Weekly Roundup, 6th June 2018

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about mortgages.

Contents

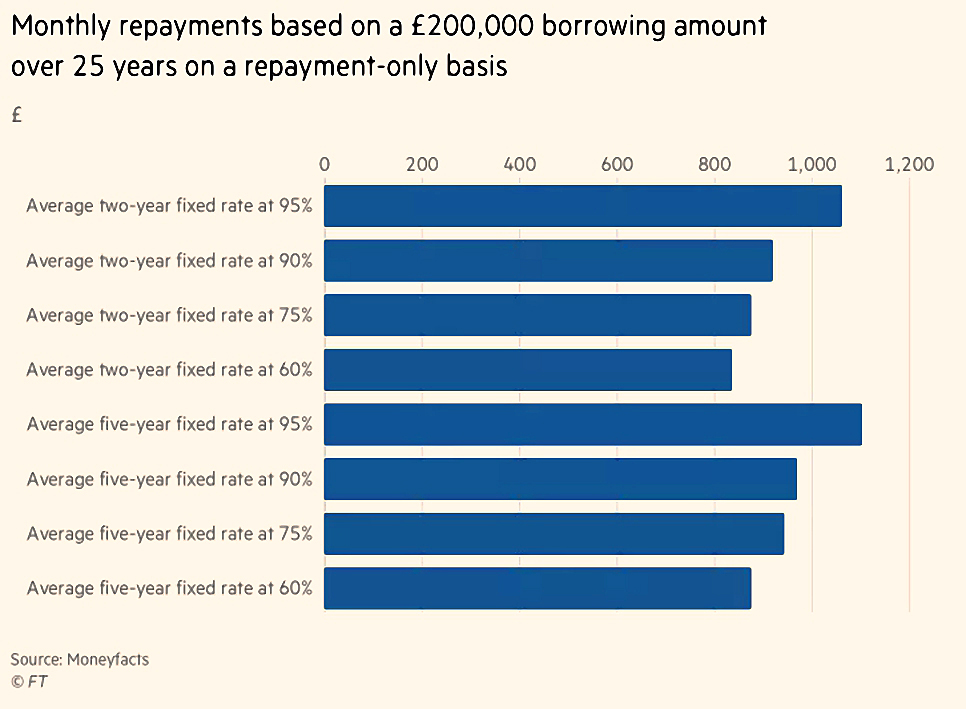

Loan to value

James Pickford looked at the cost of mortgages.

The chart shows the monthly repayments on a 25-year loan of £200 with two and five year fixes.

- For each loan, the repayment with a 95%, 90%, 75% and 60% loan-to-value (LTV) ratio is shown.

As you might expect, the larger your deposit, the less you have to pay in interest.

- I’m not sure what Story this Chart is supposed to tell.

Apparently the rate on 95% loans has fallen, but that’s hardly big news.

Failing forecasts

Tim Harford’s column was about forecasts.

He began by looking at how people flattered themselves when remembering their forecasts of what would happen during Nixon’s visit to China (way back in 1972).

- The paper written about these forecasts was called “I knew it would happen”.

Back in the 1950s, Paul Meehl demonstrated that checklists can beat expert opinion in forecasting (specifically medical diagnosis).

But economic forecasting is too complicated for checklists, or even for modern AI systems.

The “hybrid forecasting tournament” aims to explore how humans and AI can work together to produce better forecasts.

- The AI systems will have access to satellite imaging (crop growth, commodity stockpiling) and web searches (sentiment analysis).

Tim notes that falling conception rates precede economic downturns, as do negative lyrics in pop hits (Spotify streaming is a current area of analysis).

But he says that the best thing to do is to keep a diary of your predictions and beliefs, and “regularly revisit and reflect”.

Taxpayers

Kate Beioley reported that top earners are paying more tax.

- Those on the 45% tax rate paid £54.3bn in the 2016/17 tax year, up from £50 bn the previous year.

- That’s a 9% increase, compared to 1% more from the rest of us (£123.3 bn, up from £122 bn).

The main causes are the pension relief taper above £100K in income and the reductions in the LTA from £1.8M to £1M.

Destiny

Merryn’s FT column was about destiny.

Rwanda plan to sponsor Arsenal in order to boost tourism.

- They already make $50M a year from gorilla viewing permits.

- Per capita income has tripled over the past 15 years.

- And Western aid now forms only 17% of GDP.

Yet the tourism minister’s plan was ridiculed by the BBC.

- Merryn thinks that this is an example of what Hans Rosling called the destiny instinct.

- This is the idea that “things have always been this way and will never change”.

Much of Africa is now similar to the way that European countries were between 50 and 100 years ago.

Merryn thinks that the destiny instinct could lead you to invest too heavily in developed markets.

- She recommends frontier markets trusts from BlackRock. Aberdeen, Templeton and Ashmore.

- There also an iShares Frontier 100 ETF.

I don’t believe that Africa has a destiny.

- But I do believe that many of its countries have a problem with corruption and with property rights (look at last week’s reports of land stealing in South Africa for example).

- And I don’t have a 50-year investment horizon.

So there are other emerging (and indeed, frontier) markets that I prefer – Vietnam for example.

Merryn’s column in MoneyWeek noted that other people are starting to agree with the magazine’s way of thinking:

- Legal & General said that Help to Buy was distorting the UK housing market.

- An ex-member of the BoE’s Monetary Policy Committee said that low interest rates were now damaging the UK economy.

- UBS said that domestic focused UK stocks were undervalued.

- Events in Italy demonstrated that the country is a threat to the euro, and possibly to the EU itself.

Crowdfunding

Also in MoneyWeek, Ed Bowsher looked at equity crowdfunding platforms:

- Crowdcube

- This is the oldest platform – started in 2011.

- Minimum investment is £10.

- Successful firms include E-Car Club, Camden Town Brewery, Monzo and Revolut.

- Seedrs

- Started in 2012.

- Minimum investment is again £10.

- Uses a nominee model only, so that the platform can look after investor interest collectively (Crowdcube has the option of nominee or direct investment).

- Success stories include Revolut and Wealthify.

- Monthly secondary market at the prevailing market value.

- Syndicate Room

- Started in 2013.

- Minimum investment is £1,000.

- Uses a lead investor model for all companies.

- Technology and healthcare bias.

Other platforms include GrowthDeck, VentureFounders and Envestors.

- And firms like Startup Funding Club operate without a platform (via pitch evenings).

There’s also a site called CrowdRating which analysis many companies on the platforms and seems to be good at working out which will go bust.

- The Fantasy Equity Crowdfunding blog also provides news and views.

Ed’s been investing himself in dozens of the the EIS and SEIS companies on the main three platforms.

- He is disappointed that there haven’t been more successful exits to date.

With typically bad timing, Sugru, the moldable glue maker that had a valuation of £40M on Crowdcube, was sold for £7.6M.

- The 4,800 investors will get back just 9p in the pound.

Personally I’ve only put money in to a passive fund with around 30 investments, which came from Syndicate Room.

- I’m also planning to invest in a similar fund from Startup Funding Club.

And now Ed has whetted my appetite for DIY direct (or rather, nominee) investing of smaller amounts in multiple companies (Ed has invested in more than 60 so far).

- My average investment in a VCT is around £3K.

- For that I get access to probably dozens of companies.

So I would probably need to invest as little as £100 per company on the platforms to get a similar effect.

- The Syndicate Room fund worked out at something like £350 per company, so that might be used as an upper limit.

Another issue that needs more investigation is how the tax relief paperwork is handled.

- The Syndicate Room fund will issue a single certificate for the entire investment.

- Looking after a certificate for each £100 that I invest sounds like a lot or trouble.

Effective altruism

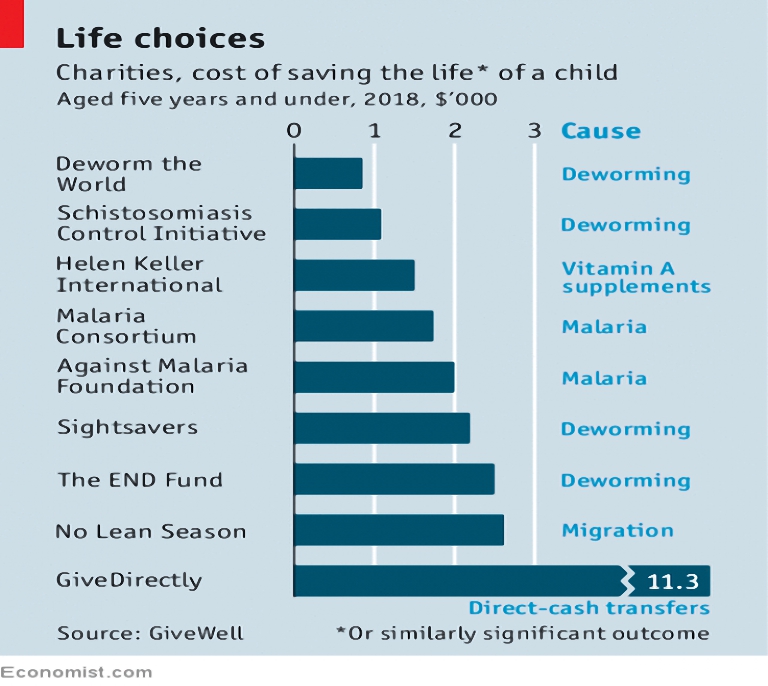

The Economist this week had a couple of articles on effective altruism.

The first looked at giving through the eyes of utilitarianism – the greatest good for the greatest number.

- GiveWell ranks charities by measures like cost per life, rather than the more traditional percentage overheads.

The benchmark for comparison is direct giving of cash to a recipient.

- Give Well recommends just nine charities, and the names on its list are not the best known ones.

Against such a framework, charities like the Make-A-Wish Foundation come out very badly – they spend $10K per wish and the recipients usually have terminal illnesses to begin with.

- At the other end of the scale, charities that work on deworming, malaria and vitamin supplements in developing countries can often save a child’s life for less than $3 (compared with $11 for direct giving.

Since each dollar raised by a particular charity leads to 50 cents less being raised by others, inefficient charities are having a net negative effect.

The problem with this analysis is the old adage “charity begins at home”.

- Many donors from rich countries want to help people that are more like them (and interestingly, animals that are not like them).

They might find volunteering at a local soup kitchen more emotionally satisfying than buying mosquito nets for strangers over the internet.

The effective altruism movement is popular only within a limited demographic – specifically, young white men with science and philosophy degrees.

The second article looked at the 80,000 Hours initiative from the Centre for Effective Altruism in Oxford.

- The idea is that high performers should take the most lucrative job that they can (investment banker, say, or plastic surgeon) rather than the one that does the most good directly.

- Then they should donate most of their extra earnings to charity, which will do more good than they would be able to personally.

The concept is known as marginal utilitarianism.

Sunk costs

The Economist also looked at sunk costs.

- It’s been known for a long time that people are unwilling to abandon failing projects into which they have already made significant investments.

- This is part of the reason why people don’t Cut Their Losses as they should.

It seems that not only do people take into account their own sunk costs, they also look at investment by other people.

Dr Christopher Olivola told 600 people they they had a front-row ticket to a basketball game on the day of a storm – attending would be cold, slow and possibly dangerous.

- It was too late swap the ticket or give it to someone else, but you could watch the game at home on TV.

There were four options for where the ticket came from:

- Either they obtained it themselves or it came from a friend.

- It either cost $200 or it was free.

Whether they or their friend paid, they were more likely to attend in person.

- Free tickets were easier to ignore.

Dr Olivola hypothesized that using a gift was part of demonstrating that you appreciated it (like wearing an Xmas jumper from a relative).

- But surprisingly, expensive gifts from strangers were even more likely to be used that those from friends and relatives.

Perhaps this exaggerated gratitude is the way that we turn strangers into friends.

Lessons from Vegas

Buttonwood looked forward to the the World Series of Poker, and concluded that for all but the most talented, a rules-based approach is best (in investing as well as poker).

In last year’s final hand, one player held A2 while the other held A8.

- With one card to come from 44 in the deck, A2 had only a 7% chance.

- He needed one of the other three 2s.

And since both players were “all in”, they each knew the odds.

- So A8 did the right thing when he called A2’s final bet.

But of course the last card was a 2, and A2 won.

Usually, poker players don’t know which cards their opponents are holding.

- There is uncertainty, along with betting and bluffing, aggression and greed.

And the same is true of investing.

- Nassim Taleb calls the idea that risk in financial markets can be calculated the ludic fallacy.

In truth, extreme events occur more often than you would expect.

Some people seem born to thrive on uncertainty, but for most, rules are best.

- In poker, this might be which starting hands you will play in each table position.

- In investment, it might be an asset allocation that you rebalance each year.

But just because rules make things simple, don’t assume that they make things easy.

- Investors are prone to do the wrong thing when events go against them.

Your own behaviour is often the hardest thing to master.

Buybacks

Schumpeter looked at the confusion around share buybacks, particularly in the US.

Buybacks have only been allowed in the States since 1992, but 97% of the S&P 500 have used them over the past decade.

- Of the $8 trn returned to shareholders during this period, more was via buybacks than by dividends.

There were $189 bn of S&P 500 buybacks in 1Q18, a new record.

- It was also a 41% increase on the same quarter last year, and represented 48% of gross cash flow (compared to a 10-year average of 30%).

- Most of the increase is down to 20-odd firms with large foreign cash piles.

Schumpeter believes that buybacks are a sensible tool that reflect economic imbalances rather than cause them.

He came up with six “muddles” about them:

- They are not “unnatural” but simply a more flexible version of dividends.

- Shareholders can choose whether to participate, and the level of cash returned can be increased (and switched off) without repercussions.

- They don’t create shareholder wealth.

- They can transfer wealth between those who participate and those who don’t (or the opposite, depending on the price paid).

- They aren’t simply used to increase the stock price or the earnings per share.

- Any temporary boost will be hard to sustain, since annual buybacks average 2% of the stock market’s valuation, and 1% of the value of shares traded.

- Three quarters of the largest buyers don’t use EPS in their pay plans.

- They aren’t an alternative to reinvestment.

- Large buyers typically have intangible assets (intellectual property) and could not reinvest the money usefully.

- They don’t lead to low investment.

- Investment is lower as a proportion of cash flow, but that’s because cash flow has risen relative to GDP.

- They don’t show whether corporation tax reform (cuts) were a good idea.

- The tax break was worth $100 bn so a better measure would be to see if investment rises by more than this (perhaps, at least in 2018).

More significantly, buybacks are usually a sign of peak optimism.

- The last peak was just before the 2008 crash.

Irish state pension

The Chief Investment Officer website reported that Ireland is looking at changing the basis of qualification for its state pension.

- They currently use the UK system, where time bounded (annual) contributions to a limit are used to assess entitlement.

They are thinking of switching to a total contributions basis.

I wish we would do the same:

- I have 41 years of contributions, many of which were paid against very high salaries.

- Yet because of the way the government has decided to treat the contracting out that they encouraged a few decades ago, they only count as 31 years.

Total contributions would be fairer, but it will never happen here.

Quick links

- Morgan Housel wrote a great (and pretty comprehensive) post about The Psychology of Money.

- Jon Boorman of Broadsword Capital wrote about Some Things He’s Learned Over the Last 30 Years.

- Flirting With Models (NewFound Research) looked at Seasonality Within Sectors.

- They also looks at how Dollar Cost Averaging Can Be Improved by Trend.

- Big Ern had An Idea For A New ETF (actually a pair of them).

- And the Economist looked at Wizz Air, a realistic challenger to RyanAir.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.