Weekly Roundup, 6th January 2015

We begin our weekly roundup as usual in the FT.

Contents

P2P developments

Judith Evans reported that Zopa plan to target the retirement market with an annuity replacement product based on P2P lending. The other main players (RateSetter in the loans to individual space, and Funding Circle and ThinCats in the loans to business area) are said to have similar plans.

Meanwhile Andrew Bounds reported that Assetz Capital have teamed up with International Finance Group of the US to offer a retail invoice finance discounting product which should return 5-7 per cent a year.

The product works by buying invoices from businesses at a discount in return for up front cash flow.When the invoices are paid (typically 60 days later) Assetz will receive the full value. The main existing UK providers of such products are MarketInvoice and Platform Black, which have minimum investments of £50K. MarketInvoice has reported typical returns of 12% pa.

These are welcome developments, and if tied to tax wrappers will make the sector a useful option for retirement planning.

Keep it simple

Jonathan Eley wrote about the need for simplicity in financial services in the face of the changing customer base. Old fogey enthusiasts like myself are in decline, and the majority now comprises time-poor individuals who find finance bewildering and/or boring. Cash ISAs and buy-to-let are the easiest and “safest” products for them to understand.

He makes three proposals:

- fewer products (there are 2000 open-ended funds and 400 investment trusts at present)

- one clear indicator of costs

- simpler literature

These are all sensible ideas, but they are not in the interests of fund managers, who want to confuse investors. We need regulation to decide what constitutes an “approved” retail fund, and we need to force individuals to engage with their financial future on a regular basis. Some hope of either of those wishes coming to pass.

Pension changes

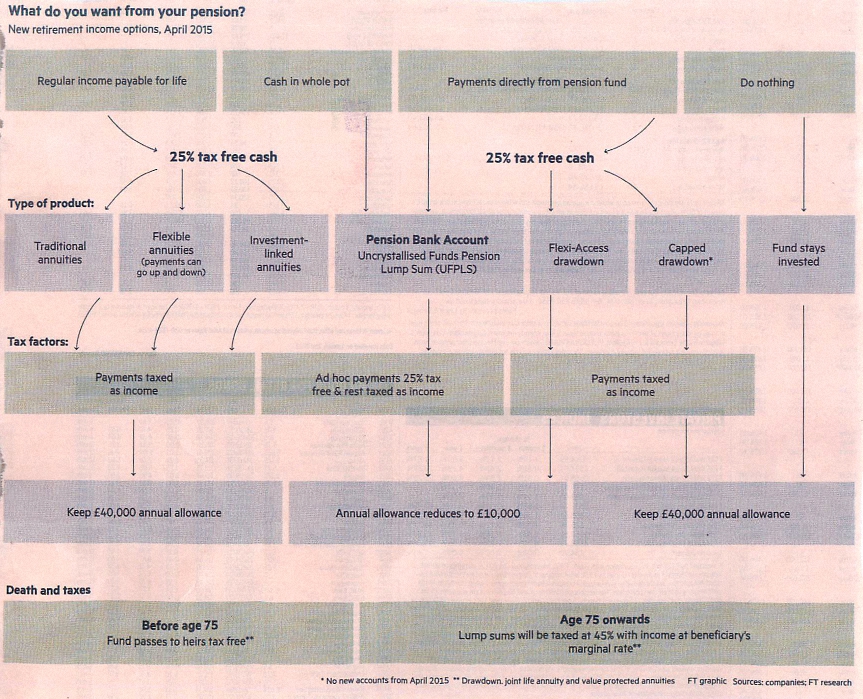

Josephine Cumbo wrote about the forthcoming pension changes. It’s a decent introduction to the subject for those who aren’t already aware, but I can’t help thinking that it over-complicates the situation. Take a look at the diagram below.

The main point of the changes to me is that you no longer need to buy an annuity, and that flexi- (uncapped) drawdown is available to everyone from age 55, not just those with a cushy £20K defined benefits pension to fall back on.

For anyone who noticed their retirement approaching, none of the other options should be required. The main thing to do before April is find out whether your current provider(s) will be offering flexi-drawdown and if not, work out the simplest and cheapest way to transfer to someone who does.

One important point concerns future pension contributions: flexi-drawdown reduces the annual allowance from £40K to £10K, but this is not the case if only the 25% tax-free lump sum is taken.

House price indices

In the “Chart that tells a story” feature, Kate Allen looked at the various UK house price indices. The traditional ones come from Halifax and Nationwide, and are based on mortgage data and their own definitions of a typical house. I’ve used them in the past and found them unreliable in the case of central London (perhaps because of the low reliance of these buyers on mortgages).

My own preference is for the Land Registry data, which appeared at a later date but now provides 20 years worth of data. The key limitation of this index ((though not for my purposes)) is the omission of new homes, since it relies on prices from repeat sales.

Kate introduced me to two new indices:

- the ONS ((I should have realised they would have an index)) which uses data from the Council of Mortgage Lenders

- and the LSL Acad index (set up by the FT) which uses Land Registry data as an input to its own model

I will be investigating these two indices before my next portfolio valuation. I hope that the data series will be long enough for me to consider using one or both of them alongside the Land Registry data. Kate also mentioned that the ONS has plans to combine its data with that of the Land Registry. If this comes to fruition, I may need to revise my methods once again.

More forecasts for 2015

John Authers counselled against viewing the future in one year sections. Despite current appearances, the chances are that in the longer term the rest of the world will outperform the US. Steady rebalancing in this direction would be a good idea.

Over 12 months, John sees three scenarios:

- US profits grow with low inflation, a strong dollar and continued cheap oil. Easy money supports Europe and China. Divergence deepens and a US bubble forms.

- US growth takes off, and the Fed raises rates. Wages rise and consumers keep spending. US profits are weak and stocks are flat. Funds move to the Eurozone and emerging markets, and the divergence slowly corrects.

- Financial crisis in oil-dependent states (starting with Russia), and money flows out of emerging markets. The Eurozone slumps and US confidence ebbs. US stocks fall.

Obviously the second option is preferable and may even be most likely with cheap oil (but not much cheaper than at present). We are in for an interesting year.

Rent controls

![]()

Over on her blog at MoneyWeek, Merryn wrote about the suggestion by think tank Civitas that private sector rents should be capped to inflation. She’s not in favour, and neither am I. Structural intervention in markets often produces the opposite to the desired effect. In this case reduced supply and poor maintenance are the obvious candidates.

Merryn would like to address the issue indirectly, by reducing the cost of housing for those people (particularly in the South) who would rather buy than rent, but can’t afford to. She discusses a few ways to do this before settling on the removal of interest rate offsetting against profits for buy-to-let investors.

This might scare off smaller operators who lack the scale to incorporate ((I presume Merryn doesn’t want to restrict relief for limited companies)) but it seems to me that it might equally just lead to even higher rents. People with assets need to receive a return on them, however they are taxed.

My personal view is that the market should set rents without government intervention. Supplying subsidised housing to 23% of the population seems meddling enough. If we want housing to cost less, we should either reduce demand ((find some way to slow or even reverse the relentless growth in the UK population, or persuade more people to relocate to the future “Northern Powerhouse” that George Osborne is so keen on creating)) or increase supply (build more houses).

Bond funds will go bust

Morningstar reported that that Bill Eigen has closed his long-only bond fund because he believes the sector will soon tank. He now runs an absolute return bond fund for JP Morgan and can short the market. As things stand, he is 55% in cash.

The only question with the bond market it seems is when. While central bank intervention remains so dominant, the answer would appear to be “not just yet.”

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.