Weekly Roundup, 5th December 2022

We begin today’s Weekly Roundup with the looming recession.

Recession countdown

Sad news from Macro Alf, who is putting his newsletter behind a paywall from January 2023.

- In the meantime, he ran through what his leading indicators are telling him about the looming recession.

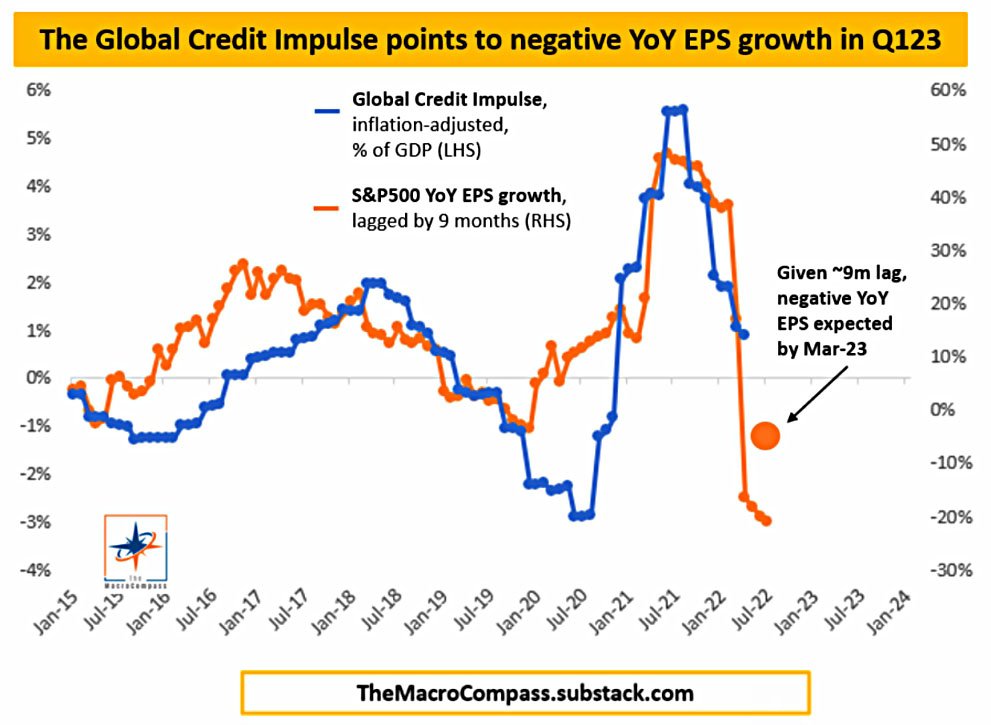

His flagship Global Credit Impuls index leads S&P 500 earnings growth by around 9 to 10 months and indicates negative YoY EPS by March 2023.

- Alf expects a 10% to 15% decline in EPS.

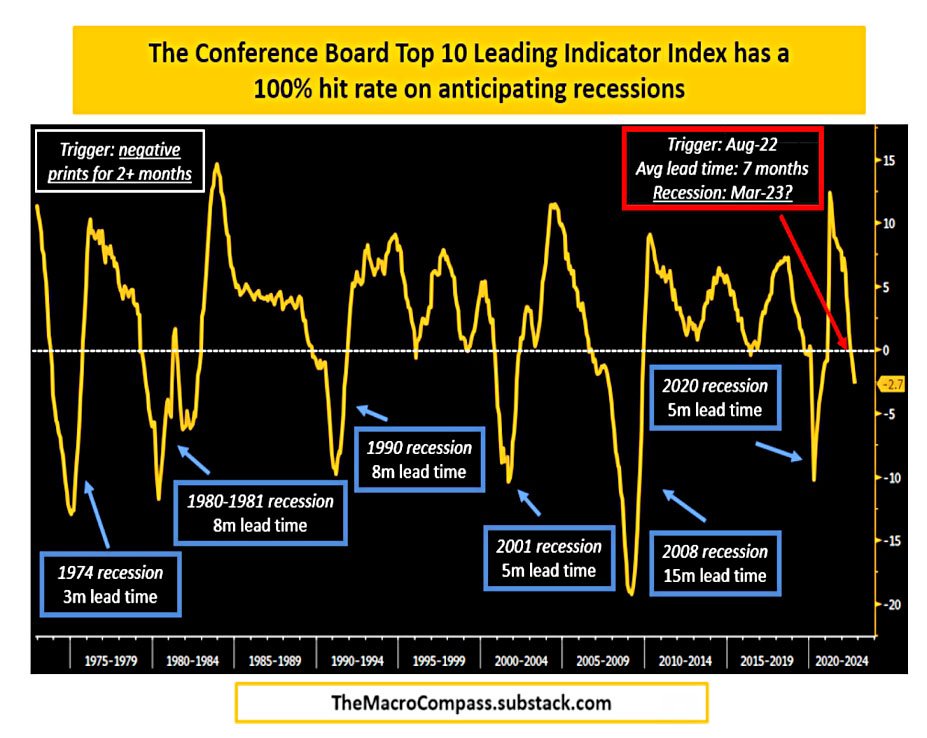

The US conference board leading indicators predict a recession after two months of negative prints.

- This happened in August, and the median lead time is 7 months, so again, we are looking at a recession in March 2023.

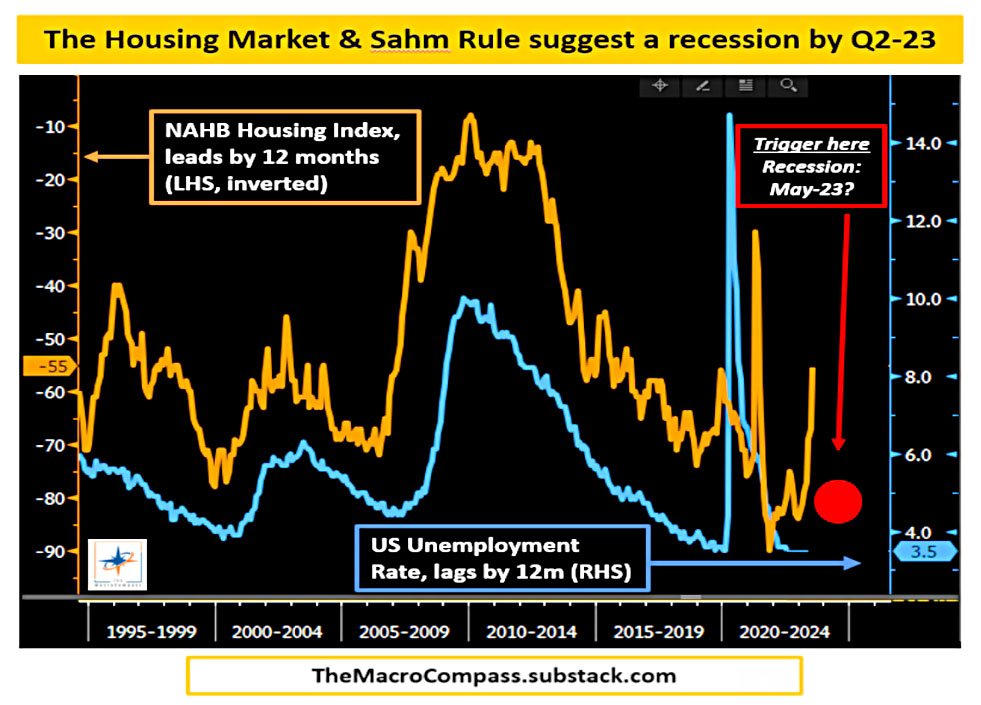

Housing-related jobs and economic activity represent anything between 12-15% of US GDP and employment, and the interest-rate sensitive nature of the real estate business makes it very prone to rapidly respond to changing economic and financial conditions.

The NAHB housing index leads US unemployment by around 12 months.

- The Sahm Rule predicts a recession when the 3-month MA of unemployment (U3) gets 50+ bps above its low of the previous 12 months.

The current target is 4.2% unemployment, which we should hit in 2Q23.

- By late 2023, unemployment could be above 6% or even 7%.

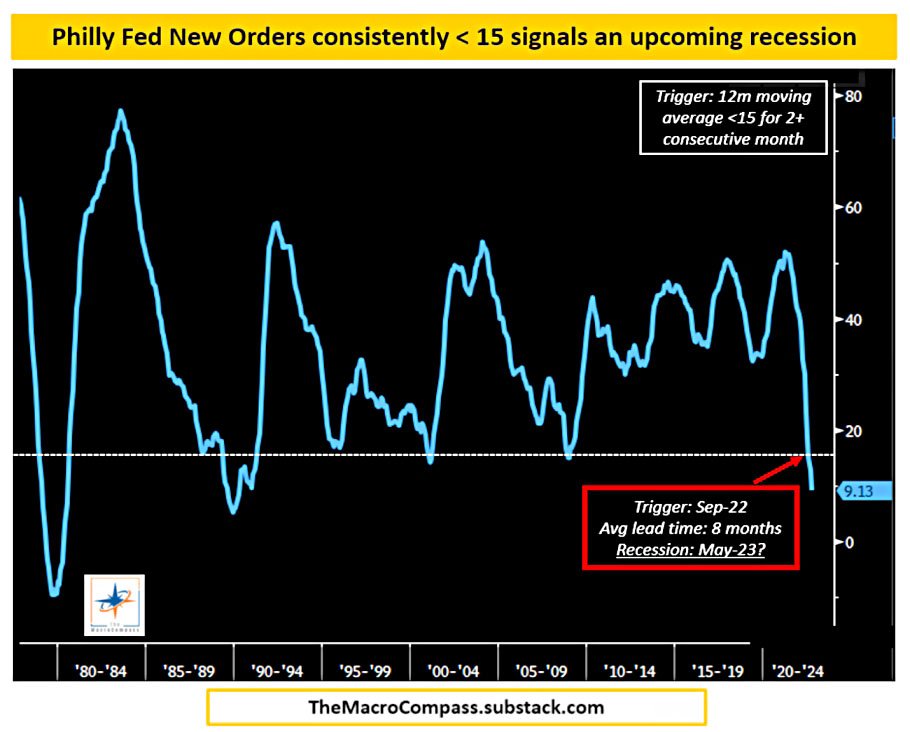

The Philadelphia Fed surveys 125 individuals, but these are Chief Executives of key companies and asks them to Forecast New Orders.

- When the 12-month MA drops below 15 for 2+ consecutive months, we always get a recession.

The trigger was hit in September, and the average lag of 8 months predicts a recession in 2Q23.

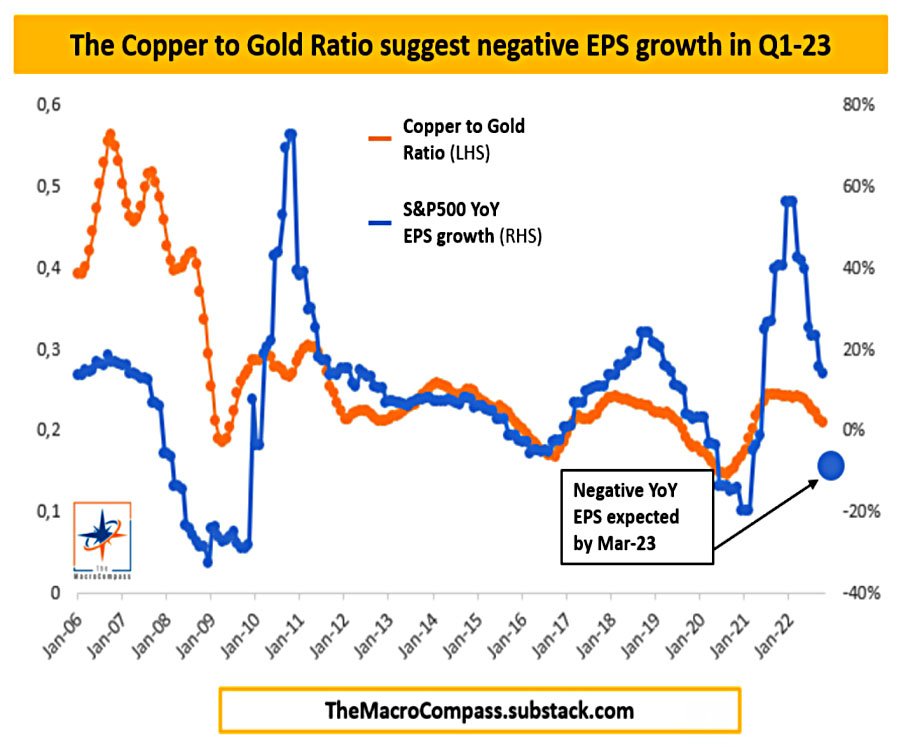

The Copper to Gold Ratio does a good job at telling us whether the real economy is set to deliver an acceleration or deceleration in growth.

This measure predicts that S&P earnings growth will head into negative territory by March 2023.

- Alf also notes that the yield curve has been inverted since April 2022, again pointing to a recession in 2023.

This is the broader definition of recession, including higher unemployment and negative earnings growth, as well as two quarters of negative GDP growth.

- So what asset classes do well in a recession?

Alf’s chosen model is the year 2001:

In 2000, the Fed hiked to 6.5% and took off the excess animal spirits in markets. In 2022, the Fed hiked to ~5% and took off the excess animal spirits in markets. In 2001, job market losses and earnings contraction followed.

Alf expects the Fed to pivot in 2H23, just as it did in 2001.

- The best assets to be in are bonds and the dollar.

Earnings

Joachim Klement wrote that the market is becoming less discerning.

Whether a company has good or bad earnings matters less and less for share prices and instead it is the overall market sentiment that drives a larger chunk of equity returns.

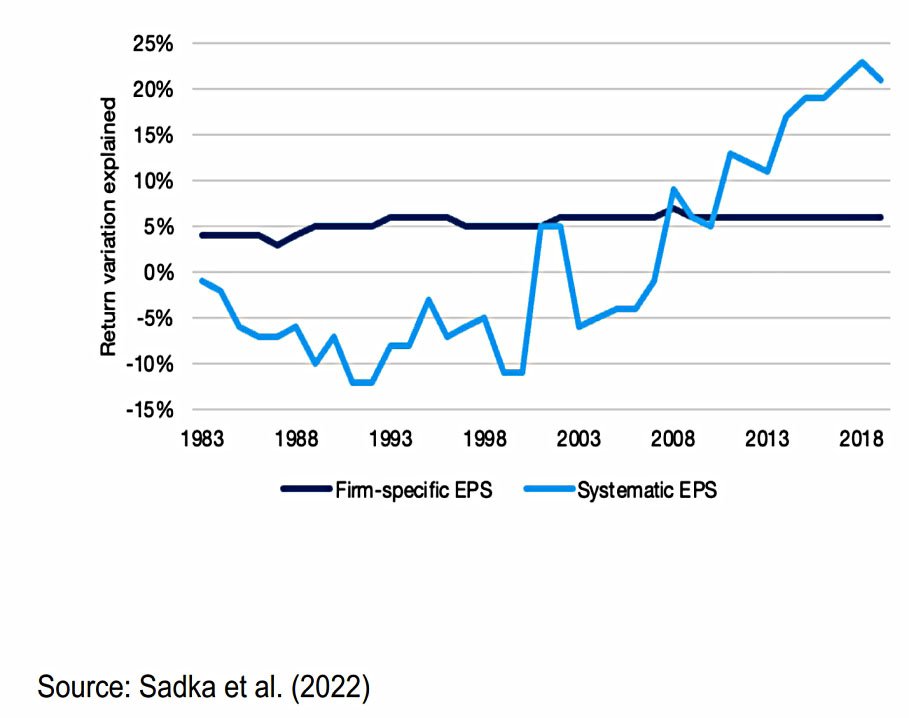

The study he looked at predicted returns for non-financial US companies based on the historic relationship between earnings growth and returns (using a 20-year regression of returns in the 12 months following earnings releases).

- Company earnings predicted only 5% to 6% of the variation.

Meanwhile, the market average earnings regression explained 20% of the variation.

- Before the 2008 crash, this contribution was usually negative.

Explanations include the increasing use of mark-to-market rules in accounting and the increase intangible assets.

- Joachim also suspects the rise of passive investing and commenters on the post also suggested the easy money (low interest rates) following the 2008 crash.

Dividends

Joachim also reminded us that dividend yield is not a reliable predictor of future returns.

Many investors still work under the assumption that dividend yield is a good measure of value and that stocks with higher dividend yields should outperform stocks with lower yields in the long run.

Yang Bei from the University of Missouri tested the predictive powers of many valuation measures.

- Over one year, the vast majority failed miserably.

- Joachim believes that valuation is still useful over 5 to 10 years.

Yang Bei has also tested dividend yields as a predictor in 17 countries over 150 years.

- Using in-sample regression of past data, five countries showed a significant relationship.

Using the out-of-sample prediction of future returns, only one country showed significant forecasting power.

- Luckily for us, that country was the UK.

Unfortunately, across 17 countries, one useful result is most likely down to chance.

Valuation measures are a poor predictor of one-year performance. If you are a value investor, you need to have a multi-year holding period.

Are things tight?

The Economist asked whether monetary policy is truly tight.

While some economists warn that interest rates have now risen by more than is necessary to contain price growth, others say that monetary policy has not really tightened at all.

The Taylor principle says that central banks need to raise interest rates by more than the increase in inflation.

- Otherwise, the real cost of borrowing will fall, providing a stimulus which should make inflation worse.

The widely-known Taylor rule says that real interest rates should go up up by more than half of the increase in inflation.

- But nobody is following the rule.

Since the start of last year inflation has risen by five percentage points in America, eight points in Britain and ten points in the euro zone.

No central bank is keeping up.

- The problem is that the Taylor rule looks backward, and real interest rates should be forward-looking.

We could use expectations instead:

- Subtracting US consumers’ expectations of 5.4% inflation over the next year from the Fed’s target rate of 4% gives -1.4%.

That is below the pre-Covid rate and not contractionary.

Things look better if we look further forward (and many loans are provided over many years).

The five-year real interest rate priced into financial markets has risen sharply since the start of last year, by 3.4 percentage points.

Harvard Professor Greg Mankiw worries that the Fed is overdoing things:

Mr Mankiw points to a three-point rise in annual wage growth—and real rates have roughly kept pace with inflation.

But the Taylor principle is a minimum, and more tightening is required in an overheating economy (as the US has at present).

- And both economic models and financial markets have underestimated inflation in recent months.

Perhaps central banks are right to rely on data and to slowly comply with Taylor.

- It all depends on whether you think that persistent inflation is more dangerous than a severe recession.

Gamification

The FCA has warned trading app firms against including gamification in their apps, as they risk tempting consumers into taking actions “against their own interest”.

- Things they have in mind include the famous Robinhood confetti on a stock purchase, as well as leaderboards, push notifications with market news and even default investment amounts.

The FCA surveyed 3,000 app users and compared their reported risk appetite to their investment choices.

- Twenty per cent of people were deemed to be “at risk” and 4% actually had “problem gambling behaviour”.

Separately, the CFA institute has recommended that apps move away from one-click transactions and focus reward and feedback systems on long-term outcomes.

- The FCA was even worried about features like copy trading, zero commissions and free shares.

CFA director Sivananth Ramachandran, the author of the report, said:

Gamification can be a powerful tool for increasing financial literacy and attracting new and younger audiences to investing. However, the techniques that are so adept at increasing user engagement are often leveraged to drive excessive or high-risk trading, or to encourage other harmful behaviours at the expense of investors.

He wants to see a warning on apps that excessive trading can harm financial health.

For Freetrade, Alex Campbell said:

Behavioural economics and design should be harnessed by companies to help support customers in making better long term decisions, not engage in speculative and harmful behaviours like day trading.

For eToro, UK managing director Dan Moczulski said:

There is no place for [gamification] in investing. [Copy trading is designed to help time-poor users to make more informed investment decisions, and for it to work properly, we need complete transparency when it comes to past performance.

I agree that gamification could affect a small number, but investing is for adults, and the responsible majority shouldn’t suffer in order to protect the vulnerable minority.

- It might be a good idea if gamification features could be switched off, but banning things would be a mistake.

Starling

Starling bank, which I use for both company and personal services, has decided to block transactions in and out of crypto platforms.

- I do have a tiny amount of direct crypto, but as far as I can remember, I used my regular current account to invest in this, and I have no current plans to repatriate it.

So it won’t affect me directly, but it’s an illustration of how the fallout from the FTX collapse has had on the relationship between crypto and mainstream finance.

- Plenty of banks banned crypto a couple of years ago, but Starling has decided this is a good time to break the bad news.

Starling said:

We’ve taken the decision to prevent all card payments to crypto merchants and to implement further restrictions on outgoing and incoming transfers. We recently tightened restrictions on inbound and outbound transactions by card and bank transfer.

The innovative technology, and thinking, behind cryptocurrencies has great potential advantages, however, right now, they are high risk and heavily used for criminal purposes and, as such, we no longer support them.

I can see why Starling wouldn’t want the hassle, but I’m not sure banks should be telling people where they can send their own money.

Quick Links

I have just three for you this week.

- The Economist looked at Microsoft, Activision Blizzard and the future of gaming

- Alpha Architect wrote about Trend Following and Relative Sentiment

- And Mauldin Economics said that The Economy Is a-Changin’

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.