Weekly Roundup, 26th June 2018

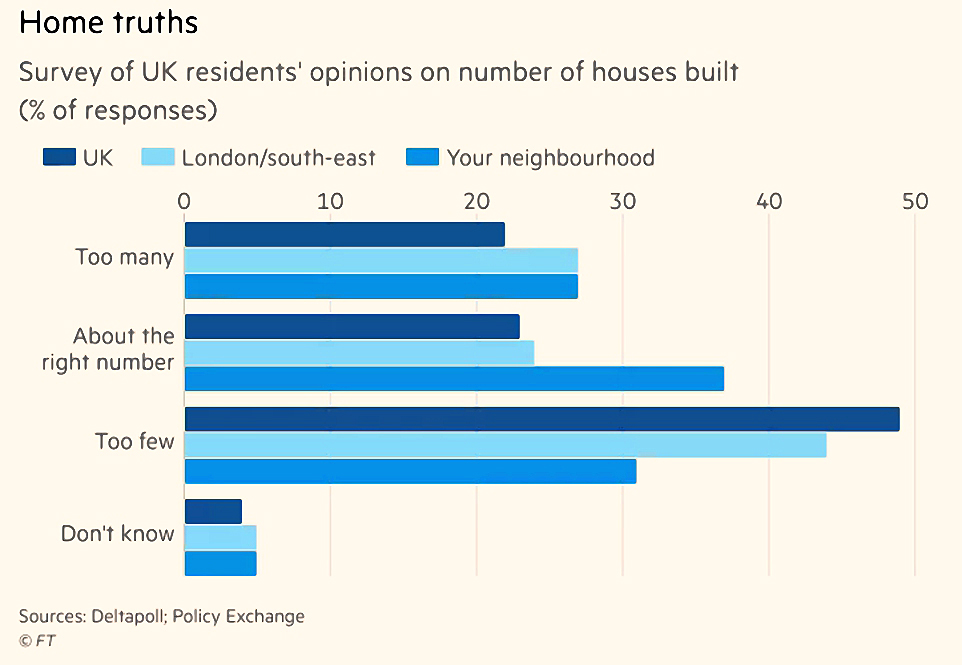

We start today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about NIMBYs.

Contents

NIMBYs

Aime Williams reported on a survey of 5000 people on behalf of think tank Policy Exchange.

- It showed that plenty of people are in favour of more homes being built.

- But not so many are keen on them being built in their own neighbourhood

Yes, it’s another article from the FT’s Department of the Bleeding Obvious.

Policy Exchange believe that the key reason that so many people are NIMBYs (“Not In My BackYard”) is that they think that new housing will be ugly.

- Most people prefer Georgian and Victorian styles, and these rarely get built.

The YIMBY (“Yes In My BackYard”) movement feels the same, and is campaigning for more Victorian-style mansion blocks (which are surprisingly high density) to be built.

- Style is definitely part of the problem – the blocks built recently near me are mostly horrible.

But I think there are three other reasons:

- Increased density

- Prices per square foot are now so high that flats have to be tiny in comparison to the local average in order to be “affordable”.

- Most properties near me are family houses, but all the new builds are two-bed apartments or smaller.

- Changing character

- Smaller flats means smaller household sizes.

- This can change the type of people who live in an area, and therefore the type of services that are provided to them (bars and fast food joints replacing traditional restaurants, for example).

- Overwhelmed services

- Some services take time to respond to the increase in demand (the NHS, for example).

- Others can’t respond – the Northern Line near me is now largely unusable in the morning rush hour, as people from further down the line fill the trains before they arrive.

- And still others (petrol stations, DIY stores) are replaced by the new flats, making life less convenient for the existing locals).

So it’s not too surprising that people don’t want the area they bought into to change for what they see as the worse.

It’s a bit like the immigration debate.

- I don’t think that so many people don’t want any immigration at all.

But they want to see immigrants who can make a contribution in terms of skills and resources they bring with them.

- And they don’t want so many people to arrive in the same area that the character of the location is changed.

I think that the often-touted (but never built) new “garden cities” – with good transport links to London – are a better approach to the housing crisis than ever-denser developments in the capital.

- But I wouldn’t say no to some more Victorian mansion blocks.

Catch up

Tim Harford looked at whether poor countries catch up with rich ones.

- This is known as convergence.

It should be relatively easier for poor countries to make progress, since investment should show higher returns.

- This is the argument that the biggest difference is between 1 and zero – the law of diminishing returns.

This in turn should draw capital to such countries to help them develop.

- In practice, things are more complicated.

The world has converged since 1970, but most of the gains are concentrated in six countries – China, South Korea, India, Poland, Indonesia and Thailand.

Economists now speak of “conditional convergence”.

- Dodgy regimes prevent countries like Venezuela and North Korea from catching up.

Apparently there are a few (low-tech) sectors where convergence happens anyway:

- They include pasta/noodles, knitwear and plastic bags.

- This appears to be down to global supply chains.

Since it’s World Cup time, Tim notes that convergence is also observed in international football.

- This is down to fierce (and transparent) competition, and a global labour market that encourages skills transfer

I think Tim’s right in the sense that the gap between the bigger and smaller teams is closing.

- But when the competition gets down to the sharp end next week, I still expect the usual suspects to be involved.

Investment trusts

Merryn’s column was about the success of the investment trust model.

- Over the last 18 years, they have outperformed OEICs by 1.4% pa, according to research by Cass Business School.

This is partly down to sector bias (factor investing, for example more exposure to small companies) and partly because of (moderate) gearing.

- Share buy-backs and survivorship bias also help.

But after all four factors are removed, there is still 0.84% pa of outperformance.

- Merryn thinks that good governance also contributes (she is a a non-exec director of two trusts), as well as (historically) lower fees.

Fees are no longer lower than those of OEICs, though you also need to consider platform fees, which are often still lower for ITs.

- The other factor to consider is the discount / premium to underlying net asset value – Cass used NAVs rather than share prices for their research.

It’s risky to buy an IT on a premium that might subsequently disappear, or even on a smaller than usual discount.

- The average discount to NAV since 1989 has been 9.4%, but today it’s only 4.2%.

Despite these concerns, I’m a big fan of ITs for the actively-managed part of my portfolio (outside UK stocks, where I can make the case for direct investment).

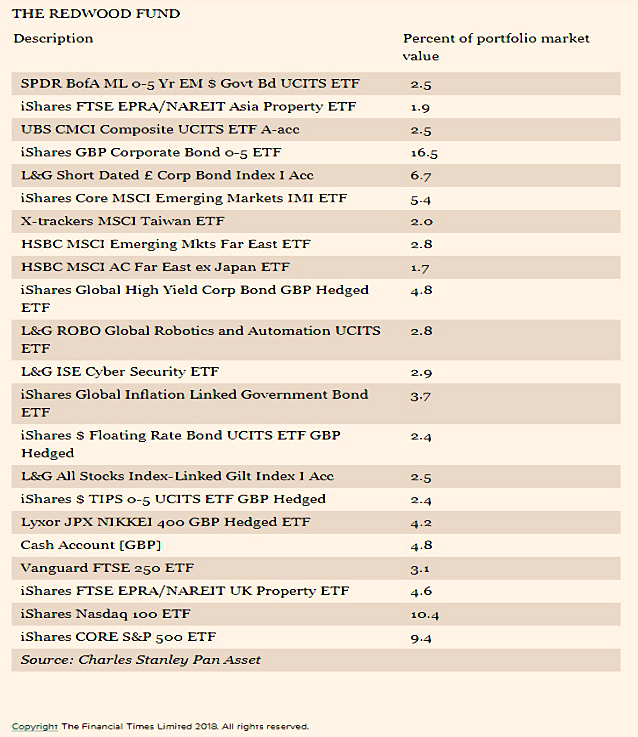

- Here’s a list of our favourites.

P2P property lending

Davis Stevenson wrote about P2P property lending.

- He ran an event on the topic last week, which I was fortunate enough to attend.

Lendinvest used to be the biggest player in this market, but no longer takes on new investors via its platform.

- It does have a retail bond programme, though.

Alternatives include Lendy, Relendex, Octopus, Alpha Real, Landbay and Proplend.

- There’s also Urban Explorer (UEX on AIM) and Starwood European Real Estate Finance (SWEF).

The most common product is bridge funding – short-term loans to developers at higher rates than traditional P2P lending (4% to 8%, rather than 4% to 5%).

David is not convinced.

- Interest rates could rise and the property market could have a slow-down.

- At the same time, most lending is conservative, with many loan-to-value (LTV) ratios below 60%.

I think that there are two additional problems:

- Most UK private investors have more than enough exposure to property through their primary residence, since property prices are so high in the UK.

- Apart from ITs (REITs), it’s difficult to tax-shelter your property exposure.

- IF-ISAs exist for some of these lenders, but at £20K per platform you need a substantial portfolio to obtain suitable diversification.

- And each £20K in your IF-ISA is £20K less in a much more flexible stocks and shares ISA.

If you do fancy investing, here’s David’s checklist of questions:

- Who does most of the borrowing — buy-to-let landlords, small builders or developers? Personally, I’d favour small builders over buy-to-let landlords, because they tend to operate in niche, higher-margin markets where demand is strong and are less vulnerable to any downturn.

- Where is the lending happening regionally? Greater London and the Southeast looks less attractive to me than some of the regions.

- Examine the capital stack in great detail. How much lending is going on above you? What is your lender’s median LTV ratio?

- Check out the due diligence process. Does a named person meet every lender and visit every site? I prefer good old fashioned human beings to make the lending decisions rather than AI and Big Data.

Redwood fund

John Redwood had his regular update on the ETF portfolio he runs for the FT.

- The fund is up 2% in 2018.

John sold his European shares in 2017, and expects things to get worse there before they get better.

Tail wags dog

John Authers feels that the rise of passive funds means that the tail is wagging the dog as far as indices are concerned.

- There were three big developments in indexing this week, and all moved the market.

First, GE was kicked out of the Dow Jones index after more than a century.

- It’s the last of the original members to leave.

- Walgreen Boots Alliance took its place, and rose 3% on Wednesday.

MSCI promoted Argentina from it’s EM index, replacing it with Saudi Arabia.

- The Argentinian market rallied 6%.

This week also saw the annual rebalancing of the Russell large- and small-cap indices.

- This is now the heaviest trading day of the year.

- The Russell rules are transparent, and new additions to the Russell 2000 usually outperform in the days leading up to the switch.

The problem is that active funds underperform indices on average (ie. in aggregate), so index funds are likely to attract ever more cash.

- Macro drivers or markets (such as central bank policy on things like QE) mean that the importance of stock-picking in comparison to asset allocation is even less important than usual.

- And low return environments (which we potentially face for the next decade at least) mean that low fees are more important.

So there’s no reason to think that the dog will regain control of his tail.

Lucky few

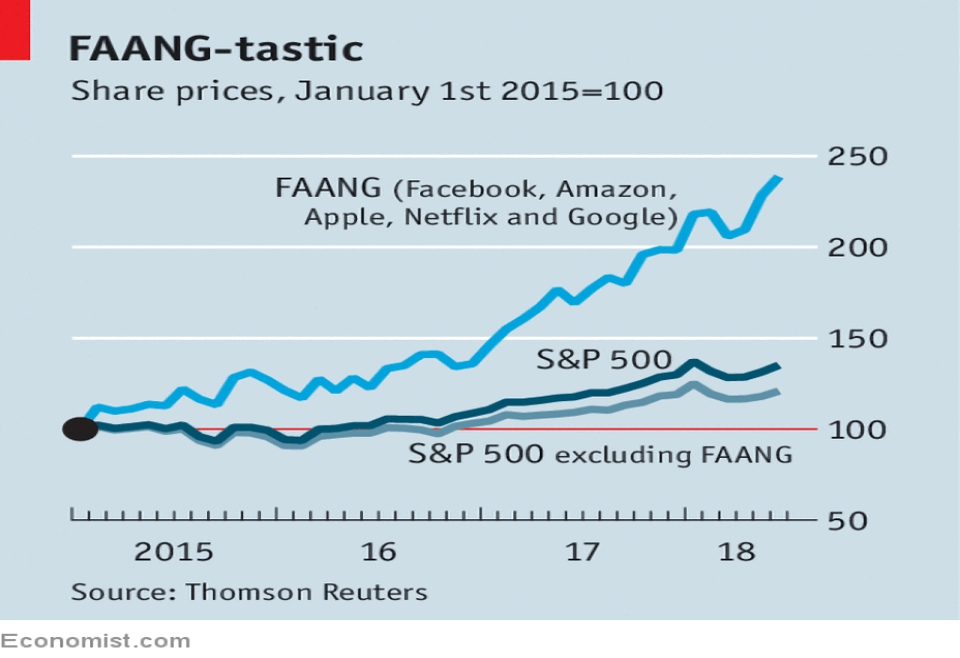

In the Economist, Buttonwood looked at a new paper from Hendrik Bessembinder.

Five stocks (Apple, Exxon, Microsoft, GE and IBM) created 10% of the wealth from 1926 to 2016.

- The top fifty stocks produced 40% of the total wealth.

- 90% of the universe of 25,000 stocks were worse investments than Treasury bills.

This means that the current FAANG domination is not so unusual.

- Of course, today’s winners may not be tomorrow’s.

The Economist recommends wide diversification across assets and geographies,

This paper has been discussed in several places this week, usually with gloomy conclusions.

- I think there is room for a more positive interpretation.

A key finding is that 4% of stocks deliver all the returns, with the remaining 96% flat.

Some think this means that you should hunt down this 4% (not easy) and ignore everything else.

- But you could equally ignore the 4%, and concentrate on owning the top half of the remaining 96%.

Avoiding the bottom 48% ought to deliver a handsome return.

- And it should be less difficult than finding the 4% of needles in the haystack.

Scottish Mortgage

The same research was quoted at the Scottish Mortgage Investor Meeting that I attended this week.

- Roger Lawson was also there, and he wrote it up for ShareSoc. (( Note that Roger misquotes Bessembinder’s key finding – I think – as being that 0.4% of stocks create half the returns – though that probably isn’t too far from the truth either ))

For those unfamiliar, SMT is a global growth IT which in recent years has focused on US and Chinese tech stocks, plus the odd luxury brand.

- The AGMs are still up in Edinburgh, so they also put these meetings on in London.

I’d never been before, and I was taken aback by how self-satisfied the fund managers seemed to be.

- Perhaps they are entitled, since their recent track record is excellent.

- There was also a lot of name-dropping (primarily of tech and luxury firm CEOs) which I didn’t enjoy.

James Anderson (the fund manager, not the cricketer) suggests that you need to look for the really successful growth companies.

- He looks for stocks with potential 40% pa growth, which should make his job fairly simple, given that so few stocks could achieve this.

He thinks that tech will disrupt not just media but also advertising and consumer defensive brands, along with healthcare.

- He also predicts deflation rather than inflation, and that China will dominate.

I’m a lot happier with his macro outlook than his approach to stock selection.

Quick links

- Marketwatch reported on a day trader whose demo platform turned out to be real, leaving with a $5 bn position.

- He also had a $12M profit, which his broker doesn’t want to pay him.

- Jim Rogers is linked with a new ETF which is driven by AI.

- Vanguard has a new version of the CAPE – the “fair-value” CAPE.

- There’s a CO2 shortage in Europe, potentially affecting those of you who drink fizzy beer.

- Investing for a living updated their quant strategies historical performance through 2017.

- The Adventurous Investor thinks that a crypto meltdown is looming.

- Himco looked at how to make price momentum more effective.

- FT advisor fears than pension tax relief will be cut in order to fund the extra £20 bn a year promised to the NHS.

- And Quant Investing explained how to lower your losses and increase your returns.

- Spoiler alert – you sell things trading a below the 200-day MA (he got the idea from Meb Faber).

That’s it for this week.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.