Weekly Roundup, 28th May 2019

We begin today’s Weekly Roundup in the FT with Tim Harford, who was trying to discern luck from judgement.

Contents

Luck vs judgement

According to Tim, randomness often explains the difference between triumph and failure.

- He used fund managers Neil Woodford and Anthony Bolton as examples.

But an alternative possibility is that the world changed. Good ideas don’t work forever because the competition catches on.

On balance, Tim favours luck as an explanation:

Sometimes things turn out very differently for no reason that we can discern. We might as well call that reason “luck” as anything else.

The psychologist Daniel Kahneman has recently been studying what he calls “noise”: the variability of judgments for no obvious reason. We rarely appreciate just how much inconsistency there is in the judgments we and others make.

Tim explains the magazine cover “curse” as a simple regression to the mean:

Few people make the cover after a run of mediocre luck. They appear after things have been going well, and if the good luck fails to hold then it seems like the jinx. More likely it is a return to business as usual.

Genius followed by mediocrity is a story arc we all notice. Mediocrity followed by genius just looks like genius.

Tim also points out that outsized success often comes from taking risks or being contrarian.

- But such an approach can also lead to outsize failure, too.

Redwood fund

John Redwood said that he was biding his time during the US-China trade war.

- During the rally at the start of the year, he reduced his stock allocation from 6% to 50% and increased cash to 15%.

He also cut his position in China and pulled out of Germany altogether.

As well as the China dispute, the US now wants to talk to the EU about car and food exports.

- A resolution here will be delayed by the recent European elections.

So John is doing nothing with his extra cash:

I still do not expect a recession or banking crash to warrant liquidating the rest of the share portfolio, but am awaiting a greater sense of optimism and direction from markets. That in turn will require new measures by central banks or governments to stimulate slowing economies.

Private client wealth management

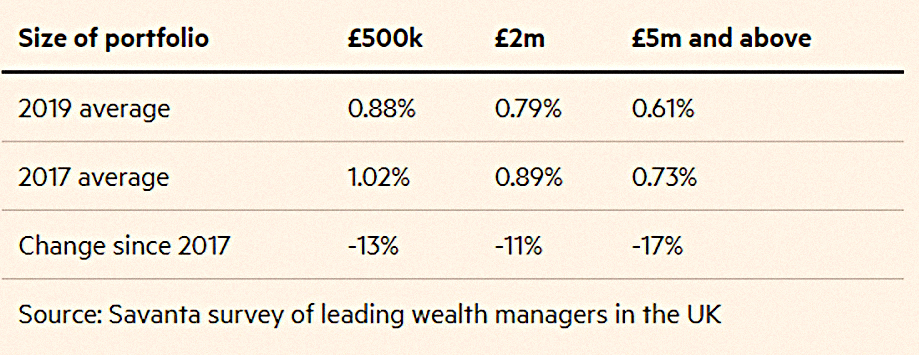

The FT published its annual survey of private client wealth management providers.

- It was carried out by market research firm Savanta, and director David Barks wrote that regulation has forced down fees.

David is talking about Mifid II, which increased transparency and will, therefore, have created downward pressure.

- The average fee for a £1M discretionary portfolio is now 0.86%, down from 0.99% in 2017.

At the same time, transparency has led to the unbundling of fees, with separate platforms and /or custody charges now common.

There has also been a move towards model portfolios, which are cheaper to run – especially for smaller clients.

- Minimum values for fully discretionary portfolios now average £800K, whereas the minimum for a model portfolio is often as low as £50K.

There are also trends towards family office services, and away from niches like offshore and charity services.

A less positive effect of Mifid II has been more paperwork.

- Perhaps because of this, the average manager now has just 118 clients, compared with 147 in 2017.

Bailouts

The Economist looked at failing companies and contrasted the reactions to the collapse of British Steel and Jamie Oliver’s restaurant chain.

The Labour Party argued that British Steel should be taken into public ownership. Even the right-wing Daily Mail appeared sympathetic to the idea of a bail-out.

Of course, no one suggested that Jamie’s should be bailed out.

- But of course, there is no real difference.

It is not clear why Britain needs to produce its own steel, since there is a perfectly good global market in the commodity.

IPPR, a think-tank, suggests that in addition to the jobs lost directly, a further 7,000 workers in the supply chain are in jeopardy. Yet it is hard to see why this should not apply to Mr Oliver’s restaurants, too. Laid-off waiters will claim welfare payments. Food suppliers will lose a big client.

If these were sensible grounds for a bail-out, any failing company would be entitled to one.

The newspaper suggests that instead there should be state-funded retraining for steelworkers.

- But what will they retrain in, and what new jobs will move to the affected areas?

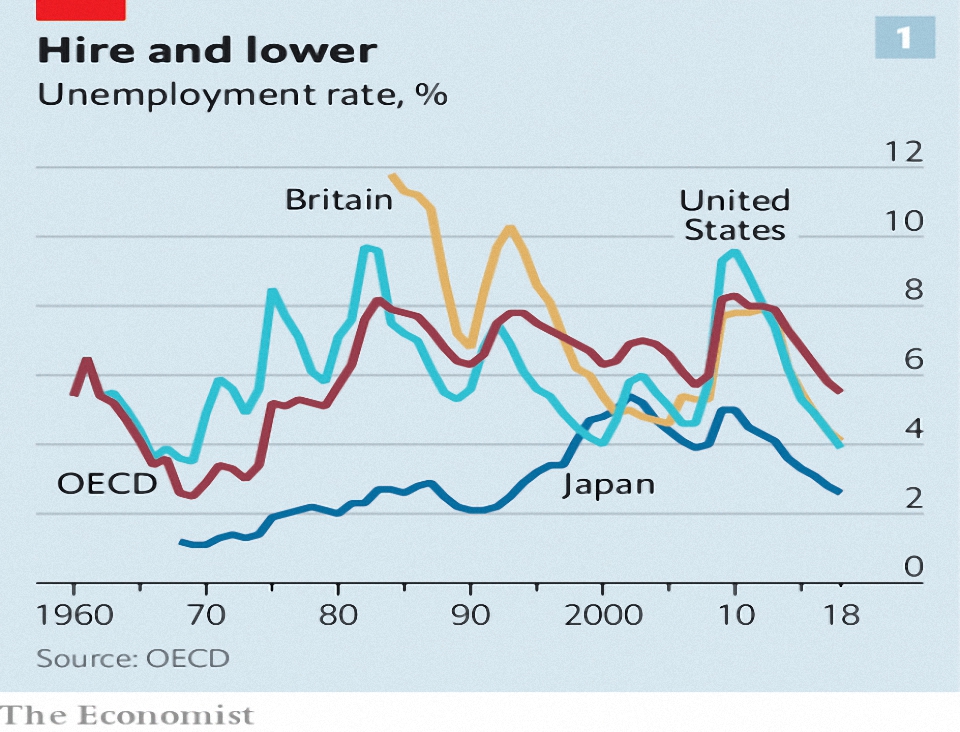

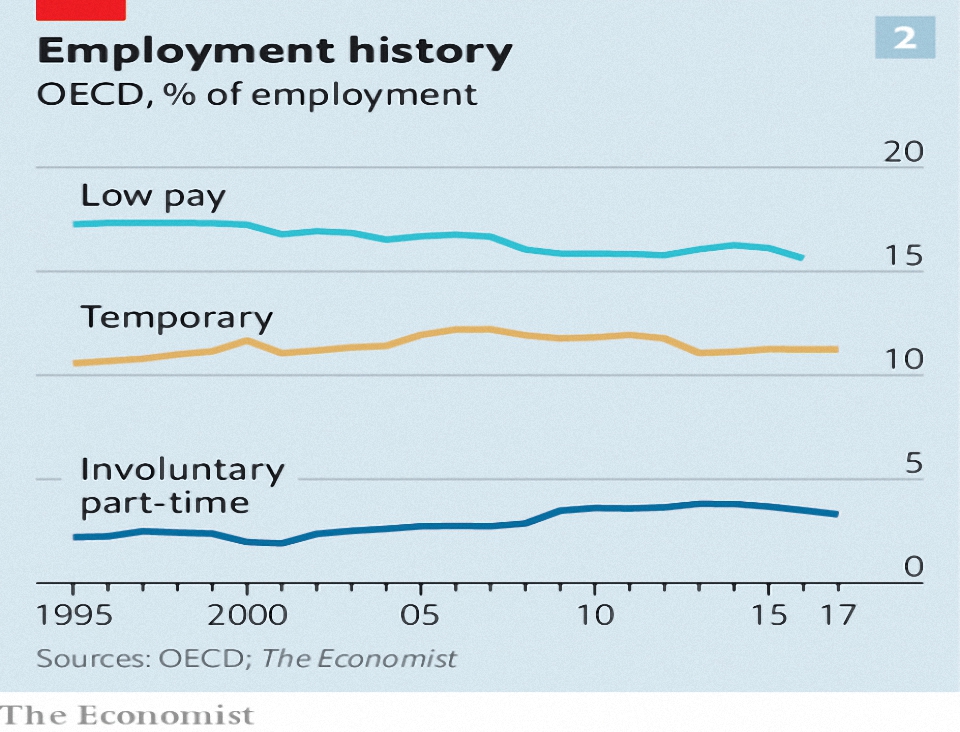

Jobs Boom

Stocking with jobs, the Economist had two articles (1 and 2) on the “unprecedented employment bonanza” in the rich world.

- The many current critics of capitalism appear to have missed this.

Not only is work plentiful, but it is also, on average, getting better. Capitalism is improving workers’ lot faster than it has in years, as tight labour markets enhance their bargaining power.

The zeitgeist has lost touch with the data.

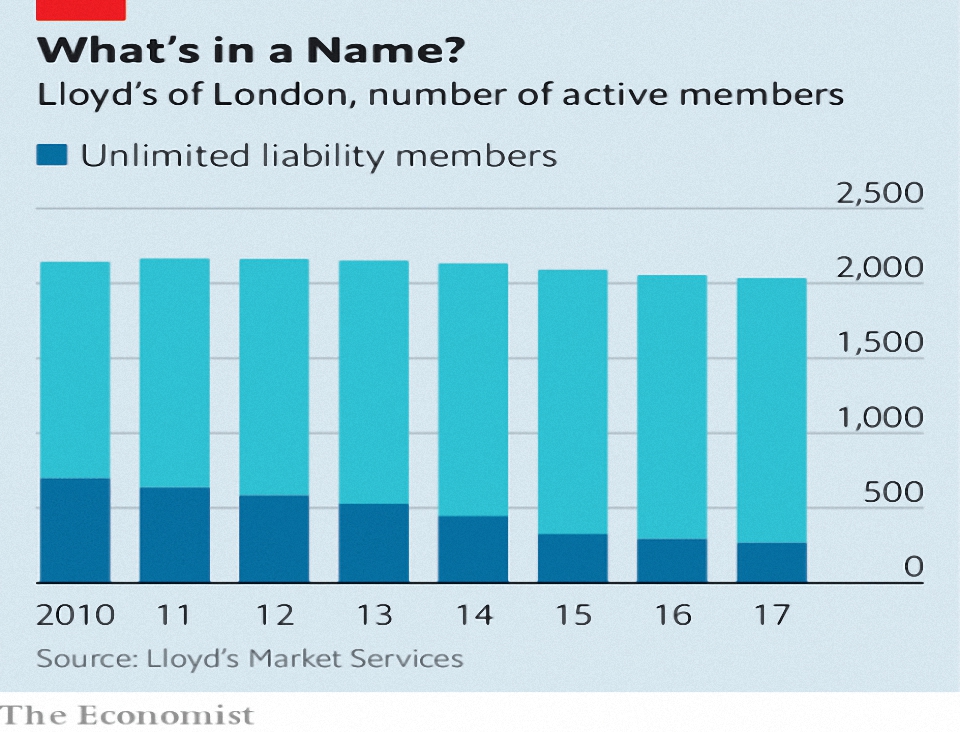

Lloyds

The Economist also reported that Lloyds names face two years of negative returns from hurricane losses.

- They also form an ever-shrinking source of capital to the insurance market – now contributing less than 10%.

There were 34,218 Names at their peak in 1989, but now there are only around 2,000 left, of which only 240 have unlimited liability.

- Most are men over 60.

The chief lure is that the system allows money to be used twice.

To insure £1m worth, say, a Name needs to commit about 55% in assets as “funds at Lloyd’s”, but can continue receiving interest or dividends on it.

There are tax advantages to boot.

Returns used to average 10% on the amounts insured, and therefore close to 20% pa on the funds deposited at Lloyds.

- But natural disasters have meant losses in 2017 and 2018 of 21% and 8% on funds deposited.

These losses will wipe out reserves and Names will need to “reload”.

- With the prospect of more natural disasters in the future, some will not.

Growth and stock markets

We’ve written previously on the weakness of the link between economic growth and stock market growth.

- This week Buttonwood returned to the topic.

He started by looking at index composition:

Most of the growth in the world’s GDP over the next five years will be in developing countries, says the imf. You might like to buy a basket of stocks from a broad range of countries that taps into this growth.

But the benchmark MSCI emerging-market index does not really offer that.

It’s light on Africa and heavy on the Asian supply chain to the rich world.

- The mismatch comes from the classification of countries by GDP per head, but markets by liquidity and openness.

Korea and Taiwan are rich countries, but they are developing stock markets.

- Between the two and China, that’s close to 60% of the EM index.

A stock index measures what is investable. If you are seeking exposure to broad-based economic development, you need to be creative.

That means looking at smaller, less liquid stocks outside the index, or perhaps the shares of rich-world firms that earn the bulk of their revenue in developing countries.

The alternative is the “frontier market” index, but even that is dominated by Kuwait, Vietnam and Argentina.

Even in the rich world, the mismatch persists:

- The US, UK and Switzerland have outsize markets, and Germany and Italy have small ones.

Big Picture Investors

Regular readers will be aware that since January I’ve been organising a Meetup group in London around Passive Investing in ETFs.

- If this is news to you, you can find out more about the London Passive Investing Club here.

And you can register for the next meeting here.

I’ve finally got around to setting up a companion group for active investors.

- It’s called Big Picture Investors and you can find out more about it here.

You can register for the inaugural meeting here.

Quick links

I have ten for you this week:

- The FT looked at Facebook launching its own currency.

- And wrote about the risk of a tech cold war.

- FT Adviser reported that P2P property platform Lendy has entered administration.

- The Adventurous Investor looked at Safety in Size.

- And wrote about Home Bias.

- Alpha Architect looked at volatility anomalies.

- And wrote that Volatility Targeting improves risk-adjusted returns.

- UK Value investor looked at Cranswick.

- ERN wrote about how to lie with personal finance.

- And Flirting With Models looked at how to disprove a signal.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.