Options 3 – The Retirement Manifesto

Today’s post is the third in our series on options trading. We look at the options strategy used by Fritz over at The Retirement Manifesto.

Contents

ERN’s options strategy

In the previous two articles, we looked at the strategy used by ERN from the Early Retirement Now blog.

- ERN is responsible for a mammoth series of blog posts on safe withdrawal rates.

Here’s what we found:

- People have an aversion to negative skew, which means that they overpay for insurance and lottery tickets.

- This seems to be related to the over-weighting of salient but unlikely events (which does not contradict Taleb’s assertion that we underweight “impossible” events.

- So selling insurance and/or lottery tickets can be profitable.

- Selling insurance (writing options) is the easier of these two strategies for private investors to implement.

- Options are not as complicated or (necessarily) as risky as most people imagine.

- ERN successfully uses a strategy of selling ATM index puts in large size.

- ERN uses Interactive Brokers as they have the cheapest per contract commissions.

- ERN’s account size is more than $660K and is now 35% of ERN’s net worth, and around half of his net worth outside retirement accounts.

- He uses the shortest contract possible, which means that he normally writes options that expire in one or two trading days.

- He thinks this means that he gets bigger premiums per unit of risk.

- He also likes to have the maximum number of independent bets in order to access the “house edge”.

- ERN uses leverage for two reasons:

- To boost the return from the likely base rate

- To overcome taxes – ERN uses a 1/(1-tax rate) approach as a minimum.

- For a 20% tax rate, this would mean gearing of 1/0.8 = 1.25 times.

- The delta on a typical put that ERN writes is 0.15, which means it is 15% as volatile as the underlying.

- So even with say three times leverage, the volatility would be much less than the underlying.

- Long-term, ERN expects a 12% gross return (8.5% after-tax) with around 7% volatility, which is a lot better than the index.

- From 2000 to 2018, through two bear markets and two bull markets, the strategy outperformed the S&P 500.

- It also had lower volatility (10% pa, cf. 15% for the S&P 500) and it had smaller and shorter-lived drawdowns.

- The strategy also traded successfully through October 2018 – the worst month for the S&P 500 for seven years, down 7%.

- The market never dropped much below ERN’s strike prices.

- At the time of the last update, ERN was using reduced leverage of 2-2.5 times.

- The time value of the options had been reduced from 7% down to 5-5.5% pa.

- Using a $300 premium target on a nominal option value of $280K gives an unleveraged return of 5.57%.

- ERN now targets strikes that are 5 Delta or 1.5 to 2 standard deviations below the index level.

- The loss allowance (how much premium will need to be given back) has been increased from 50-55% up to 60%.

- Returns are 4.7% from the options and 4.6% from the margin cash portfolio.

- That’s a 9%+ return overall, or more than 7% above 2% inflation expectations.

- That’s better than long-run stocks with better drawdowns and lower volatility.

The Retirement Manifesto

We first met Fritz back in 2017, when he started a couple of chains of linked posts by finance bloggers on both sides of the Atlantic, to which 7 Circles contributed posts.

- The first was about Drawdown Strategy.

- And the second was about a measure of savings call the Fire Prowess Gauge.

But it turns out that Fritz also trades options.

Fritz’s options strategy

ERN only uses a single strategy, but Fritz uses three:

- Sell a put

- Sell a call

- Roll a position

He also uses TD Ameritrade (ThinkOrSwim) rather than Interactive Brokers.

- And his account is less than 10% of his net worth, compared to 35% for ERN.

He illustrates the first two techniques using John Deere stock (DE) in 2014.

- With the stock trading at $88, he sells a put at $84.

- So if the stock trades below $84 when the option expires (in a couple of months), Fritz has to buy it.

- Selling the put earned $110 on a 100 share lot (ie. an underlying value of $8,400).

- This is a 7.9% annualised return – 110/8400*12/2

- Most puts expire without being exercised.

- Fritz might have 15 or 20 trades open over a given quarter (options period).

- Sometimes (when the stock price has increased significantly) Fritz will buy back his put for a much lower price (say $10 rather than the $110 he was paid to sell it).

- Let’s say the DE put is exercised at $84 and the stock is trading at $81.

- Because of the $100 premium, Fritz’s effective purchase price is $82.9

- But he’s still lost money – he’s down $190 with the stock price at $81.

- But his purchase price is much lower than the $88 DE was trading at when he wrote the put.

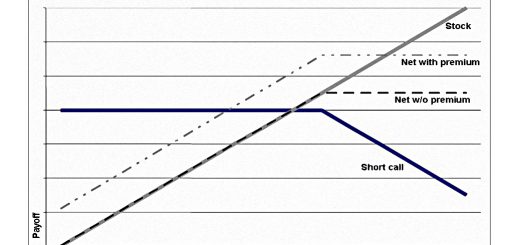

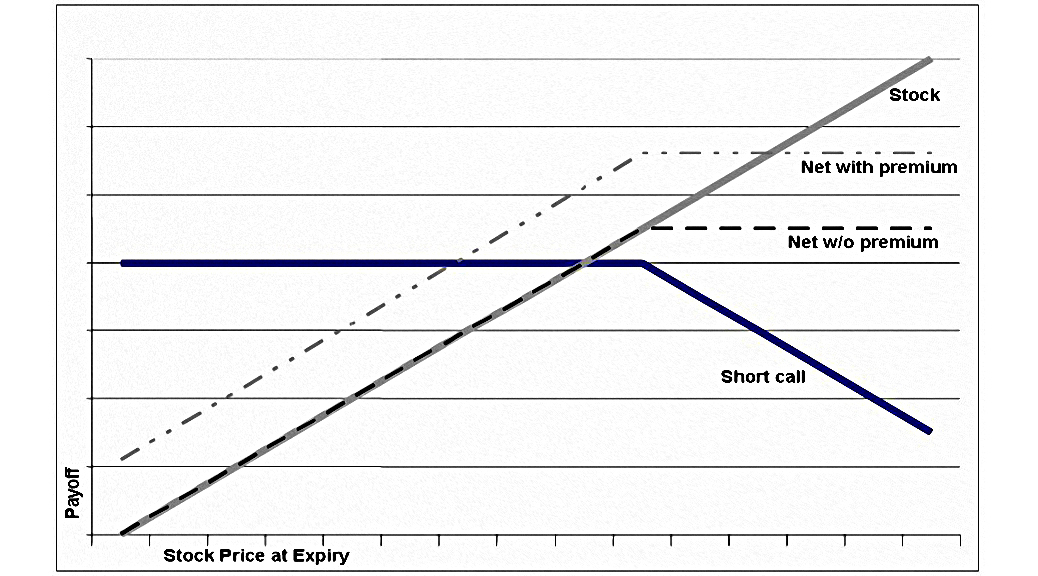

- Now Fritz sells a covered call at $90 strike in three months time.

- This means he has to sell if DE is trading above $90 in three months.

- He gets $86 for this, which means his entry price is now $82.

- But often the call won’t be exercised, and Fritz just sells another one.

- At the time of his article, Fritz had “sold” DE seven times for accumulated premiums of $968.

- He still owns the stock and receives the dividend.

- But he’s earned 7% pa on top from call premiums.

Rolling a position

When the stock price is above the strike and a call expiry is looming, but Fritz doesn’t want to sell, he rolls his position.

- In May 2016, DE was trading at $82, above the $80 strike of Fritz’s call.

- So he “rolled” his position from May 16 expiry to Sep 16 expiry.

- This earned him another $252 in premiums.

- The roll is two trades – buying back the May call (which cost $320) and selling a Sep call (which earns $572).

You might also roll the initial put if the stock is trading below the strike price and you would rather not have to buy the stock.

Over the 18 months that he’s held DE, Fritz has received a total of $1,000 in premiums, which takes his cost basis down by $10 from the $84 he first paid.

Risks

Fritz outlines the risks that come with this strategy:

- You may be forced to buy a stock at a price higher than market price when your put

expires. - You may be forced to sell a stock at a price lower than the market when your call

expires. - Your call may be exercised before the expiration date, which means you’d be forced to

sell the stock at the call price.

In addition, you have to maintain sufficient cash in your account to pay for any forced purchases, or else pay to borrow money “on margin”.

- And the potential frequent trades can increase your expenses.

Conclusions

Now we have a second, complementary strategy to investigate.

The one thing I would have liked to have seen is some backtesting/data on historical returns for this strategy.

- I think ERN mentioned that covered calls had a similar return to his out of the money puts, but I’d rather hear this from someone who is using the technique.

We have options strategies from several more bloggers to get through, so I’ll be back with another one in a few weeks.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.