Rethinking 60-40 – Part 2

Today’s post is our second visit in 2021 to the topic of whether the traditional 60-40 stocks/bonds portfolio still makes sense.

Contents

Recap

Here’s what we looked at last time out:

- Stocks are riskier (more volatile in price) than bonds but have higher long-term returns.

- The logic of blending two assets together comes from the idea that their prices will move in different directions.

- When stocks go down, you hope that bonds will move up in price.

- The riskiest portfolio recommended by financial advisors to customers with differing levels of risk appetite would be 80-20 stocks/bonds – and the safest would be 40-60

- So the 60-40 portfolio can be thought of as the middle option of three.

- In fact, bonds are a pretty bad hedge for stocks in any case, unless you either hold a lot of them (bad for overall returns) or use a lot of leverage (risky).

- But the 60:40 portfolio is easy to understand and has proved pretty easy to market to investors.

- It’s also done pretty well over the decades, so many investors would miss it.

- The need to rethink 60-40 all starts with the prospect of higher inflation and its potential impact on the bond-equity relationship.

- If inflation rises for an extended period, this could be bad for both stocks and bonds.

- In quant speak, the bond-equity correlation might turn positive.

- This is actually the normal relationship, but in recent years, investors have become used to bonds rising when stocks fall.

- In particular, recession-driven stock market crashes lead to a demand for safe-haven assets, which are traditionally government bonds.

- So the price goes up, and the yield goes down.

- When the economy recovers, so do stocks, but bond prices fall back.

- But as bond yields approach zero during the good times, they don’t have far to fall in a crash.

- And so they have a limited ability to protect you.

- And with bond yields close to rates on savings accounts, there’s little incentive for private investors to hold bonds at all.

Alternative assets

The simplest fix is to replace bonds with alternative assets:

- The obvious candidates are gold and cash.

- More adventurous investors might consider other precious metals, commodities in general, private equity and venture capital, hedge funds, infrastructure funds, royalty companies and even crypto (particularly in combination with gold).

- Real assets – like property, art and farmland – are another way to go.

- most investors in the UK have too much property exposure through their home (since prices are high)

- if you do choose property, be selective – perhaps choose warehousing over office space and retail

- the other two assets are difficult and expensive to access.

- Older investors, in particular, might also have DB pensions, which act as a bond portfolio without you choosing to own bonds.

Reports

In the previous article, we looked at reports on this topic from State Street and JP Morgan. Interesting points included:

- Bond returns are driven by the coupon (yield) – these are currently low

- Stock returns are inversely related to starting valuations (eg. PEs), which are currently high

- The projected return on 60:40 is now just 3.5% pa

- More esoteric bonds offer higher yields, but also higher correlations with equities

- Factor premia (smart-beta funds) are another asset class to look at

- Patience and diversification are required since no single factor works all the time and many factors underperform for years (eg. value right now).

- So are hedge funds (particularly long-short equity, which is not readily available to DIY investors, and global macro, which is), options and managed futures (trend-following).

- The last two are very much DIY pursuits.

Rethinking 60-40 – Part 2

Humble Student

Since my first article on this topic, I’ve come across four other pieces on similar themes.

- Let’s take a look.

First up is Cam Hui of the blog Humble Student of the Market.

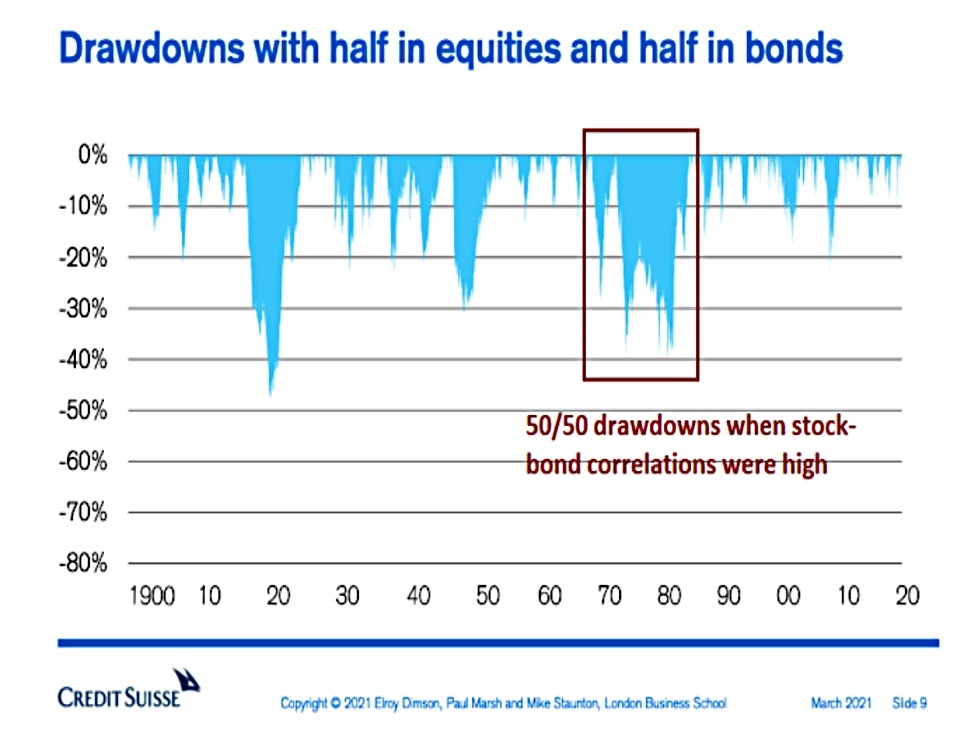

- In a post entitled 60/40 resilience in an inflation age, he notes that stock-bond correlations increase with rising inflation, preventing bonds from providing resilience in the 60/40 portfolio.

Drawdowns can reach 40%.

The Singapore and Norway sovereign wealth funds have said the same thing.

- Singapore notes that we should expect lower returns going forward, and Norway has moved to a 70/30 target model (and is actually holding 73/25).

Ray Dalio’s Bridgewater has moved to use gold and inflation index-linked bonds (linkers) instead of sovereign bonds in its risk parity fund.

Cam says that linkers would be the logical substitute, but they were not traded during the last inflationary period (the 1970s).

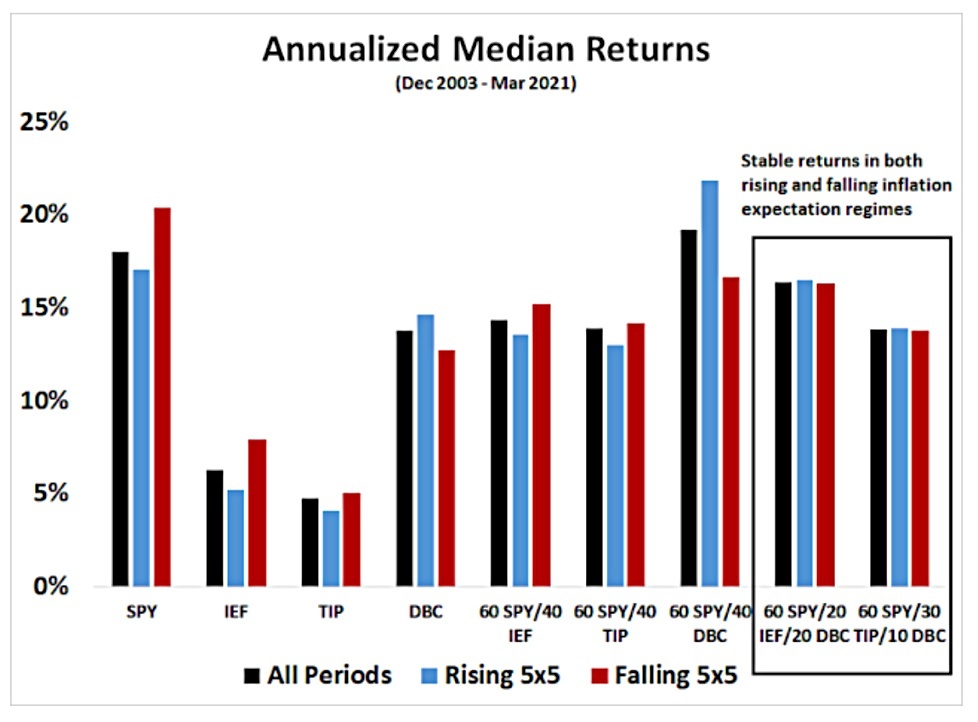

- So he has used 5×5 forward inflation break-even “expectations” to analyse assets from 2003 onwards (when the 5×5 data begins). (( The 5×5 uses the difference in market interest rates, over 5 years, starting in 5 years – so between a 10-year and a 5-year bond ))

He looked at four assets:

- Stocks (SPY)

- 7-10 year bonds (IEF)

- Linkers (TIP), and

- Commodities (DBC)

And five portfolios:

- 60/40 stocks/bonds

- 60/40 stocks/linkers

- 60/40 stocks/commodities

- 60 stocks, 20 bonds, 20 commodities

- 60 stocks, 30 linkers, 10 commodities

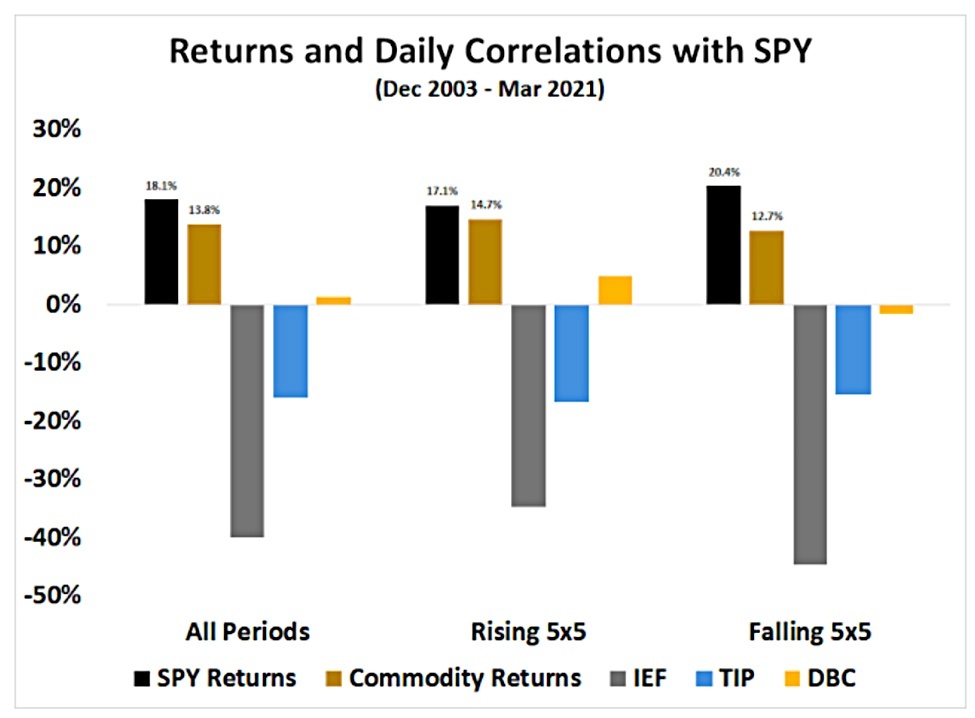

Because the period since 2003 has largely seen falling inflation, Cam divided the returns between periods when the 3-month average 5×5 was rising and when it was falling.

Cam makes four points:

- Stocks prefer falling inflation

- Bonds are diversifying even with rising inflation, but as their yields rise, they will lower portfolio returns

- Linkers are less diversifying but will impact returns less

- Commodities have close to zero correlation, but slightly positive when inflation is rising – they also have good returns, particularly in rising inflation

Cam also notes that gold could be used instead of (or I would argue, as well as) commodities.

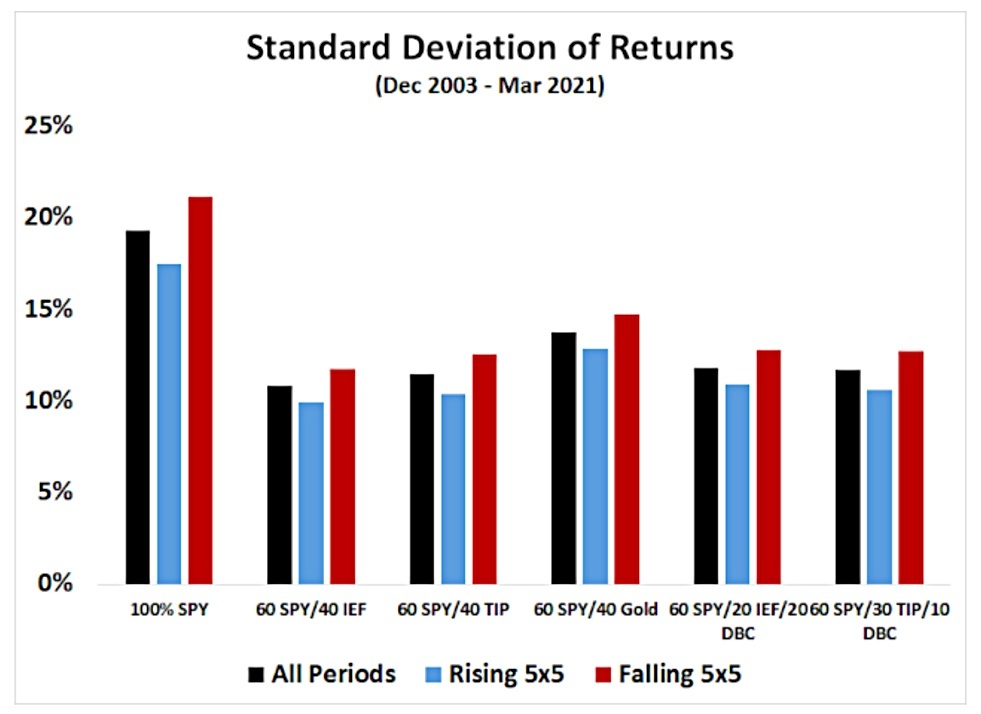

As we find so often, the more diversified portfolios were more stable.

- Cam didn’t test this, but I would look at a portfolio of all four assets (and more).

Cam adds a caveat:

While my study showed a negative stock-bond price correlation, the historical record shows that stock prices were negatively correlated to the 10-year Treasury yields and therefore positively correlated to bond prices during periods of high CPI.

I conclude that my study only represents a broad sketch of asset return characteristics and it does not represent an exact roadmap of what investors might expect during a period of strong inflation.

Orbis

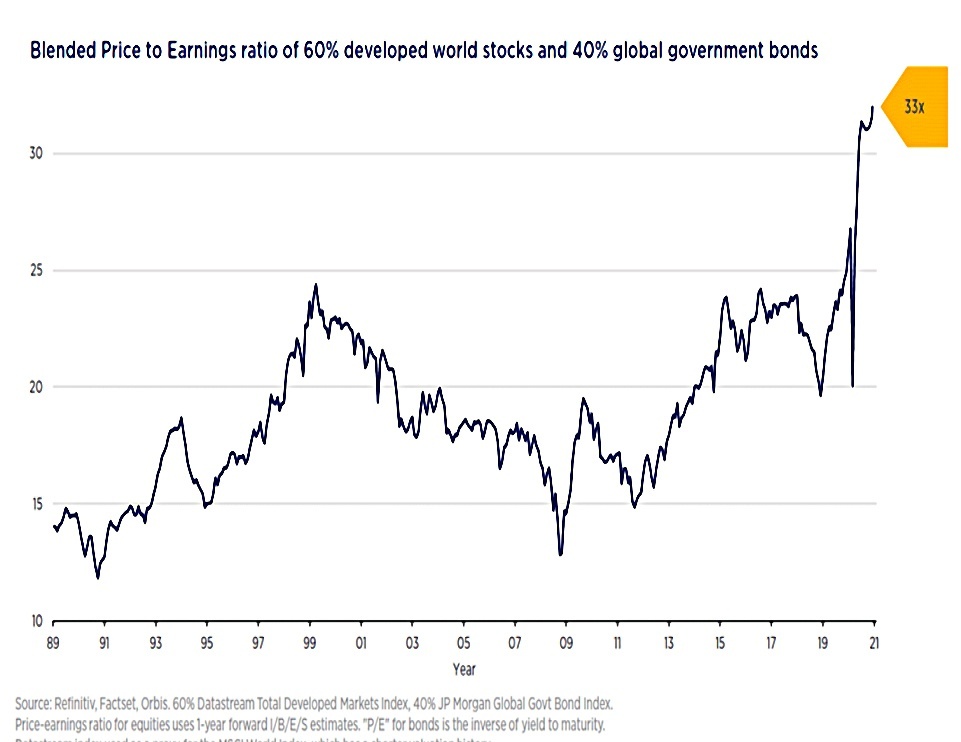

Orbis emailed me a chart reminding me that the classic 60/40 is not a lower-risk portfolio any more.

A traditional passive 60/40 portfolio is significantly more expensive than it has ever been.

The Orbis approach to solving this problem is bottom-up:

The equity portion of our Global Balanced Strategy has more than a 90% Active Share, meaning that there is a less than 10% overlap with the equity portion of its benchmark.

In contrast to the benchmark’s 40% component made of Government bonds, our portfolio instead comprises a mix of select corporate bonds, gold, inflation-protected bonds, and hedged equity.

Factor Research

Nicolas Rabener of Factor Research looked at 60/40 portfolios without bonds.

He began with a dig at pension funds:

Their average allocation to bonds was approximately 30% in 2020, almost identical to 1999. Over that 20-year period, the U.S. 10-year government bond yield fell from 5% to a mere 1.5%.

So bonds have increased risk and lower prospective returns.

- Nicolas wonders whether the 40% bond allocation might be replaced with liquid alternatives in order to create an anti-fragile portfolio.

The usual suspects are real estate, PE and infrastructure, but Nicolas is sceptical:

None of these private asset classes represent true diversifiers – they, like stocks, depend on positive economic growth. On paper, they may seem to offer diversification, but that is due to smoothed and lagged valuations.

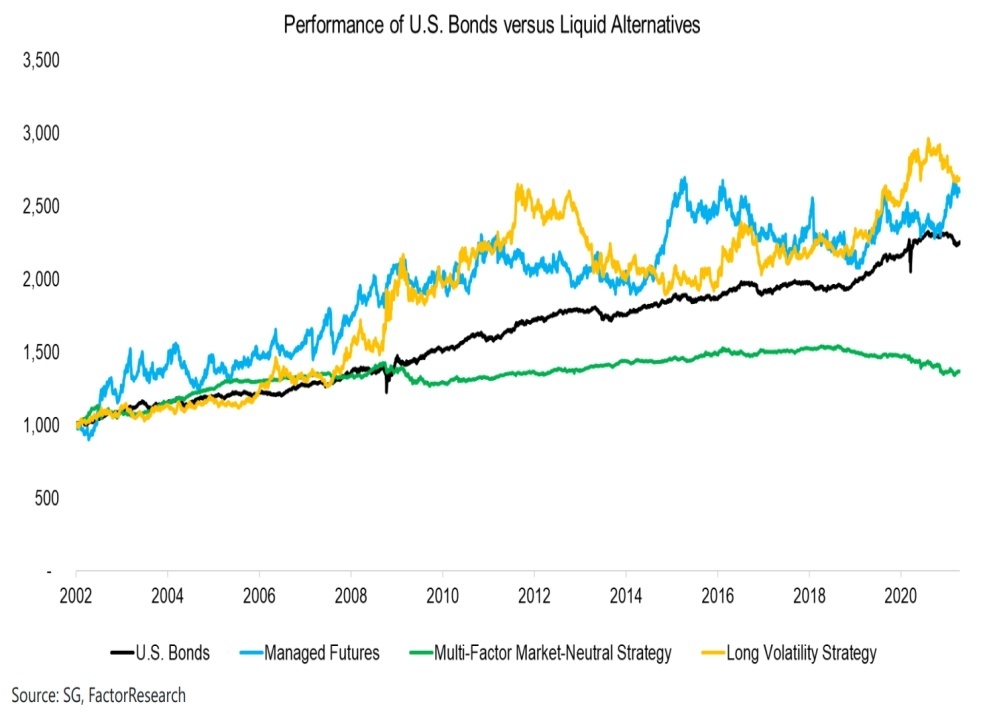

He looked instead at three alternatives:

- Managed futures (trend-following or CTAs)

- Multi-factor market-neutral, providing exposure to five equity factors (value, size, momentum, low volatility, and quality)

- Long volatility – a simple combination of JPY / AUD and gold (safe-haven instruments).

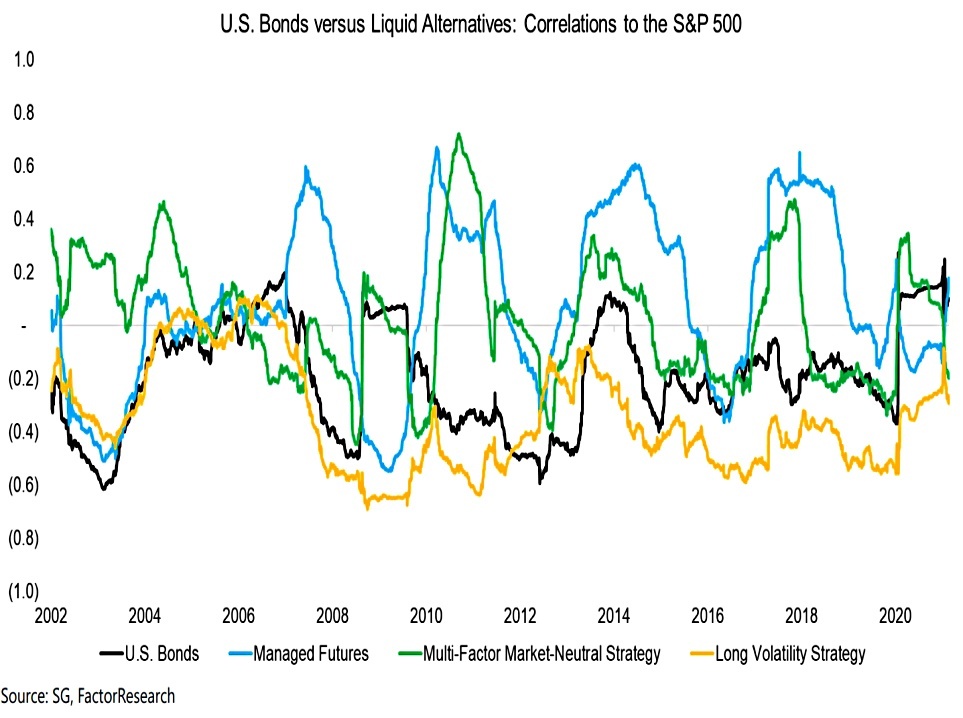

The first and third of these strategies generated similar returns to bonds from 2002 to 2021 (with higher volatility) whereas multi-factor generates a lower return with lower volatility.

Long vol generally has a negative rolling one-year correlation to the S&P 500, whereas the other two strategies have roughly zero correlation (similar to bonds).

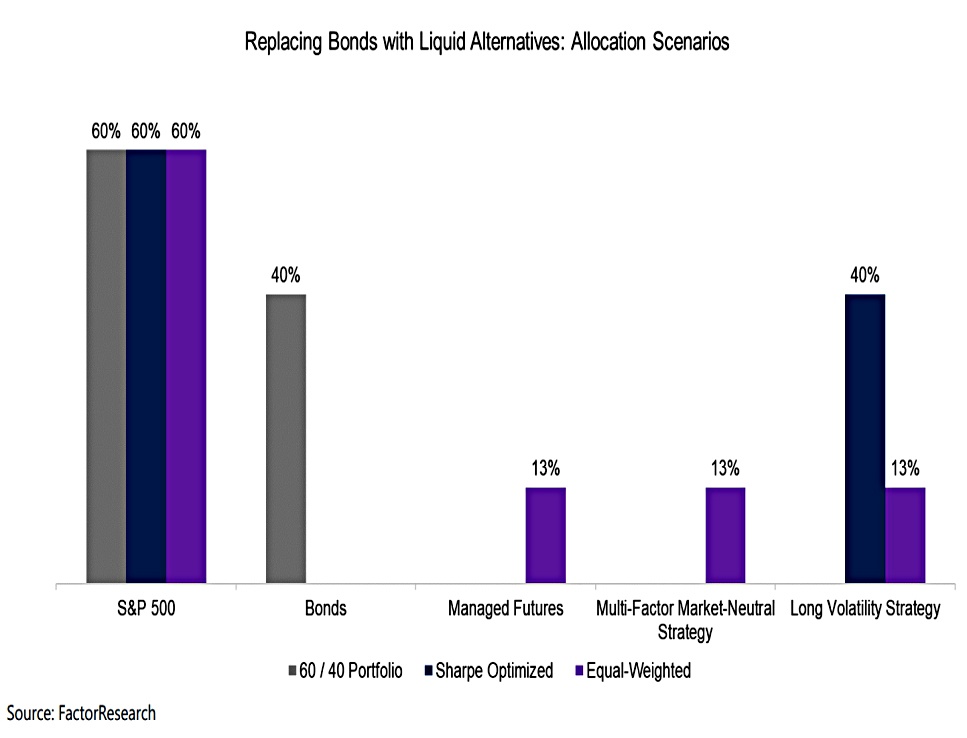

Nicolas looked at two alternative portfolios as well as the standard 60/40:

- A Sharpe-optimised portfolio, which ended up being 60% stocks, 40% long vol. (( Optimisation often produces these extreme weightings, which is why a “hand-crafting” approach can be better ))

- Splitting the 40% bond allocation over the three alternative approaches.

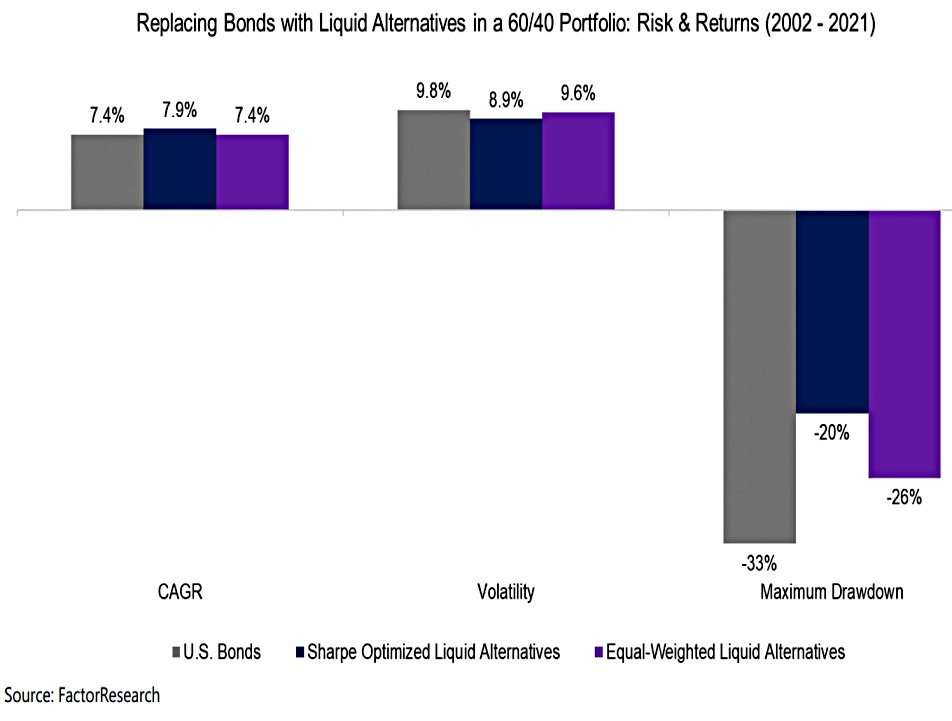

The optimised portfolio beats the 60/40 – it has a higher return, lower volatility and lower maximum drawdown.

- The equal-weight portfolio is also better than the 60/40, though only slightly.

Investors could have replaced bonds with liquid alternatives already and would not have incurred a worse investment outcome over the last 20 years.

Nicolas notes that these alternative strategies are not liquid enough to accommodate the entire existing fixed income allocation and that missing transaction costs flatter historic returns (though equally, bond returns might be expected to be worse in the future).

Conclusions

That’s it for today – the message is the same as last time:

- There’s no “silver bullet” asset that you can replace your bonds with (though long vol worked well historically).

But there are plenty of options that you can use together to achieve the same effect.

- Which ones you feel comfortable using is down to you.

I won’t revisit this topic for a while unless I keep finding interesting articles on bonds.

- If you spot any, let me know.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

As you say, no ‘silver bullet’.

Would you also consider the state pension to “act as a bond portfolio without you choosing to own bonds.”?

Hi Al,

Yes, I would and I do.

The state pension would translate to quite a nice bond portfolio if only it didn’t start at such an advanced age. I will have been retired for 16 years when I get mine.