Weekly Roundup, 13th November 2018

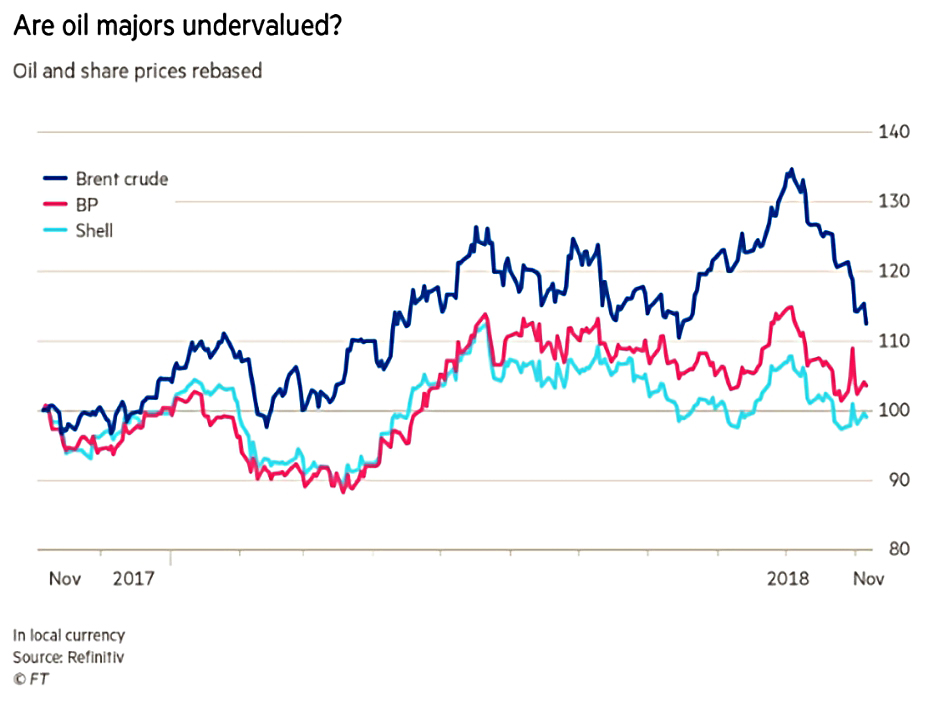

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about the oil majors.

Contents

Oil prices

Kate Beioley wondered whether Shell and BP might be undervalued, since their prices have not kept up with the rising oil price.

- Both companies share prices fell in 2015 and 2016 when the oil price fell.

- Since then they have cut costs and boosted profits and earnings.

Their prices have risen but not as much as the oil price.

BP in particular looks like good value on two important metrics. One is the company’s current enterprise value to cash flow from operations, which stands at 5.3 for its full 2019 year.

On that metric BP is better value than Chevron, Exxon Mobil and Total among others. BP is also trading on the lowest multiple of enterprise value to debt adjusted cash flow of any of the supermajors.

The key risks (apart from a falling oil price, which is happening at the moment) are that demand for oil set to increase more slowly in the future, before eventually falling back.

- And increased competition from renewables means that existing reserves might never be used up.

On the plus side, both groups are solid dividend payers.

Life begins at 60

Merryn thinks that life now begins at 60, and that we need to adjust to this.

She begins by discussing how difficult it is to make decisions about DB pension transfers, transfer of assets to escape IHT, and equity release.

- What they have in common is that you can’t know in advance whether you have done the right thing, since you don’t know how much longer you will live for.

In general, people underestimate how long they will live for, with those who make it to sixty having a good shot at 90.

- The over 50s are healthier than previous generations, and are spending more.

For Merryn, it is middle age that is getting longer, not old age.

Yet it’s had to change your career over 50, or even stay in your original one past 65.

- And education for most people ends by around age 21.

The median pound in the UK is spent by a household headed by a 47-year-old. But advertisers remain fixated not on them but on Generation Y (born between 1980 and 1995).

She pointed us at a Longevity ETF, but it’s US-listed.

Coming back to finance, the industry still tries to “lifestyle” you into bonds once you hit 50, even though you might live for another 40 years.

Merryn wants to see:

Systems where people can dip in and out of education over a lifetime and are better able to change careers, and hence find ways to let even those in their 80s be productive, valued members of society.

Hear, hear.

Equities vs bonds

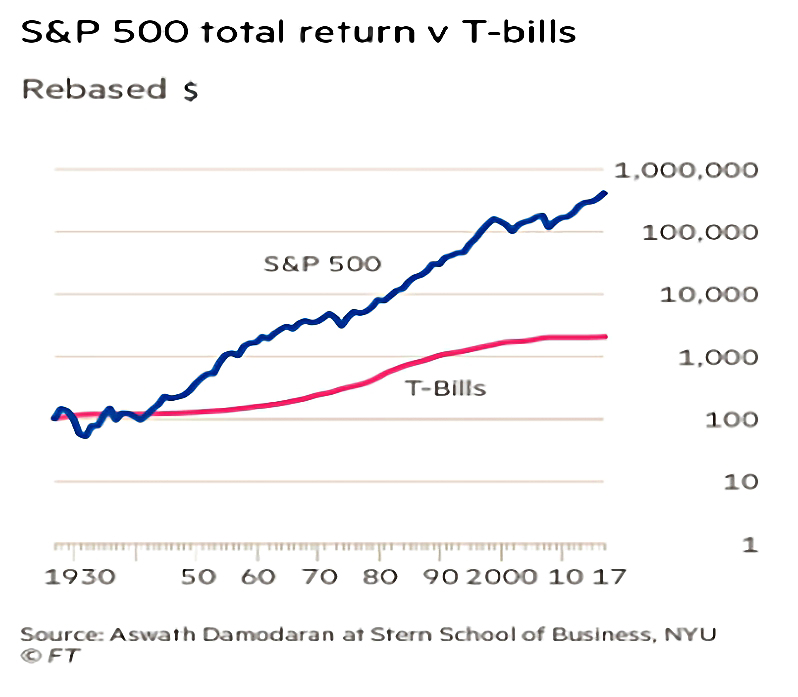

As luck would have it, Terry Smith wrote about the Bessembinder Report just a few days after I did.

His article was the latest in his series on “busting the myths of investment” and asked “Do equities outperform bonds?”

When focusing on the stocks’ return over their full lifetime as quoted entities, up until the end of the period or delisting — essentially a buy-and-hold strategy for all stocks — [Bessembinder] found that only 43% of stocks exceeded the return on one-month Treasury bills, even with dividends reinvested.

Of course, stocks as a group do outperform.

Large positive returns from a few stocks offset the modest or negative returns from the vast majority of stocks.

Bessembinder also looked at returns by decade:

The decade returns for most equities are lower than those earned by investment in Treasury bills. Moreover, the results have been getting worse.

Of the stocks floated between 1947 and 1956, 87% had higher returns than US Treasuries. This fell to just 31.7 per cent of those floated from 1977 to 1986.

The median stock entering the market since 1977 did not just underperform Treasuries but had a negative return.

Unusually for an active manager, Terry draws the right conclusions from the report:

Most active investors are doomed to underperform not only the equity indices but also bonds. If you are not confident you can identify the few stocks which outperform, then just buy the index.

But he squeezes in a soft sell for his own approach:

The returns from active stock selection can be large if the investor selects a concentrated portfolio of the few stocks which offer positive returns.

That’s easier said than done.

- The low hanging fruit would seem to be the avoidance of the under-performing stocks, which should be a bit easier.

Of course, you could combine both strategies.

Stock pickers

Michael Mackenzie was also pushing stock pickers, along with “credit pickers”.

The return of market volatility as central banks steadily remove the security blanket of easy money should represent good news for active managers and macro-based investors.

A world riven with divergences among markets and regions is just the type of febrile environment that warrants paying a higher fee for a more active approach to investing.

As Michael points out, the past decade of QE has been good for passive investing.

- In contrast, we could be looking forward to a period where stocks and bonds slide together.

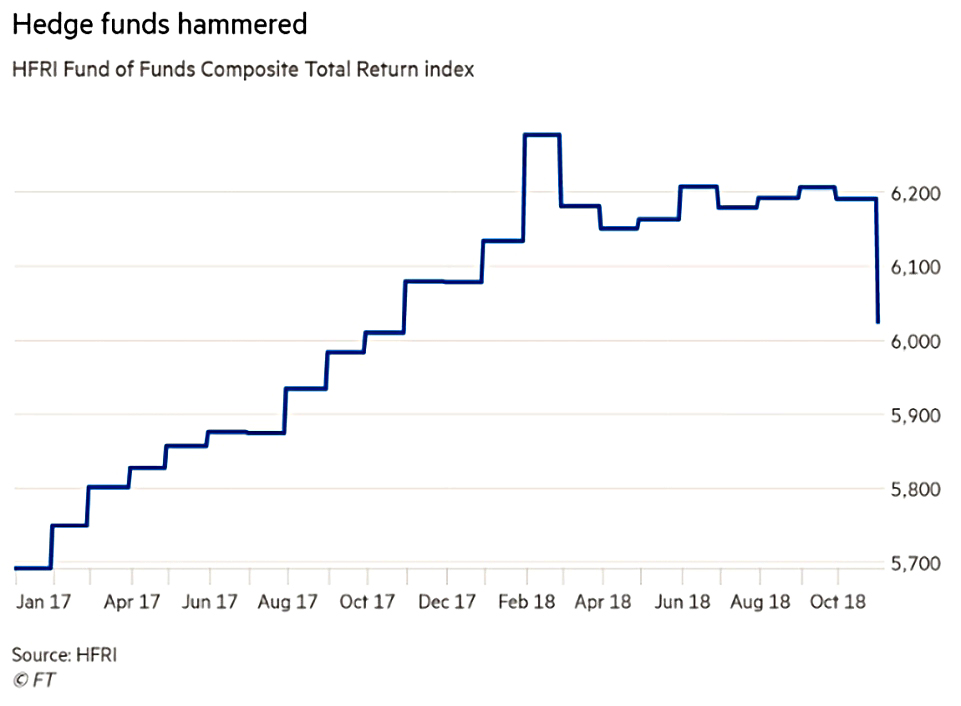

Hedge funds could be a smart investment, but most have done badly:

The scale of pain for the long/short fraternity last month, with an average loss in the region of 7.5 per cent according to prime brokers at major banks, clearly indicates that many funds were betting a lot more on stocks rising rather than striking a better balance.

It looks like a lot of the fund were simply “long tech” – a crowded trade set to end badly with a stampede to the exits.

They’ll need to do better in the future.

Low vol

Over in MoneyWeek, John Stepek wondered whether rising interest rates might kill off the low vol anomaly.

Low vol stocks have outperformed over the last 25 years, in contrast to what the efficient market hypothesis might suggest.

- The EMH predicts that “riskier” / more volatile stocks should have higher returns.

The sectors that dominate in low-vol portfolios – accounting for more than half of the value of the stocks in these indices during the period under examination – are property and utility companies.

These are high yield sectors that are particularly attractive when interest rates are low and moving lower still.

- When yields rise, the prices of these “bond proxies” might fall.

Probate fees

The government has confirmed that probate fees will soar, albeit by less than an earlier draft paper had suggested.

- The maximum fee will rise from £215 to £6,000, rather than the £20,000 initially proposed.

- This is still an increase of almost 4000%.

Under the new rules – which could apply from April 2019 – fees are to be tiered, with nothing to pay on estates below £50K.

- Below £300K there is no IHt to pay, but probate will now cost £250.

From £500K to £1M the fee is £2.5K.

- Estates over £2M will pay the maximum £6K.

The government has stated that fees will never be more than 0.5% of the value of the estate.

Since the amount of work involved does not increase with the value of the estate – and does not cost anything close to £6K to carry out – this is in effect an extra bit of inheritance tax.

- It would appear to have been left out of the recent Budget in order to attract less attention.

Pesky KIDs

In the Times, Holly Black noted that Key Information Documents (KIDs) for some funds may be misleading.

- The Unicorn AIM VCT is ranked 3 on a risk scale that runs up to 7.

That means it is “low to medium risk” and “unlikely” to lose you any money.

Of course, the trust – which I hold myself – invests in AIM stocks, which are fairly high risk.

The KID also says:

Even in “unfavourable” stock market conditions, the fund is expected to deliver 11.3% a year over the next decade. In “favourable” conditions, that return leaps to 19.6% a year.

The new KIDs are based on European legislation and have applied to ITs (which include VCTs) since early this year.

- ITs and ETFs that haven’t updated their KIDs to the new standard usually can’t be traded by private individuals.

The predictions in these documents are based entirely on how the fund has performed in the past few years, a period when stock markets have posted new record highs. The forecasts have been branded “wildly optimistic” by the AIC [Association of Investment Companies].

Insider sales

John Authers’ newsletters from Bloomberg have started to turn up in my inbox (they are called Points of Return if you want to sign up).

The first section that caught my eye was on insider sales.

- Insider buying of shares (especially in size) is almost always a good sign.

Insider sales are usually thought to be less significant, since there could be any number of “good” reasons to provoke a sale (eg. buying a new house).

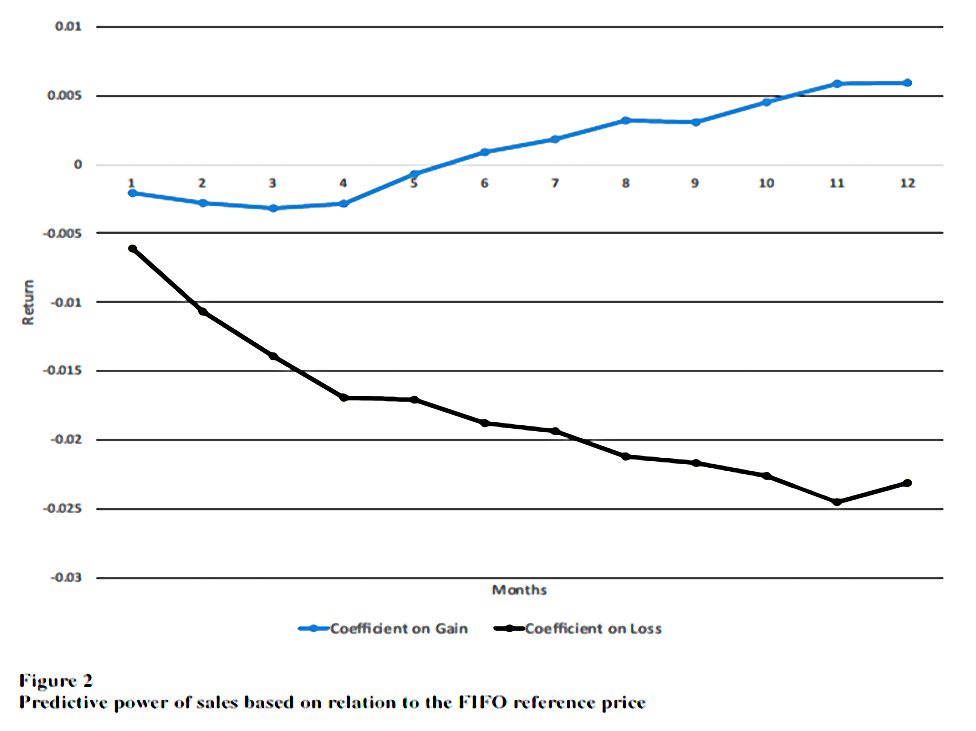

Peter Kelly of the University of Notre Dame’s business school used “first in, first out” (FIFO) accounting to work out whether shares had been sold for losses or gains.

Peter Kelly of the University of Notre Dame’s business school used “first in, first out” (FIFO) accounting to work out whether shares had been sold for losses or gains.

Sales for a loss imply that very bad things are about to happen to the share price.

People hate taking a loss and will go to great lengths to avoid doing so. You are admitting that your previous decision to buy it was a mistake, and that you are abandoning hope of recovering.

What the Fed didn’t say

John’s second piece was about what the Fed didn’t say after its decision to hold interest rates as they are.

He provided a list of things the Fed chose not to mention:

- October’s stock market turbulence.

- The ongoing emerging-market crises.

- The U.S. housing market, which is showing clear signs of weakness.

- Oil, which has now fallen more than 20 percent peak to trough (and which will therefore bring inflation down with it).

- The dollar, which is strengthening again.

Any of these might have provided an excuse not to raise rates again next month.

- It seems that the strike price of the “Powell put” (when the Fed will intervene to stop declining asset prices impacting the wider economy) is a lot lower than the current price of US stocks.

Quick links

I have seven for you this week, with the first three coming from The Economist:

- The growth of micro-brands threatens consumer goods giants.

- Billboards are old but booming.

- The struggling care-home industry is an unlikely hit with investors.

- The Adventurous Investor looked at three alternative finance platforms that are making waves.

- The Irrelevant Investor looked at how our early memories shape our attitude to the stock market.

- Flirting with Models looked at How to Measure the Benefit of Diversification, and

- O’Shaughnessy Asset Management looked at Alpha within Factors.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.