Weekly Roundup, 7th August 2018

We begin today’s weekly roundup in the FT , with the Chart That Tells A Story. This week it was about inheritance tax.

Contents

Inheritance tax

We’re into August, and there’s very little of interest in the financial press.

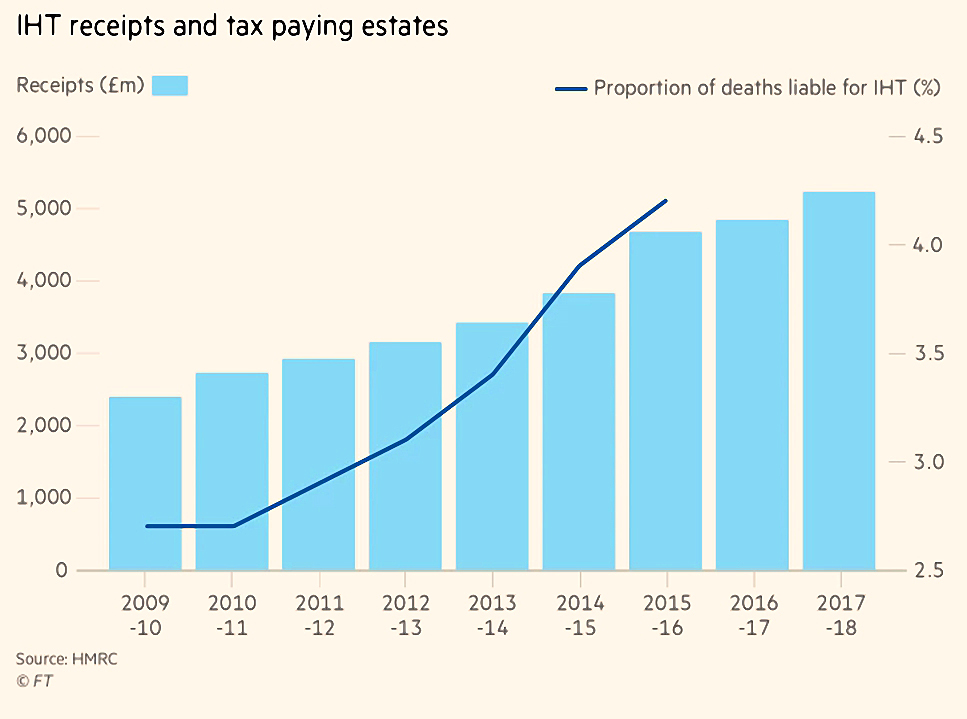

Kate Beioley reported that inheritance tax receipts have hit a record high of £5.2 bn for 2017/18.

- This is hardly surprising, given that the IHT allowance has been frozen at £325K since 2009, and more and more houses are now worth more than that.

The residence nil-rate band was introduced in 2017 and allows you to pass on another £125K to a direct descendent only.

- This will rise to £175K by 2020/21, giving a total exemption of £500K per person, or £1M for a couple.

- This new exemption means that IHT receipts could soon start to fall again.

Regular readers will know that I’m not a fan of IHT since it is applied to money that has already been taxed when it was received (income tax) adn will be taxed again when it is spent (VAT).

- I’m not alone, either – it’s regularly dubbed “the most hated tax in Britain”.

This is despite the fact that there are several ways to avoid it (see AIM below) and only 4% of estates pay it.

- When they do, though, its a tidy sum – the average bill is £179K.

The Office of Tax Simplification has been asked by Philip Hammond to take a look at IHT, and will report before the budget.

- I think it’s more likely that “loopholes” will be closed than that the nil-rate band will be increased.

AIM in ISAs

It’s five years since AIM shares were allowed in ISAs.

- The Business Property Relief that exempts AIM shares from IHt has actually been in place since 1995, but it was the ISA inclusion that greatly popularised AIM shares in general.

Ironically, our own AIM IHT portfolio is not held in an ISA for historical reasons.

Zero-cost trackers

It’s more than 40 years since Vanguard introduced the first retail index-tracker fund in 1975.

- This week, the regular focus on driving down the costs of these funds reached its logical conclusion, with the launch of the first zero-cost fund.

Of course, it’s only available in the US, and perhaps surprisingly, it comes from Fidelity rather than Vanguard, as the Economist reported.

- Shares in BlackRock, Invesco and State Street all fell.

Fidelity will make money from lending shares to short-sellers, and will hope to upsell other services (advice and more expensive funds) to investors.

- Low cost passive funds now hold close to 50% of US equity fund assets, and the trend towards lower costs can be expected to continue.

Let’s hope that zero-cost funds make it across the Atlantic at some point.

The twenty percent

[amazon template=thumbnail&asin=081572912X]

The Economist also reviewed Dream Hoarders by Richard Reeves, a book which argues that the upper middle class in the US are a bigger problem than the fabled 1%.

- Reeves defines the upper middle class as the top 20% of society.

Apparently, these people – “well educated, and hard-working, prudent savers and attentive parents” – are determined to hang on to their own prosperity rather than share it with others.

They hand on good genes, rear their children in homes rich in human capital, and provide the best of every educational opportunity.

This could only seem to be a problem to someone entirely unfamiliar with human nature.

- If only we had more people like these devils.

Interest rates

UK interest rates rocketed up by 50% this week, or by 0.25%, depending on how you look at it.

- They went up from 0.5% to 0.75%.

With inflation at more than 2%, the real rate is still massively negative.

- This is known as financial repression.

When interest rates hit 0.5% back in 2009 (close to the stock market low), I would take bet any amount of money that they wouldn’t stay this low for this long.

- It’s a good job that nobody wanted to take that bet.

Monevator did a bit of digging into the interest rate technicalities:

- r* (r-star) is the “equilibrium interest rate” – the “Goldilocks” rate than maintains inflation at the Bank’s target (currently 2% pa).

- R* is the “underlying trend rate” – what r* would be without the influence of short-term factors.

The Bank of England currently thinks that R* is currently between 0% and 1%, and that r* is lower than R*.

- Presumably, with CPI-H at 2.3% and the mid-range R* at 0.5%, the BoE believes that r* is around 2% below R*.

R* has fallen from a mid-range value of 2.75% since 1990.

- The 1990 value would imply interest rates of 4.75% pa (we actually had rates much higher at the time – 14.875%).

But at the moment, we can’t expect the Bank to raise rates beyond 2.5% pa.

Basic income

In the Spectator, Patrick Spencer of the Centre for Social Justice (CSJ) argued that Labour’s proposed universal basic income (UBI) wouldn’t help the poorest in society.

- My own objection to UBI is that it is unaffordable.

The CSJ reckons the poverty line is £16.3K ps (that will be news to anyone on the state pension of around £8K pa).

- A UBI at that level would cost £850 bn (105% of current government spending).

I wasn’t aware that Labour were proposing anything that generous.

- But even assuming a more modest £6.2K pa, Patrick points out that the current welfare system (Universal credit) provides £16.7K pa to a single parent with two children.

Another problem with UBI is accounting for regional variations in the cost of living.

Quick links

I only have three for you this week:

- Michael Johnson fears that collective DC (CDC) pensions could undermine the pension freedoms,

- Professional Advisor reported that people are taking advantages of the freedoms to the tune of a record £3.2 bn in 2Q18, and

- Dual Momentum reported on how momentum solutions can help in retirement (decumulation).

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.