Weekly Roundup, 23rd February 2016

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story.

Contents

Gold

Henry Sanderson took a look at gold, which is popular once again.

- After three years of outflows, gold ETFs are reporting record daily inflows. Prices are up 15%, too.

The article looked at the different ways for investors to gain exposure, but disappointingly it seemed aimed more at US investors predicting a doomsday scenario.

I’m interested in options for the UK private investor who wants 5% to 10% gold exposure as partial insurance against weakness in stocks and other currencies, and the article didn’t provide them.

- I’ve used PHAU in the past – it’s the Physical Gold ETF from ETFS.

- Henry wasn’t keen on investing via gold mining shares. These can be volatile, and may not track the gold price closely.

- Gold coins like British Sovereigns or Britannias area another option, as they are tax-free in the UK.

Smart Beta

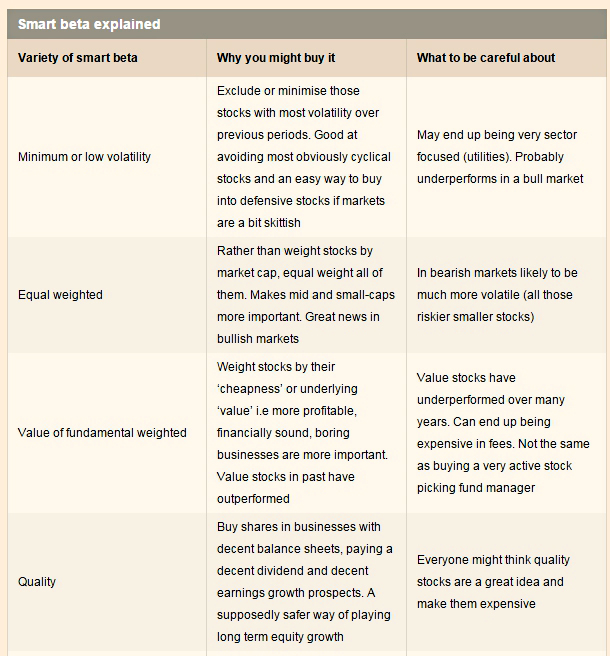

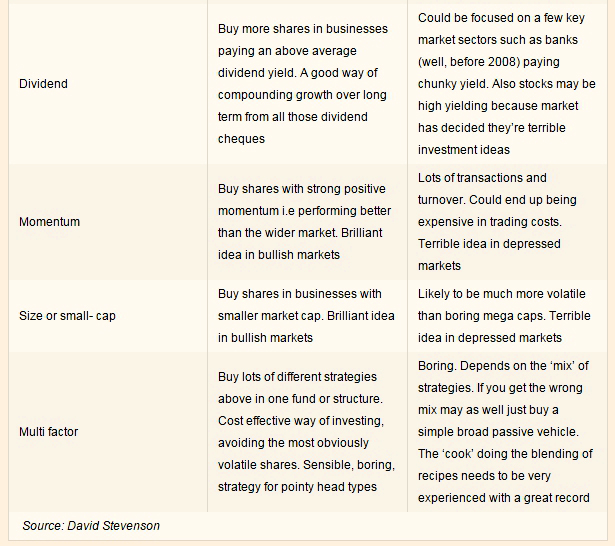

In his Adventurous Investor column, David Stevenson gave a good overview of smart beta.

- Smart Beta is the “third way” between low-cost trackers and conviction stock active funds.

- It’s a way of simplifying, automating and lowering the cost of the “factor investing” approach that I’m a big fan of.

It’s also catching on, mostly with institutional investors. Smart beta now accounts for 20% of the ETF market.

- this is partly because fees have fallen a lot in recent years, particularly in the US

Certain types of stocks tend to outperform:

- small stocks

- value (cheap) stocks

- momentum stocks (that have recently risen in price)

- dividend stocks

- low-volatility stocks

There are also superior ways to construct indices (eg. equal weight) than the market cap approach that has been used for the past 40 years.

As David points out, the problem with smart beta is that the marketing guys have poked their noses in, leading to a lot of mumbo jumbo that will confuse most investors.

- David has a chart summarising the main offerings, their good points and what to look out for.

One thing to watch is churn.

- Tracking an index can require a lot of changes to stock allocation through the year, and following smart beta rule can be even more active (and costly).

Cheap oil

Tim Harford looked at the consequences of cheap oil.

- In theory, low oil prices are bad for the planet (a lot of oil will be burned) but good for the economy (transport costs are low).

- Even in the UK, which produces a lot of its own oil, cheap oil should boost GDP by 1% or more.

This matches past experience:

- oil was cheap during the golden age of the 1950s and 1960s, and the oil shocks in the 1970s triggered recessions.

- The pattern was repeated in the last 25 years, with cheap oil during the boom 1990s and higher prices before the 2008 financial crisis.

Tim ran through some simple maths:

- the world consumes around 100M barrels of oil per day

- at $100 a barrel, that’s $10bn per day ($3.5trn per year)

- low prices like today would cut that bill by perhaps $2trn per year

- with global GDP at $80trn, that’s a 2.5% boost

But there’s a snag.

- in previous eras, this transfer from producers to consumers was a boost

- producers were saving their profits while consumers would spend their windfall

- today, consumers will use the spare cash to pay down debts, and producers will be forced to reduce investment and public spending

- so the low oil price can be recessionary and deflationary

A secondary effect will be the lack of innovation in energy-saving technologies.

- Tim’s solution is a carbon tax to discourage oil consumption

The next recession

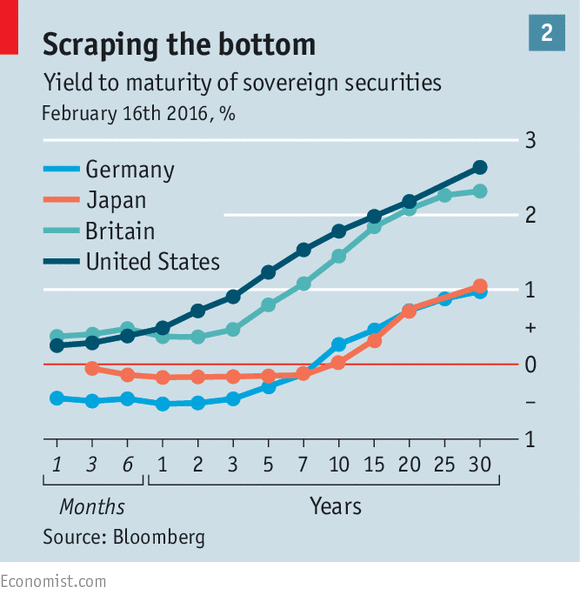

John Redwood looked at whether a loss of confidence in the banks could trigger a recession, and burst the QE bubble.

- He thinks that investors are worried that central banks have run out of options (more on that later).

There are legitimate concerns about Greek, Italian and Portuguese banks, and somewhat less concrete problems with Deutsche bank (as we saw last week).

- The real issue is that with low and negative interest rates, it’s hard for banks to make money (and use the profits to strengthen their balance sheets).

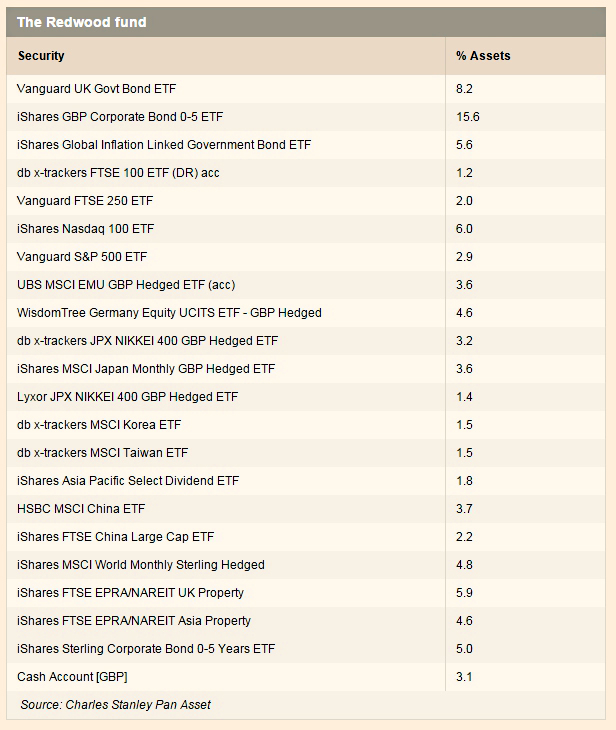

John thinks that we are in a world of slow growth, but not “no growth”, and he expects to see a bonus from cheap oil.

- His ETF portfolio is tilted towards developed markets, technology and emerging Asia.

Political risk in the US

John Authers looked at political risk in the US.

Despite the media coverage for Donald Trump, prediction markets have given the Democrats more than a 50% chance of winning the election ever since the summer of 2015.

- they are currently at 62%, 10 points ahead of their score at the same stage four years ago

But stock markets can affect election results.

- Falling stocks make people poorer and less likely to vote for incumbents.

- Obama was the beneficiary of this effect in 2008.

- The same goes for a worsening economy.

So why are people predicting a Democrat victory?

- None of the candidates is a friend to Wall Street, so further stock market wobbles are likely in the run-up to the election.

John draws a parallel with the 1968 election: Vietnam, the assassinations of Robert Kennedy and Martin Luther King Jr, riots in the streets.

- Nixon – who won – was the Hilary Clinton candidate: well-known, not liked, but a safe pair of hands.

John sees all the risks for stock prices to the downside.

- But what if the Democrats decide to make sure thinks look good in November, to make sure that voters don’t reject the incumbent party?

Maybe we could see some helicopter money in the summer that would push the markets higher.

Not the Big Short

Neil Collins wrote about the film The Big Short, which seems to have impressed the Oscar voters and most of my friends (but not me).

- He was prompted by comments by Sir John Vickers that banks still don’t have enough permanent capital to survive the next crisis, and that more bailouts will be needed.

Neil points out that the real problem in 2007 was reckless lending.

- The complex derivatives that were spectacularly misunderstood by the ratings agencies may have grabbed the headlines

- and it’s easier to blame Wall Street than your local mortgage salesman

- but the 2008 crisis was really down to lending money to people who could not pay it back.

Slippery P2P

Aime Williams reported that the P2P lending platform RateSetter has been raiding its protection fund to make sure that businesses got hold of their loan money sooner.

Ratesetter did, at least, make an announcement that 10% of the fund would be used “provide immediate liquidity”.

- Four days later they backed down – they won’t be using the fund after all.

Nothing to worry about then.

New weapons

In a couple of articles (1 and 2), the Economist looked at what new tactics central bankers might have to resort to in order to stimulate the economy.

- The newspaper’s big theme is that fiscal and monetary policies need to work in tandem.

- Politics has been getting in the way until now.

- They also think that inflation targets should be radically changed (see next section below).

Option number one is helicopter money – giving money directly to consumers, bypassing banks and financial markets.

- The idea is that most people would spend it, and this could be encouraged by having some kind of time decay (in effect a negative interest rate) attached.

- A slightly less radical version of this would be to cancel some of the sovereign bonds purchased under QE.

- Both these measures leave the central bank technically bankrupt (owning fewer assets than it has liabilities) but this should not matter in practice

Even more radical would be wage and price controls.

- This involves using tax incentives to produce large (5% to 10%) rises in wages, and the triggering of a 1970s-style wage-price spiral

- Of course, back in that high-inflation world, this was a bad thing at the time, and incomes policies were designed to cap inflation

The Economist would also like to see more public spending, backed by borrowing at record low levels.

- If spent on useful infrastructure, rather than roads and railways to nowhere, this could have an effect, though it might take years to appear.

- But there is not much appetite for more public debt since there has been so little to show for what has been added so far.

- The rich world’s main central banks have added an average 25% of GDP to their debts through QE: US from 64% of GDP in 2008 to 104% in 2015, Eurozone from 66% to 93%, Japan from 176% to 237%.

Tax cuts for the low-paid (who are more likely to spend a windfall) could also be used.

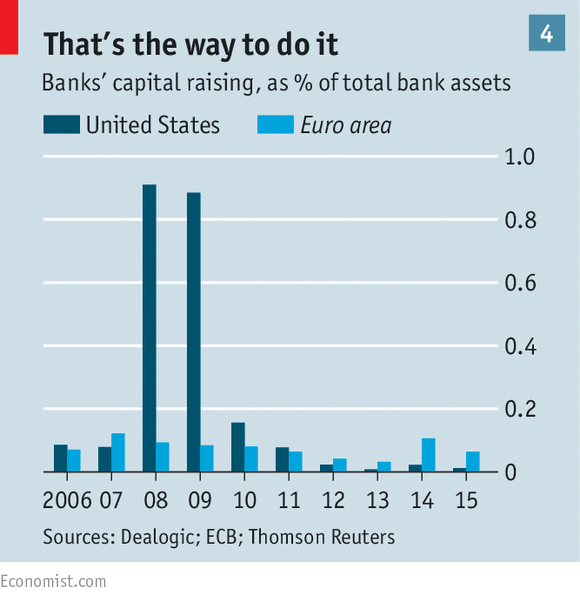

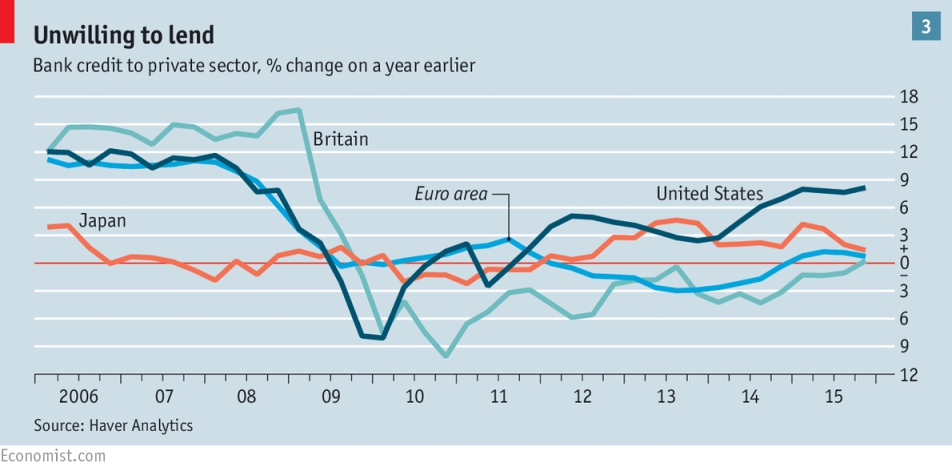

The rules on banks need to be changed so that their balance sheets can be fixed properly, allowing them to lend once more.

- This happened in America in 2009, which is why US banks have outperformed since then.

And in the US, lots of red tape also needs to go, and the tax code needs simplifying.

Knob turning and magic wands

Finally, the Economist also looked at the role of central bankers. here are two options:

- knob-turning technicians, fine-tuning the economy

- magicians, creating the suspension of disbelief in their audience

Mostly they act like the former, but in extreme situations like today – with the world increasingly sceptical about what can be done – they need to become the latter.

In the 1980s, the economic problem was the opposite of today’s stubbornly high inflation that needed to be defeated.

With high expectations of inflation held by the public, very high interest rates – high enough to kill growth – would be needed to force down prices and reset expectations.

Then economist Thomas Sargent pointed out in a 1982 paper that episodes of hyperinflation typically ended quickly with a “regime change” government policy.

So the key was to promise to halt inflation, and immediately behave as if this was possible.

A 1990 paper from Peter Temin and Barrie Wigmore applied the same approach to an economy stuck in a slump, using the 1930s as an example.

The longer that knob-turning fails, the less credible will a subsequent attempt at regime change seem.

- Witness the lack of reaction to negative interest rates.

The snag with the magic wand approach is that it generally requires a new magician – a new popular government – to do the waving.

Which offers some hope for the US, but not much for the rest of the world.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.