Weekly Roundup, 14th April 2015

We begin today’s Weekly Roundup as usual in the FT, with the Chart That Tells A Story.

Contents

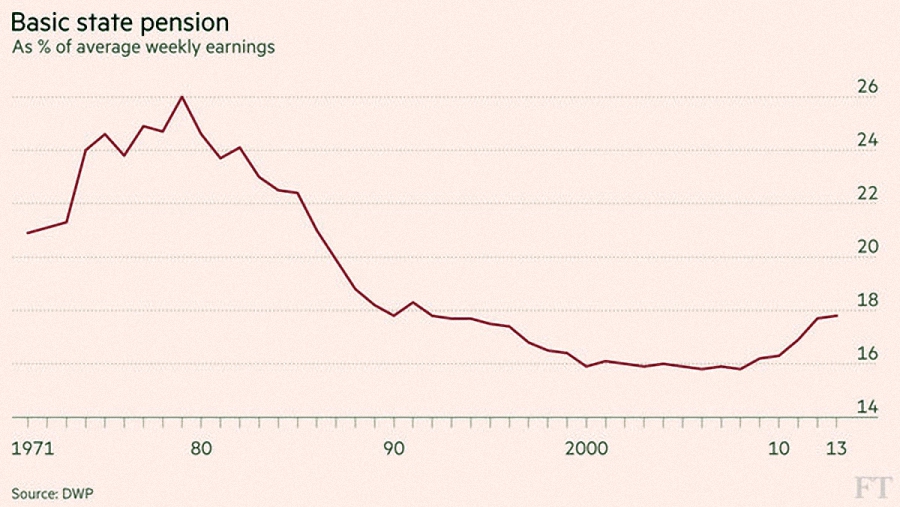

Pensions vs Earnings

Lucy Warwick-Ching took a look at the relationship between the state pension and average weekly earnings over the past forty years. Pensions peaked at 26% of the weekly wage back in 1979, and remained more than a third below that in 2013 (the last year for which data is available) despite a recent recovery from 16% in 2008.

Pensions started to decline when the Thatcher government linked them to retail prices rather than wages, in 1980. Earning generally rise faster than prices. Pensions began to recover when the coalition instituted the “triple lock”: pensions now rise by the largest of earnings, prices or 2.5% annually.

Things should improve further when the new state pension of £148 per week (£7.7K pa) is rolled out next year, but even this rate is below 1979 peak (it works out at 23% of average 2013 earnings). To qualify for the new pension, 35 years of NICs or credits will be needed.

Record VCT demand

Adam Palin wrote about the high demand for Venture Capital Trusts (VCTs) which have reported their highest annual sales since 2005-06, after which 40% up-front tax relief was removed. The reduction in the annual and life-time tax-free pensions allowances is believed to have been a factor.

VCTs are likely to be in even greater demand this year, as the annual allowance has been further reduced, and two years of heavy fundraising mean that the industry is not short of cash. Regulations mean than 70% of new money must be invested within 3 years, so there are limits on how much can be raised.

VCT rules were tightened in the recent Budget to comply with EU state aid regulations. Companies receiving VCT cash must now be less than 12 years old and the maximum investment across VCT and EIS is £15M, or £20M for “knowledge intensive” firms.

Homes sell every 23 years

James Pickford wrote about the dramatic decline in the turnover of houses. From selling every eight years back in the 1980s, the average home now changes hands once every 23 years.

The reasons are unclear, though the increasing difficulty of first-time buyers to get on the housing ladder, and of second-time buyers to find suitable affordable larger properties must be factors. The recent increases in stamp duty at the top end of the market will only make things worse.

There is also a trend away from using mortgages to finance house purchases, with the average contribution from cash and / or existing equity reaching a record 58% in 2014.

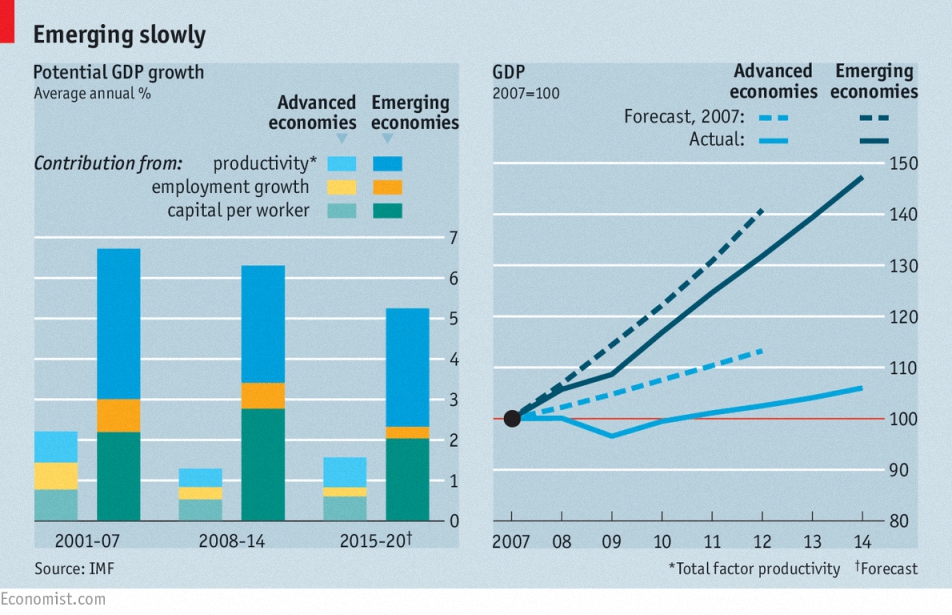

Slowing global economy

![]()

The Economist reported on slowing global growth, as described by the IMF in its latest “World Economic Outlook”. Potential growth in developed economies was already in decline before the 2008 crisis, because of slowing productivity growth and ageing workforces. The lack of investment since then has made things worse, reducing potential growth from 2.2% before the crisis to 1.5% in 2013-14.

The IMF thinks that developed countries will recover slightly but that emerging markets will suffer long-term. Demographics are already impacting countries like China, and productivity growth must slow as these countries reach developed world levels. So not much growth to look forward to anywhere.

US crowdfunding regulation

The US will bring in new rules in May which for the first time allow the general public access to risky, early-stage investments. Companies will be able to raise up to $50M in a “Mini IPO” with lighter regulation from the SEC. No stock-exchange listing will be needed, and reporting can be semi-annually rather than quarterly. No independent audit committee is needed.

Previously only “qualified” investors ($1M net worth or $200K annual income) were eligible, but now anyone can invest up to 10% of their income in such ventures. Crowdfunding websites like KickStarter and IndieGogo will be able offer shares rather than products, and are expected to boom even further. Whether the small investors will do so well out of the new rules remains to be seen.

Rich man, poor man

Every government wants to play Robin Hood, taking from the rich and giving to the poor. The economic logic is that rich people save more, so that redistribution should boost consumption and therefore GDP. It’s also a vote winner, since there are more poor people than rich ones. ((Support for redistribution actually varies by age, with the young & poor in favour and the old & rich against))

Underpinning this is the idea that the rich can smooth consumption if they are taxed more heavily – they have liquid reserves to draw upon. But new research from Princeton and New York Universities suggests that this may not be the case. The researchers looked at salaries, benefits and alimony alongside bank accounts, bonds and stocks to identify which people had liquid wealth, and which ones lived “hand to mouth”.

- Median US households held some liquid wealth in savings accounts, plus illiquid wealth in pension accounts and home equity, but had little in the way of stocks or bonds.

- Thirty per cent of the population lived hand to mouth, although two-thirds of these had significant illiquid wealth.

- This 20% do not fit the traditional definition of rich or poor. It’s tempting to call them the squeezed middle.

- Mortgages are the main driver of this phenomenon. Of those with small mortgages, only 20% live hand-to-mouth; for those with mortgages close to the property value the figure rises to 50%.

- Age is also a factor, with cash-poor households peaking at age 40.

US windfall studies show that those with liquid wealth spend only 13% of an unexpected cash sum, while those living hand-to-mouth spend 24%. Even more signficantly, the wealthy but hand-to-mouth spend 30%. A separate LBS study showed that in the UK, those with large mortgages reacted most to both tax cuts and tax raises.

The key point for politicians is that they could aim their stimulus much higher up the income scale than they think, and see an even greater boost to GDP. It also means that taxes on the wealthy need to be phased in slowly, so that assets can be liquidated in order to cope. Let’s see if any politicians take notice.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.