Weekly Roundup, 29th November 2021

We begin today’s Weekly Roundup with inflation again.

Inflation

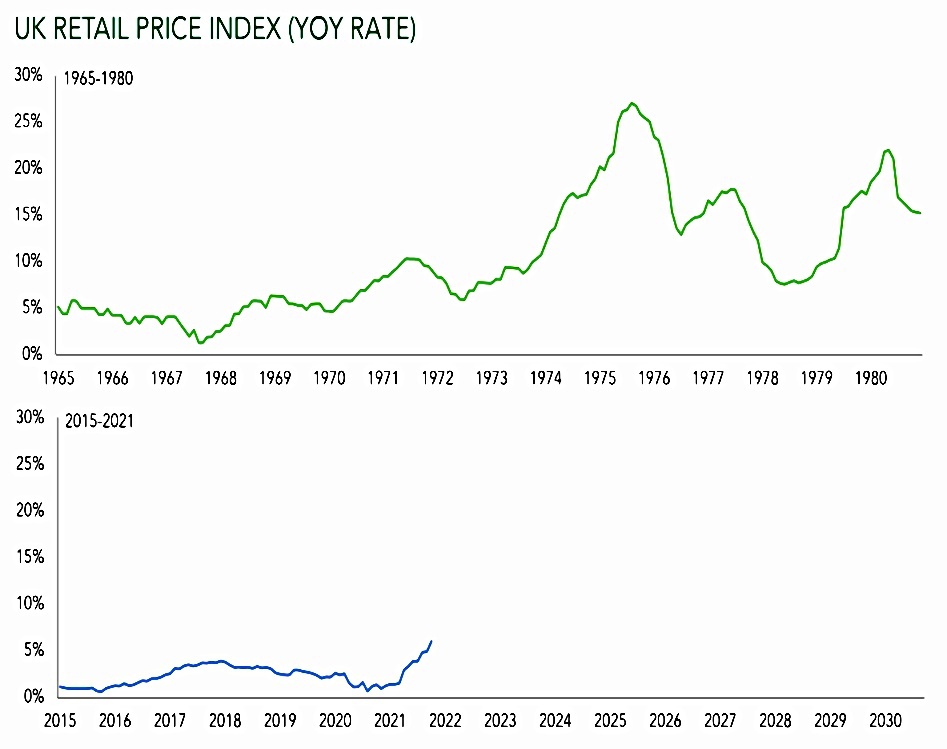

Hermoine Davies of Ruffer compared current inflation with the 1970s.

Investors have divided into two camps. Those who believe inflation will subside and the rise in prices will prove temporary. And others who fear we are entering a period of high sustained inflation reminiscent of the 1970s. We consider both scenarios unlikely.

That said, Ruffer do expect inflation volatility, and for the gap between interest rates and inflation to widen to produce ever more negative real yields.

The Real Fed Funds Rate was below -6% in October. That’s lower than at any point in the 1970s.

But they don’t foresee energy costs increasing by 10x, or a wages spiral, both of which happened in the 1970s.

When Britain’s coal miners ended their 1972 strike by accepting a pay increase of 35%, roughly 50% of the workforce was unionised. Today that has fallen to 24%.

Nor do they see interest rates rising much.

The government debt to GDP ratio for developed economies has risen from 20% in the 1970s to over 100% now.Governments have become addicted to zero-cost borrowing and cannot afford for it to increase.

And of course, higher rates would hit stocks and many bonds.

Meanwhile, The Economist wondered whether anyone actually understands inflation.

- Fed researcher Jeremy Rudd has posted a discussion paper on whether expectations drive inflation.

When workers expect prices to rise, they demand higher wages. When firms expect costs to rise, they set higher prices. In both cases, inflation becomes a self-fulfilling prophecy. Central bankers’ task is to pin down expectations at a low, stable level.

This has worked well for 30 years, but Rudd thinks that the theory is flawed.

Models of inflation mostly include expectations as a short-term variable (the next month or two). Central bankers and analysts think of them as a longer-term force, an underlying trend impervious to cyclical ups and downs. And whose expectations matter? There are ordinary people, businesses, forecasters and investors. None is much good at predicting prices.

Rudd argues that the causality of recent years should be reversed – observed low inflation led to low expectations.

- Obsessing over expectations might make central bankers too confident in their ability to keep inflation low.

Tyler Cowen of George Mason University points to hyperinflation as proof that expectations matter (at the limit, at least).

- Ricardo Reis of the LSE says that a combination of expectations, money supply, unemployment and interest rates is needed, but that expectations (on costs, for example) clear guide the price-setting of firms.

Adam Posen of the Peterson Institute argues that the key thing is for people to believe that the central bank will kill rising inflation.

Their credibility stems more from responses to crises than from attempts to manage expectations.

Rudd agrees with this, saying that it is best that inflation is not on people’s radar.

- So does Janet Yellen, who said that expectations only take hold after the central bank holds inflation near its target over a period of years.

What does this mean for today?

The hawkish view is that central banks must rein in prices before it is too late and

expectations lose their anchor.

The dovish view is that letting inflation overshoot could reset expectations.

- Which, on balance, is probably what governments and central banks want.

Startups

In his “Wealth Man” column for the FT, Jason Butler told the story of his investments in startups.

Over the years, I’ve invested in several startups. Sadly, many have lost money.

But I’ve also learnt some valuable lessons.

The most recent chapter – and possibly the most successful – is the sale of Finimize (Jason invested, and also mentored its founder) to Abrdn.

Jason recommends a few ways to reduce risk:

- Diversify (this takes a lot of capital if you want access to the high-quality opportunities not found on equity crowdfunding sites)

- Take advantage of tax reliefs (on the initial investment and on any losses), including investors’ relief for those businesses which don’t qualify for EIS/SEIS

- Invest in businesses and industries that you understand

- Make sure the fundraising is large enough to get the business through to the next one

- Invest in people, not revenue projections

All good stuff, but most people (including me) don’t have enough money to invest in a diversified portfolio of startups.

- The nearest I can get is VCTs, which fund later-stage firms will naturally slower growth (and hence somewhat lower potential returns).

Crypto

In the FT, Joshua Oliver wrote about the pressure on wealth managers and financial advisors to incorporate crypto into their plans (even though they themselves remains sceptical).

A survey for WisdomTree found that:

- 70% of advisers have spoken to clients about crypto, but

- 42% of UK wealth clients planned to invest in crypto outside of this relationship

Goldman Sachs says that 15% of global family offices already have exposure to crypto.

Those who want to commit substantial funds can struggle to find support. The mainstream wealth managers on whom they often rely for investment advice have largely stayed on the sidelines of frothy crypto markets. This is particularly true in the UK, where the authorities have taken a tougher line on crypto than in some other developed economies including the US.

Chris Woodhouse, CEO of Tilney Smith & Williamson said:

We’re in the business of managing the monies of widows and orphans for the long run. Things like cryptocurrencies don’t really figure in that. It would need to be a more developed and regulated market.

Andy Croft, CEO of St James’s Place said:

We’re not offering crypto and we’re not planning to.

Michael Bolliger, chief investment officer, emerging markets, at UBS Global Wealth

Management, thinks client queries are driven by FOMO:

You have your buddies at the golf club. They claim rightly or wrongly that they have made a fortune. You don’t want to be the last person standing in the queue.

Progress is better in the states:

Morgan Stanley’s wealth division opened up three bitcoin funds to US clients in March, followed by JPMorgan in August with half a dozen fund choices for their US client. Goldman Sachs will also link global wealth clients with crypto funds. Citi Private Bank acknowledged that an increasing number of clients are posing questions about crypto, but said its still working out what it might offer.

Jamie Dimon, CEO of JPM, said:

Our clients are adults. If they want to have access to buy or sell bitcoin we can give them legitimate, as clean as possible, access.

Joshua says that wealth managers are worried about valuation (because of a lack of future cash flows), and also about safe storage (given the regular hacks of crypto custodians).

Also in the FT, Lucy Kellaway (former columnist turned teacher) reported on the classroom craze for crypto.

- Teenage boys are hooked, apparently.

There is the cool language of technology and an endless drip-feed of hype on social networks. Digital currencies are thrillingly anti-government and rebellious, but the best thing about them is their promise of easy, instant money.

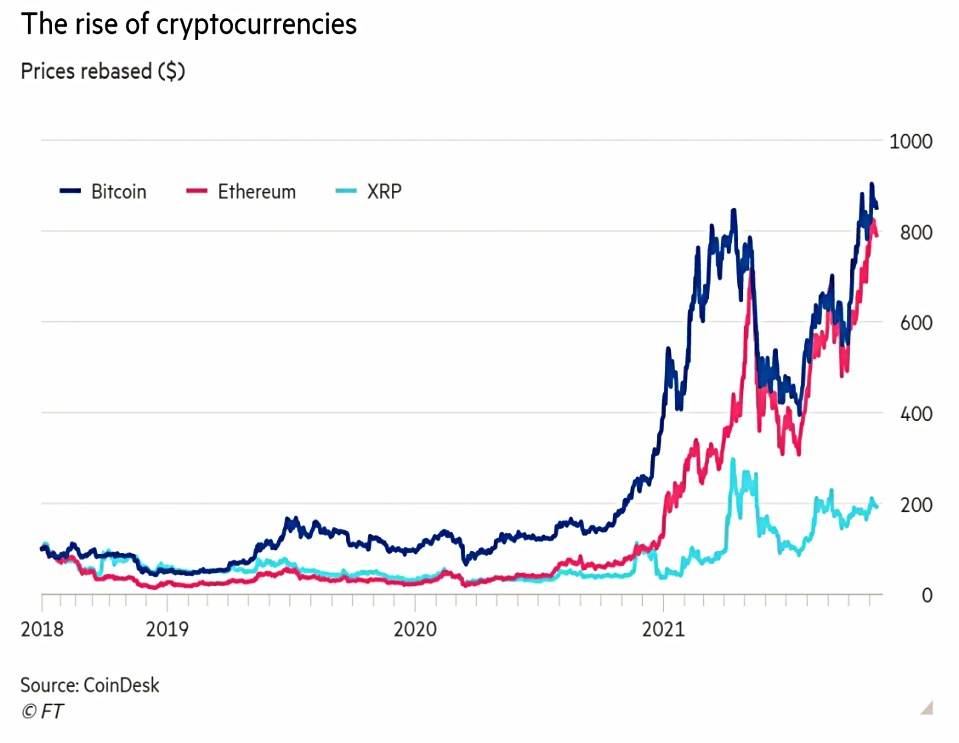

Bitcoin has gone up from £600 to £45,000 in five years — a rise of 7,400 per cent — and to the untrained teen mind this is all the evidence needed that the rise will continue.

It’s also illegal of course, until age 18.

Some have persuaded parents or other adults, many of whom themselves are financially unsavvy, to set up accounts for them. Others buy the coin at ATMs or exchange Amazon gift cards for bitcoin.

Lucy also describes how she failed to persuade her class about the dangers of meme stocks like GameStop.

I explained to the class short selling. I explained that this was turning into a giant Ponzi scheme. I showed them the steeply rising share price graph and asked them to put up their hands if they would invest now. Never mind all my warnings, the hand of almost every child in the class shot up into the air.

Their interest in money gets in the way: such is the desire for profit that dry warnings about losses have no impact at all.

And not just children, unfortunately.

Our third crypto story comes from Business Insider, who reported comments from the Bank of England’s deputy governor to the effect that Crypto-assets are becoming a potential threat to the global financial system.

Jon Cunliffe said on Radio 4:

My judgement is they are not at the moment a financial stability risk. But they are growing very fast, and they are becoming integrated more into what I might call the traditional financial system. So the point at which they pose a risk is getting closer, and I think regulators and legislators need to think very hard about that.

In the same interview, Cunliffe pumped the potential for a UK CBDC:

[This could] anchor and hold together our monetary system. The way we live and the way we transact is changing all the time. Our lives are becoming more digital. And as that happens, the way we use money and the money we hold changes.

The question is whether the public at large — businesses, households — should really have the option of using and holding the safest money, which is Bank of England money, in their everyday lives.

He wasn’t worried by the private sector “stablecoins” like Facebook’s Diem (formerly Libra):

There are proposals from new players who are not banks, including some of the big tech platforms. But those don’t yet exist at scale. So I don’t think we’re behind the curve here on regulation and management.

Quick Links

I have eight for you this week, the first four from The Economist:

- The newspaper said that Erdogan’s zany monetary experiment is impoverishing Turkey

- And that a bright new age of venture capital is here.

- A second article fleshed out the concept of adventure capitalism

- And The Economist also looked at US inflation.

- Alpha Architect reported that value is cheaper now than a year ago

- And wondered whether we should ever invest in individual stocks.

- UK Dividend Stocks used the CAPE to show that the S&P 500 is massively overvalued

- And Mauldin Economics said that shortages are relative.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.