Weekly Roundup, 19th June 2019

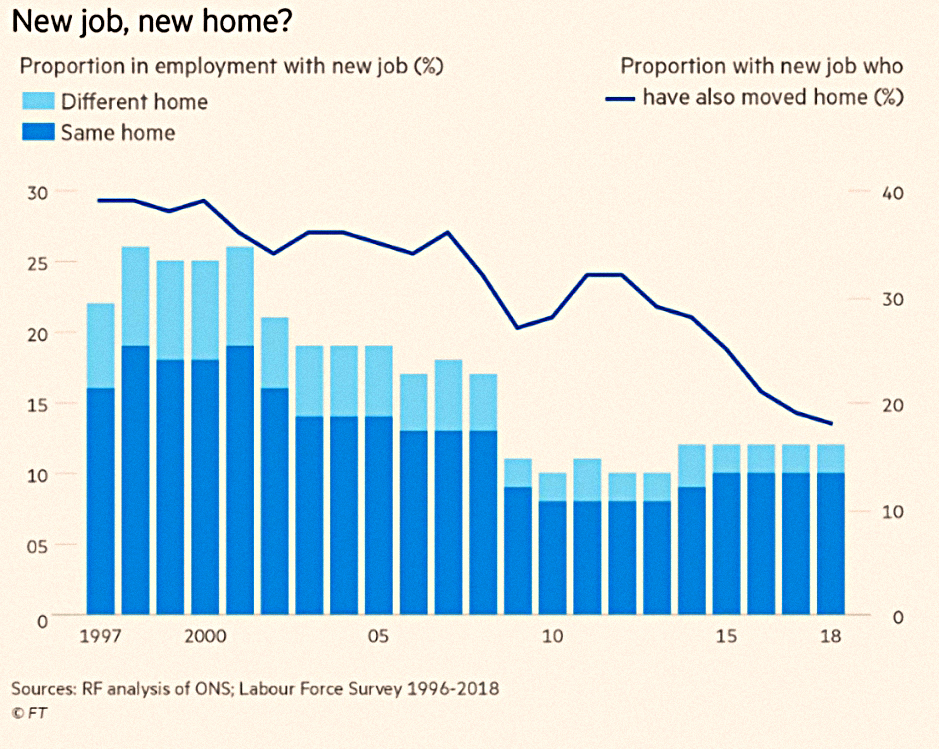

We begin today’s Weekly Roundup in the FT with the Chart That Tells A Story. This week it was about the impact of rents on worker mobility.

Contents

Rents and mobility

Lucy Warwick-Ching looked at the number of renters aged between 25 and 34 moving jobs and homes each year.

- The numbers are down 40% over the past 20 years, and so is the proportion of those who have moved jobs and also moved house.

Young people used to move from small towns to big cities in search of better-paid work, but it now appears that high rents are deterring them.

- As an example, moving from Devon to Bristol in 1997 would have increased income by 16%, but this gain is now just 1%.

Moving to Croydon from a nearby low-pay area actually leads to a loss.

As well as high rents, it’s also the case that renters today are older and more likely to have kids, which also deters relocation.

- If the Resolution Foundation is correct, the best solution is to build more houses in high-wage areas.

Tory tax plans

Lucy also had an article about the tax plans of the Tory leadership contenders.

- There were similar articles in the Economist and Money Week.

Boris looks a nailed-on winner at the moment, so in all likelihood, only his plans will matter.

- Which is good news for me, as he plans to extend the basic rate tax band from £50K to £80K.

There’s been a lot of bleating about this in the press, as it will benefit “rich” people.

- But £80K pa is not rich in London, and more importantly, people in the £50K to £100K bracket are the key adders of value in our economy.

Spending on public services and giving more money to the poor doesn’t make society better off, though this point seems lost on half of the population.

- We need to incentivise the people who make a difference.

TV licences

Unsurprisingly, the Economist backed the decision of the BBC to means-test free TV licences for the over-75s.

- I don’t like means testing and I don’t like the BBC, so equally unsurprisingly, I’m against the change.

I think the licence fee should be scrapped.

- We’d soon find out how good the BBC is if it had to earn its own money.

Bull market

Merryn Somerset Webb wrote about how digitisation is giving the bull market fresh legs.

- The average UK bull market lasts 56 months and returns 203%.

The current market is 120 months only (second only to the 152 months from 1975 to 1987) but has returned only 106%.

- If you start from the regaining of the pre-crash highs, rather than from March 2009, then the current bull is only 74 months old with a return of 83%.

We’re also lacking the traditional melt-up that normally comes at the end of a bull – there’s no euphoria yet (though we had a little at the end of 2017).

Further support is provided by low inflation (which generally leads to high equity valuations) and a likely pending productivity boom from digitisation, automation, data analysis and process optimisation.

- Merryn admits that this has been a long time coming (outside of media and finance), but she thinks that a 20-year lag for the impacts of new technology is typical – look at railways, electricity, mass transport and computers as examples.

She also mentions shale oil:

It was inexpensive cloud computing that prompted the data analysis that made finding it and getting it out worthwhile.

On the other hand, a cold war with China could bring protectionism and inflation.

- And demographics could tighten the world’s labour market and lead to wage inflation.

She recommends avoiding the expensive US and investing in the cheaper UK instead.

External influences

Jason Butler told us to ignore external influences when it comes to finances.

- He recommends developing a set of money rules to make sure that you stick to your principles.

His own rules are:

- Have 18 months of living expenses as a cash buffer

- Spend only 50% of income on lifestyle

- 15% is invested, 10% is saved, 10% goes to charity, 5% is spent on personal improvement and 10% used for “business holdings”

- Pay cash except for appreciating assets

- This is the “a mortgage is the only good debt” rule

- Don’t borrow more than 60% against a house

- Only do meaningful and fulfilling work

- Keep your finances simple

- Only use government-endorsed tax planning

- Spend to but time, experiences, maintain health and help family/friends

- Maintain a financial support team (accountant, tax planner, lawyer and financial planner)

- Have enough assets to maintain your lifestyle without working

Not a bad set overall, though I have a different split for income allocation and more of a DIY bent.

Jason also recommended a tool called Five Dials.

- I didn’t find it helpful, but you might.

More Woodford

There was a lot more on Woodford this week:

- Here are a couple of links from the FT – 1 and 2

- And one from the Economist

I’m not sure that there was anything to add to what we learned last week:

- Investment trusts make better vehicles for illiquid investments than do unit trusts.

- Active funds may become less popular with investors.

- Some people may be scared off equity investments forever, which would be a terrible outcome.

- Or perhaps they will become DIY investors instead – which would be a good thing.

- Star fund managers rarely outperform forever.

- Diversification – as always – is crucial in investment.

- Fund managers who change their styles mid-career are effectively throwing away their track record.

- A lot of investors don’t understand the risks they are taking with their money.

- Small-cap funds and those investing in unlisted stocks need to stay small and nimble.

- Fund managers are paid a lot of money but don’t share in the downside risk with their investors.

- Funds (and managers) sometimes stray from doing what it says on the tin.

- We may be in for some form of governance obligations for providers of best buy fund lists.

Time and portfolio choice

In the Economist, Buttonwood looked at Robert Merton (Nobel prize winner for his work on the Black-Scholes option pricing model) and the effect of time on portfolio choice.

- Merton was also one of the brains behind LTCM, a hedge-fund which blew up in 1998.

His paper on the importance of time on portfolio selection is now 50 years old.

- Contrary to the popular opinion that young people should take on more risk, Merton and Paul Samuelson showed that if risk appetite was constant (and stock prices are unpredictable) then the portfolio should also stay the same.

The result changes when you include human capital in the equation.

- If 90% of a young person’s capital is human, a 40% stock market crash can produce no more than a 4% impact.

For an almost-retired person with only 10% human capital, the maximum impact is 36%.

- So an older person might want a safer portfolio after all.

Human capital is low-risk. If you have lots of it, you can take more financial risk.

Cheap advice

One of the unintended consequences of the RDR (Retail Distribution Review), which banned commissions on investment products, was the loss of access to financial advice for those with small portfolios.

- Without hidden commissions, advisers could not offer advice at a price than most people would pay.

So I was intrigued to read in FT Adviser that Evalue would be offering advice for a flat fee of £200.

But it turns out that:

The service would be launched by working with benefits consultants so it could be offered in the workplace for people wanting advice on their pensions.

Which is a pretty limited version of advice.

Quick links

I have ten for you this week:

- The Economist wrote about video gaming in the cloud

- And about trust-busting talk in the US

- And about how digital technology will strengthen incumbent US retail banks

- The FT wrote about how London became a global tech hub

- And that the Bank of England thinks challenger banks are cutting corners

- Alpha Architect looked at the cross section of Emerging Markets stock returns

- And at whether leverage can explain the investment premium

- Disciplined Systematic Global Macro Views looked at whether momentum models are better than moving average models

- Musings on Markets looked at the Beyond Meat valuation

- And Early Retirement Now wrote about the small-cap and value factors.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.