Weekly Roundup, 1st March 2021

We begin today’s Weekly Roundup with a look at bonds.

Bonds

John Authers noted that Buffett’s Annual letter – out over the weekend, we’ll have more on this in a future post – contains a blast at bonds:

Bonds are not the place to be. The income recently available from a 10-year U.S. Treasury had fallen 94% from the 15.8% yield available in September 1981. In Germany and Japan, investors earn a negative return on trillions of dollars of

sovereign debt.

John notes that stocks may appear cheap relative to bonds, but that’s because bonds are so expensive.

After just two months, 2021 is the third-worst year for bonds since 1988.

After moves like this, things usually get worse, but John is not convinced:

It is possible that last week saw a peak in the excitement over the reflation trade. It will take much more to confirm that. But having come a long way in a hurry, the market has come to a convenient point to pause and gather evidence before going any further.

Inflation

John Mauldin had a great chart (courtesy of Gavekal Research) showing that the S&P 500 (or equivalent) has made no gains under inflation over the last 140 years.

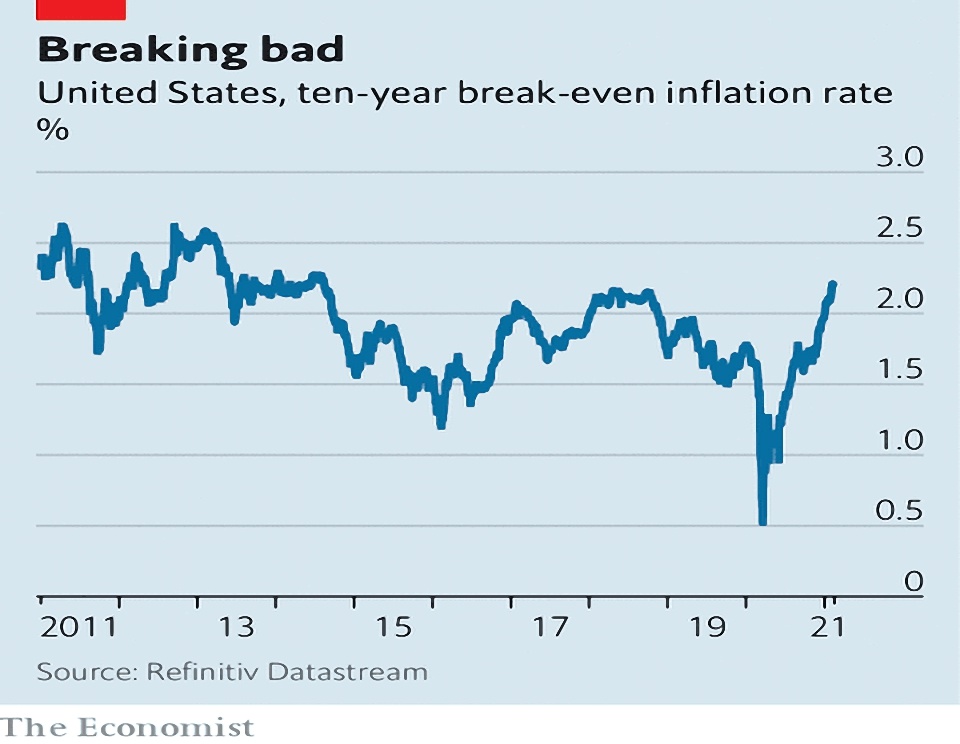

Meanwhile, the Economist said that the popular market break-even gauges are too volatile to be a reliable guide to inflation fears.

The yield gap between ten-year Treasury inflation-protected bonds (TIPS) and conventional bonds of the same maturity is widely seen as a measure of long-term inflation expectations. These inflation “break-evens” have soared to 2.2%.

But it appears that they cannot be relied upon:

In America, the oil price appears to have an outsize influence on break-evens. A model based on the oil price and the dollar tracks market measures of expected inflation quite closely, according to Steven Englander of Standard Chartered.

Sharp rises in the oil price tend to push up inflation, but the effect is temporary. They ought not to influence medium-term break-evens, but in practice they do.

The price of treasury bonds through crises also has an impact.

- After a crisis, the yield curve steepens, as do break-evens.

But this is mostly the outcome of shifting attitudes to risk, rather than forecasts of inflation.

Stocks are risky

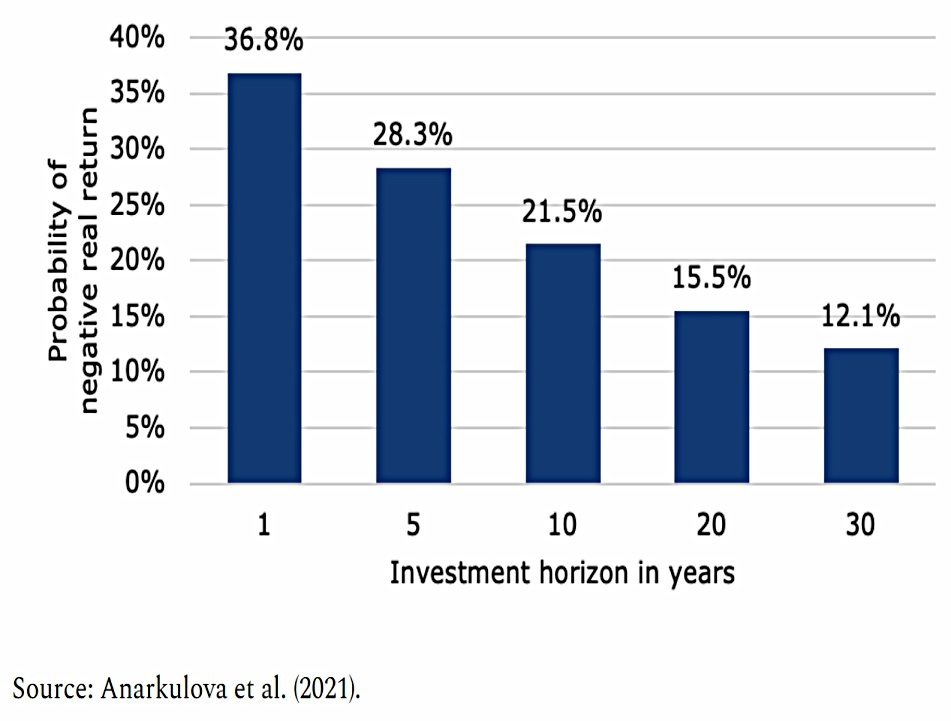

Our Klement catchup continues with an article on the fact that although stocks become less risky over time (less likely to produce a loss after inflation), they remain riskier than many people think.

This is largely down to bias from the US and the UK.

Not having seen their home territory destroyed in any war over the last century or more has certainly provided a big advantage to the stock markets in the United States and the UK. But in general, political stability and the rule of law have helped even more.

Maximum drawdowns are also better in the UK and US:

The biggest monthly drop in the UK in real terms was 26.9% and in the United States 29.5%. Be glad you weren’t investing in Australia (biggest monthly decline ever recorded -42.5%), Belgium (-55.9%), Japan (-87.2%), or Germany (-91.1%).

Swift recovery

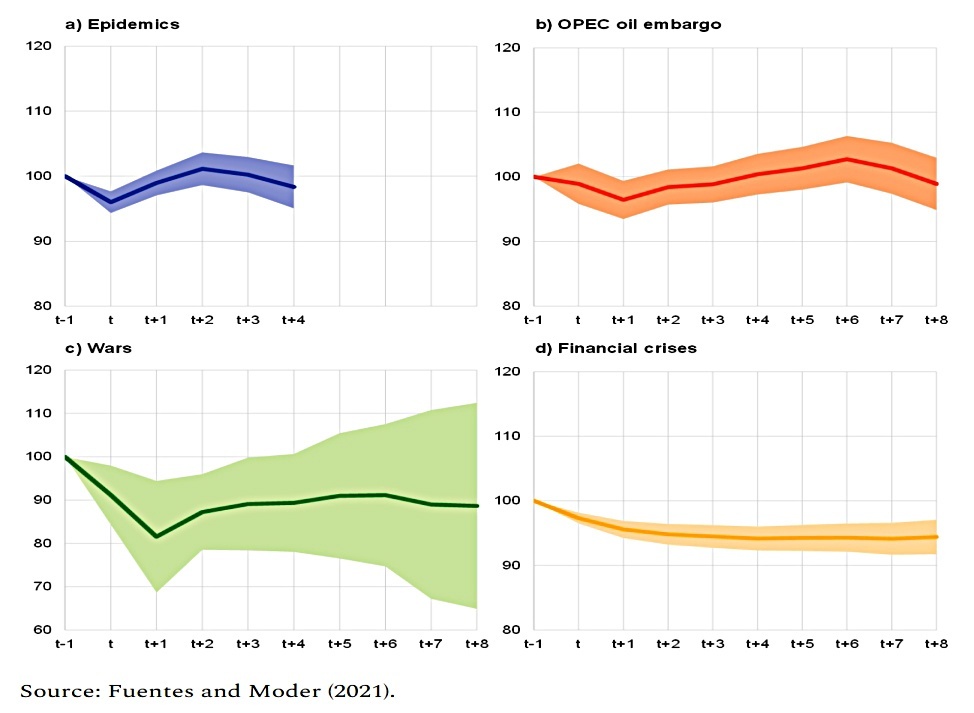

Joachim’s second article suggested that we might have a rapid recovery from this pandemic, as seems to be the case so far.

- A recent study looked at shocks in 117 countries from 1970 to 2017.

Recoveries from epidemics are much quicker than those from financial crises – usually within two years.

Bitcoin

The Economist noted that bitcoin has fallen more than 20% from its $58K high (perhaps not coincidentally after Elon Musk tweeted that its price “seems high”.

- Another factor might be that Tether has been fined by New York regulators.

We covered the problems with Tether last month.

A concern is the degree of control that Tether’s owners have over supply. Whereas only a fixed number of bitcoin are available to be “mined”, Tethers can be issued at will, giving those behind the stablecoin central-bank-like printing powers.

This leads to suspicions that unbacked Tether issuance is behind bitcoin price spikes.

A recent analysis found that the majority of bitcoin purchases on several crypto-exchanges, including Binance, Bit-z and Hitbtc, are made using Tether. More than two-thirds of all bitcoin bought on all crypto-exchanges in one 24-hour period studied were purchased with Tether.

Now NY attorney-general Letitia James has fined Tether $18.5M and told them to stop trading with New Yorkers.

- Unfortunately, the settlement allows Tether and the associated crypto exchange Bitfinex to avoid admitting any wrongdoing.

They have had to agree to more transparent reporting though.

JP Morgan has spelt out the risk:

Were any issues to arise that could affect the willingness or ability of both domestic and foreign investors to use Tether, the most likely result would be a severe liquidity shock to the broader cryptocurrency market.

Interestingly, the bank also advised clients to allocate 1% of their portfolios to bitcoin. Strategists Joyce Chang and Amy Ho said:

In a multi-asset portfolio, investors can likely add up to 1% of their allocation to cryptocurrencies in order to achieve any efficiency gain in the overall risk-adjusted returns of the portfolio.

This contrasts with previous statements from the bank that as crypto became more widely adopted, its ability to hedge against equity downturns would disappear.

Marcus

Goldman Sachs has announced plans to add automated investment (in other words, a robo-advisor) to it’s Marcus cash savings accounts in the second half of 2021.

- It’s reportedly the usual offer of stock and bond ETFs in ratios matched to risk level and time horizon, with rebalancing thrown in.

In the US, a Marcus Invest account can be opened with $1K and costs 0.35% plus the underlying ETF fees.

- So it’s probably not cheap enough for me.

Quick links

I have seven for you this week, all from the Economist:

- The newspaper claimed that the rules of the tech game are changing

- And that there are new rules of competition in the technology industry

- And that Apple’s duel with Facebook is a new form of big-tech rivalry.

- The Economist also noted that prices in the world’s biggest carbon market are soaring

- And asked what is the cheapest way to cut carbon?

- The newspaper also noted that the prices of sports cards and other collectables are soaring

- And worried that UK government loans will create a lot of zombie companies.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London.

He has been managing his own money for 40 years, with some success.

The Mauldin article is interesting.

What particularly caught my eye was there is little difference between the black & red lines – which I have interpreted to be further evidence for avoiding trying to time the market.

I think that might be confirmation bias. I agree it’s good news that on average the S&P is flat during inflation, rather than down. But there are different degrees of inflation, and stocks react differently to them.

It really depends on what’s going on outside of stocks during inflation. You might have a good shot by moving over to commodities or gold. Or if the inflation is country-specific rather than global, there could be country plays or FX opportunities.

Mike,

The phrase used by Gavekal is “excess returns”, specifically:

“All—and we mean all—of the excess returns from owning US equities in the last 142 years came in disinflationary periods, while no excess returns were achieved during the inflationary times.”

I have taken “excess returns” to mean over and above above inflation.

If this is correct, then the chart says that during periods of inflation stocks just about keep pace.

Is that your interpretation too?

Yes, I guess. But even if they meant in nominal terms, or were subtracting a risk-free rate instead, would it change your conclusions?

Not really – but given the extremes that inflation has reached in the years covered it would be somewhat comforting to know that Equities basically maintained their purchasing power!

I think we have a sample size problem – too few periods of high inflation to be sure.

The impression I’ve picked up from the current chat about rising inflation is that stocks are fine under moderate inflation (certainly up to 4%) and less good under high inflation. But someone (I think Dylan Grice) said that this negative view comes from one bad spell in the 1970s, and things might not be so bad.

Graphic of approx. decadal average US inflation (from 1913) in this post is useful:

https://www.theretirementmanifesto.com/inflation-the-silent-killer-of-retirement/

UK inflation history is generally worse – ie higher for longer.

IIRC, the 70’s was notorious for double whammy of oil crisis & high inflation!