Irregular Roundup, 23rd October 2023

We begin today’s Weekly Roundup with Dumb Money.

Dumb Money

Dumb Money, the movie about the GameStop saga, is now in the cinemas.

- I haven’t seen it, but a couple of people worth listening to have written articles about it, in the New York Times and the Wall Street Journal.

Richard Thaler (of Nudge fame) and Owen Lamont said that the movie exposes the baffling allure of Bad Investment Advice.

- For those who don’t remember, the movie tells the story of Reddit user “Roaring Kitty” who bought up a lot of stock /options in the failing video rental firm and then pumped it to his fans on the social media website.

Enough of his fans bought the stock that its share price soared, in part because of a short squeeze against hedge funds shorting the stock.

Thaler liked the film, but is worried by its potential effects:

Retail investors unfortunately behave in dumb, self-destructive ways. Their actions reflect overconfidence, financial ignorance and a wealth-reducing love of gambling.

Retail investors have a well-established track record of destroying their own wealth. Individual traders somehow have the opposite of skill — they manage to do worse than they would by picking stocks at random.

The harder that individual investors try (in the sense of trading more often), the more they lose. The best way for most people to invest in the long term is to hold a diversified portfolio of stocks.

The GameStop strategy was dumb (even if it worked out for some people, and led to the demise of hedge fund Melvin Capital).

- Thaler notes that an academic paper with the same title as the movie was previously written about the dot com boom when retail investors became wildly optimistic (or in a few cases, merely wildly premature) about the prospects for internet companies.

But in that case, the idea that the internet would (eventually) produce profitable firms was valid.

- Meme stocks like GameStop relied upon nostalgia and rooting for the underdog (plus hatred for billionaires) by bored young men stock at home under Covid lockdowns with stimulus cheques to burn.

Casinos and sports were disrupted by the virus, but Robinhood was offering commission-free trading and easy options.

Since GameStop, a suspiciously high number of other dumb things have occurred. We’ve seen bizarre price fluctuations of meme stocks that are in or approaching bankruptcy. One possible culprit for this wave of global dumbening is social media, by facilitating investor herding.

So if retail is the dumb money, who is the smart money:

The answer includes skeptics who can spot a company’s shortcomings and express their views by either selling their shares or betting that share prices will fall – short selling. Although “Dumb Money” depicts professional hedge fund investors as heartless villains , it would be wrong to think that selling short is inherently bad.

The “Big Short” movie paints a much more favourable picture of “underdog” shorters.

Cliff Assess of AQR says that he won’t be going to see Dumb Money.

The film is being hailed as a David-vs.-Goliath story, the little guy’s triumph over the Wall Street elite. That’s true only if you define triumph as a mob gleefully taking down one hedge-fund manager.

In fact, thousands of little guys (who bought too late, during the “moonshot” phase of the stock price rise) lost even more money.

The crowd of “little guys” was misled by deceptive or incompetent social-media hucksters into buying something that was very obviously overvalued.

Bed Bath & Beyond and AMC Entertainment are even worse examples of this than GameStop.

Cliff spots five themes from the meme phenomenon:

- People don’t like experts, even though they are usually right, and are much more likely to be right than a social media blowhard.

- The collective wisdom of professionals makes it difficult for any single investor to beat a competitive market.

- People think that instant access to a mass of information levels the playing field when it’s really about what you do with that data.

- Oceans of knowledge can lead to an illusion of control and understanding that collectively makes us dumber.

- HODL-ing through tough times is not always a good idea.

- Sticking with something through thick and thin works only if that thing is worth sticking to.

- Trading on hatred will hurt your bottom line.

- The wisdom of crowds only applies to independent thinkers (the Millionaire audience for example).

- Crowds that share information and come to a shared conclusion are often dangerous mobs. The internet seems to be a perfectly designed vehicle for turning a crowd of independent thinkers into an angry mob.

As we know, “the market can stay irrational longer than you can stay solvent”, but:

Even so, the rational usually win and the irrational usually lose. Moreover, when the rational lose, the irrational often end up losing too.

Cliff is not a fan of Hollywood:

Hollywood will happily take a situation it doesn’t understand and make a movie about it, replete with cartoon heroes and villains, which only lowers our discourse and intentionally makes us hate and distrust each other even more. Oh, and the same industry will do so for money while excoriating greed.

The movie also came up on the Compound podcast, where Downtown Josh Brown pointed out that a key antagonist in the movie – Citadel’s Ken Griffin – was the world’s most successful investor last year, making $4bn.

- So WallStreetBets were not the real winners.

Sequence risk

Joachim Klement wrote about sequence risk, which we’ve covered on the blog several times before.

- It’s usually referenced in the context of decumulation when you are a forced seller of risk assets at low prices after a crash.

But Joachim says that it applied to regular portfolios too.

- He imagines a portfolio that has a core of 80% S&P 500, and a satellite/flexible sleeve of 20% Nasdaq.

What would you do in 2000, when the Nasdaq starts to drop after years of strong returns?

- Would you hold on to the underperforming asset, or switch (say to international stocks)?

Over the 30 years since 1994, the average return on ten Nasdaq is 16%, compared to 10.8% for the S&P 500 and 6.6% for international stocks.

Sticking with the S&P 500 and Nasdaq portfolio would have a return of 11.8%per year over the last 30 years. Switching from Nasdaq to MSCI EAFE in October 2000 and staying there would have generated an average annual return of 11.2%.

But there’s a snag:

It would take until January 2018 to overtake the S&P 500 plus MSCI EAFE portfolio. For 17 years, you would have been better off switching.

Joachim advises switching to a new non-core holding every time the current one falls by 20%.

To this day, this simple switching strategy is ahead of a portfolio that would have stuck with the Nasdaq and averaged annual returns of 12.0%. Transaction costs would have been minimal with only six switches in the last 23 years.

So why does switching work?

Because assets that have underperformed for a while keep underperforming in the future. All too often I see both retail and professional investors hang on to underperforming assets.

We’re back to “Cut your losses” once again.

Boiling frogs

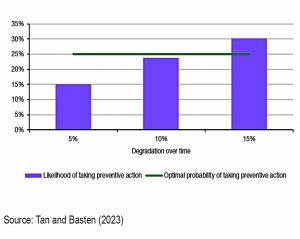

A follow-up article looked at an experiment to see what drives people to take preventative measures to avoid larger future losses.

Lijia Tan and Rob Basten [gave] people the task of looking after a machine. This machine has a certain probability of failure and when it fails, the machine has to be replaced or repaired at significant costs. To avoid failure of the machine, people can take preventive measures like a refurbishment of parts of the machine which costs much less.

There are two variables:

- how likely is a breakdown in the next year?

- how much damage will this cause?

In the experiment, the optimum refurbishment schedule was once every four years or a 25% chance of a refurb in any given year.

It turns out that the rate of degradation of the machine has a big impact.

We cannot see, feel, or otherwise experience the probability of breaking down or the costs of repairing a broken machine. But we can directly experience the change in themachine’s look and feel, i.e. how fast it degrades.

This is the boiling frog situation – slow changes are ignored.

- And the same applies to slowly degrading investments.

If the asset underperforms a little bit every month, quarter, or year, we are much more likely to give it another chance than if it drops 20% in one day. But by not taking preventive action on assets that underperform slowly we often rack up 20% underperformance by waiting.

IHT again

In the FT, Stuart Kirk argued that the debate around the reform/abolition of IHT overlooked the psychology of the situation.

- He noted that Russia, Portugal, Mexico and Canada each have no IHT, but that these countries have little else in common.

- Neither do Sweden, New Zealand, Norway, Australia, India or China have this tax.

As we saw last time, IHT is the most hated tax in the UK, although it applies to only 4% of estates and raises less than 1% of government revenues.

Stuart doesn’t buy the double taxation argument against IHT, as though the deceased has already paid tax on the money, the recipient hasn’t.

Another reason why inheritance and estate taxes are unpopular is that people know theyare wealth taxes by another name. And if a government can tax your wealth the moment you croak, why not a year before, or throughout your life?

But the key reason for the IHT hate is our desire for “symbolic immortality”:

We all yearn to live forever in the minds of our loved ones and beyond. Immortality is manifested in physical things. Maybe a photo, a favourite chair, the family home or a million-dollar trust fund. Assets handed down have psychic and emotional worth far beyond their monetary value.

He might be on to something.

Quick Links

I have eight for you this week, the first two from The Economist:

- The Economist asked Do Amazon and Google lock out competition?

- And explained How to predict the outcome of a coin toss

- The FT said that Cash is for emergencies, not portfolios

- And reported on Investment platforms under scrutiny over interest paid on customers’ cash

- Alpha Architect said that Momentum is Everywhere

- Discipline Funds wrote about The Broken Housing Market (That Isn’t Broken)

- UK Dividend Stocks said that The FTSE 250 is looking very cheap right now

- And Of Dollars and Data explained How to Invest During Times of War.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.