wanted a 0.5% rather than a 0.25% cut, and putting more pressure on China was his way of getting it next month.

The markets now put the chances of another cut at 92%, and those of two more by the end of the year at 75%.

According to John:

The Fed is left haplessly in the role played by the European Central Bank during the sovereign debt crisis, or the Bank of England in the Brexit imbroglio, in that it has no choice but to offer insurance in the case that politicians do something

really stupid.Central banks become direct purveyors of moral hazard, and there is nothing they

can do about it.

Trump’s tweet has impacted the stock and bond markets, and also the price of commodities like oil.

- China has also allowed the yuan to fall to more than 7 to the dollar.

The big question is whether lower rates will actually stimulate the US economy in advance of the 2020 presidential election.

- Trump may need to pull a trade war resolution out of the hat before then.

Quick links

I have ten for you this week, the first five from the Economist:

- The foodoo economics of meal delivery

- More on the rate cut

- The LSE is buying Refinitiv

- The LME is the only remaining open outcry exchange in Europe

- Emerging market income dreams meet reality

- Flirting with Models looked at harvesting the bond risk premium

- Alpha Architect wrote about improving Low Vol strategies

- The FT reported that UBS plans negative interest rates for rich clients

- Tim Harford had lunch with Richard Thaler

- And Klement on Investing praised sub-optimal portfolios.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.