The Value of Financial Advice

Today’s post is about a report from the International Longevity Centre. It’s called the Value of Financial Advice.

Contents

The ILC

The ILC describes itself as “the leading think tank on longevity and demographic change.”

- It claims to be non-partisan, but it accepts sponsorship from the industry (Legal and General, Aviva, and for today’s report, Royal London).

We’ve come across the ILC before:

- once when we looked at their report on annuities versus drawdown

- and before that when they called for a pensions commission

I can’t say that we’ve been too impressed so far.

The Value of Financial Advice

Before looking at the report, let me declare my position:

- I gave up paying for advice as soon as it was legally possible to access the products I needed without going through an advisor.

I believe that good advice is available at a price, but also that no investor need fail to reach their goals simply because they can’t afford access to a financial advisor.

- There are no secrets in investing, and everything you need to become a DIY investor is freely available.

The key finding of the report (which is based on the Wealth and Assets Survey) (( We shall return to this underlying report at a later date )) is that:

Those who take advice are likely to accumulate more financial and pension wealth, supported by increased saving and investing in equity assets, while those in retirement are likely to have more income, particularly at older ages.

That’s a great result for those in the industry, but I will dispute whether the report proves that paying for advice is necessary or good value.

The problem

It’s hard to disagree with the ILC when they say:

The human mind is not programmed to think long term, preferring rewards today over larger rewards tomorrow, and switching off in the face of complexity.

So it would appear that people could benefit from advice.

The advice market

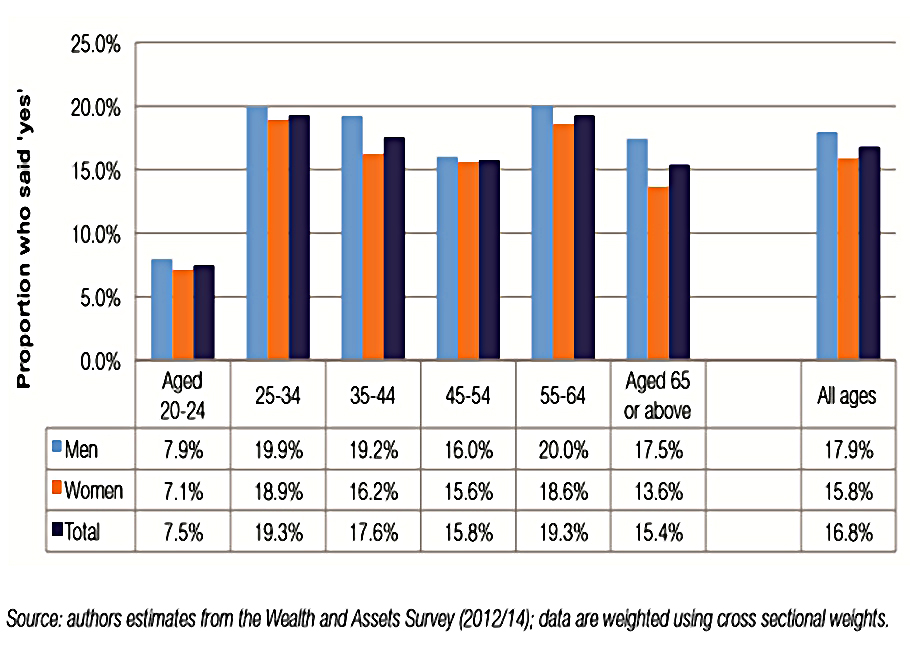

Yet only 17% of people saw an advisor between 2012-14.

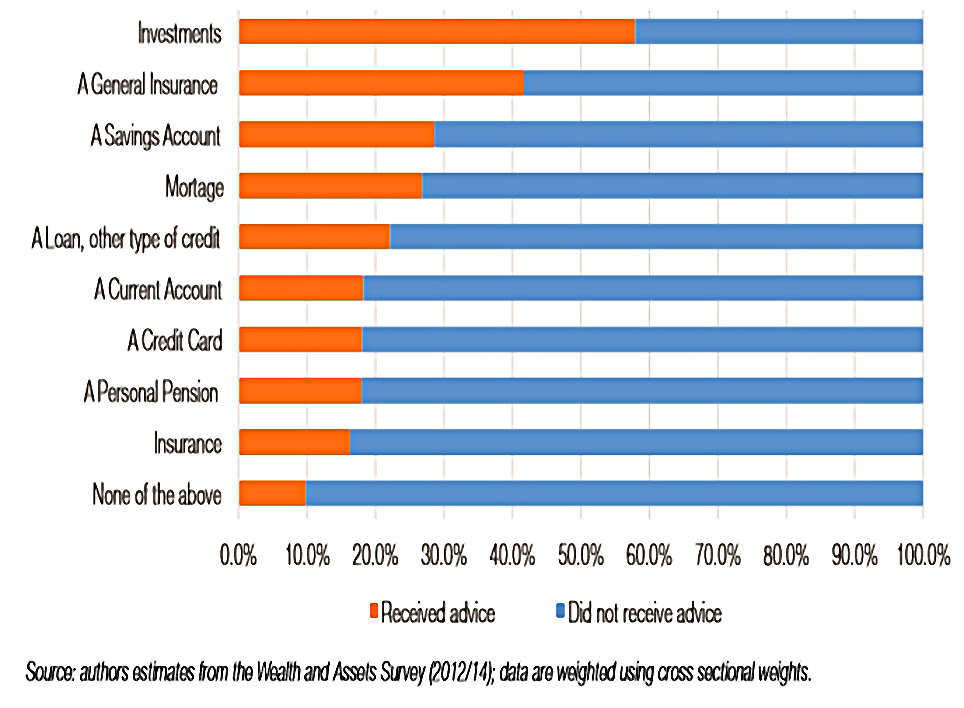

Only 60% of those who “bought” an investment product took advice.

- This figure falls to 22% for pensions.

Advice is most commonly taken by those aged 25-35 (for a mortgage) and those aged 55-65 (for pension access options).

30% of those who took advice thought that it was free, including 15% of those who saw an IFA.

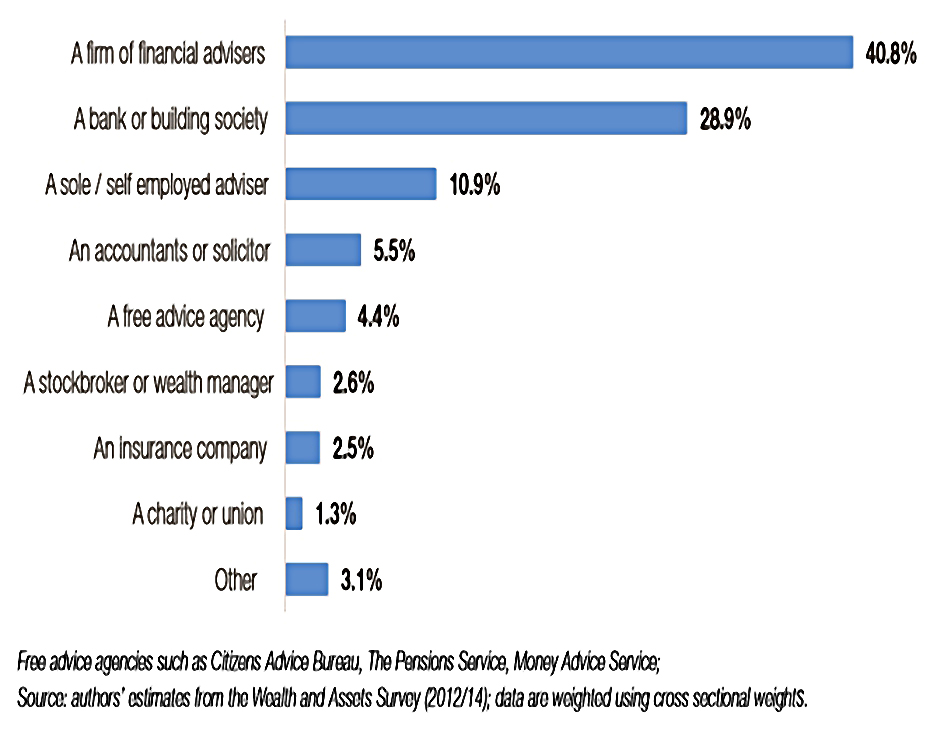

41% of advice came from IFAs, whilst 29% came from banks / building societies.

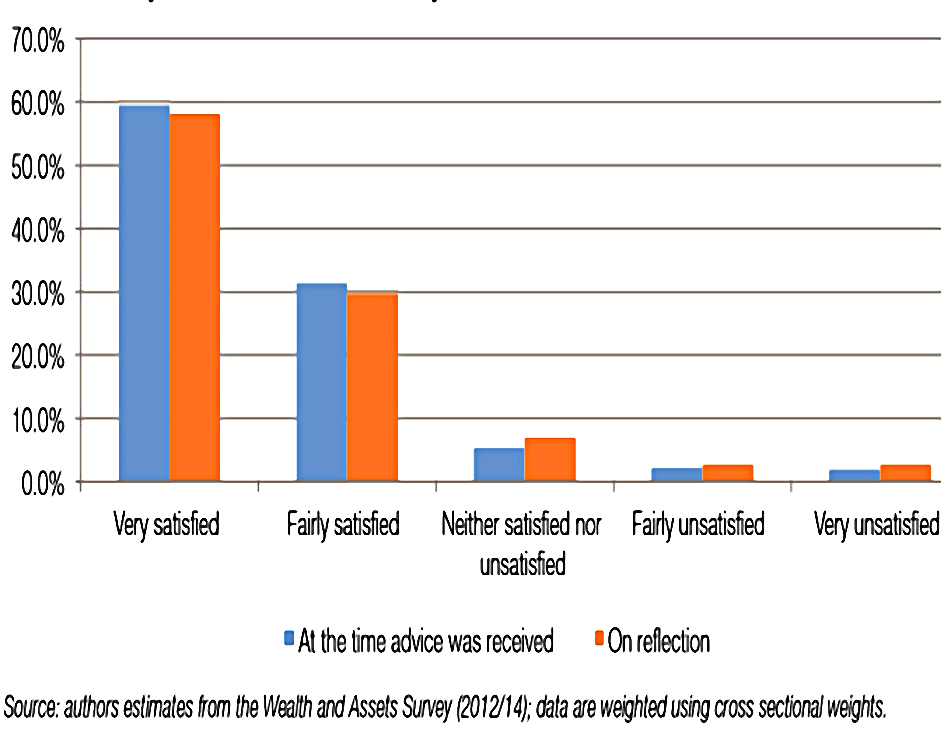

The ILC also note that 90% of those who took advice were satisfied with it, and 86% went with their advisor’s recommendation (made a “purchase”).

Few people needed a second opinion, with 63% speaking to only one advisor.

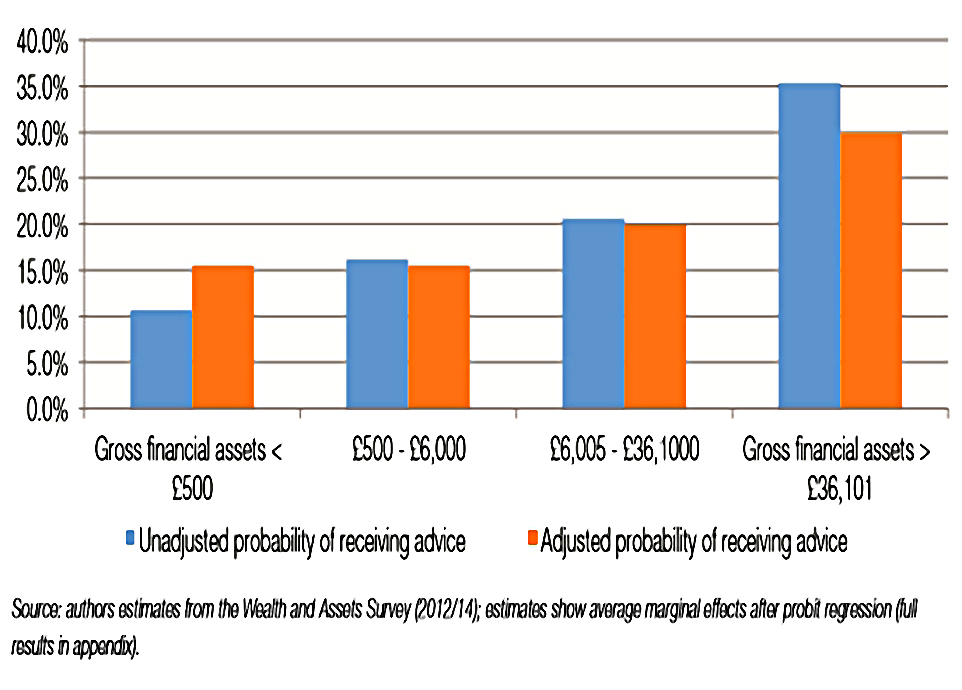

Demographics

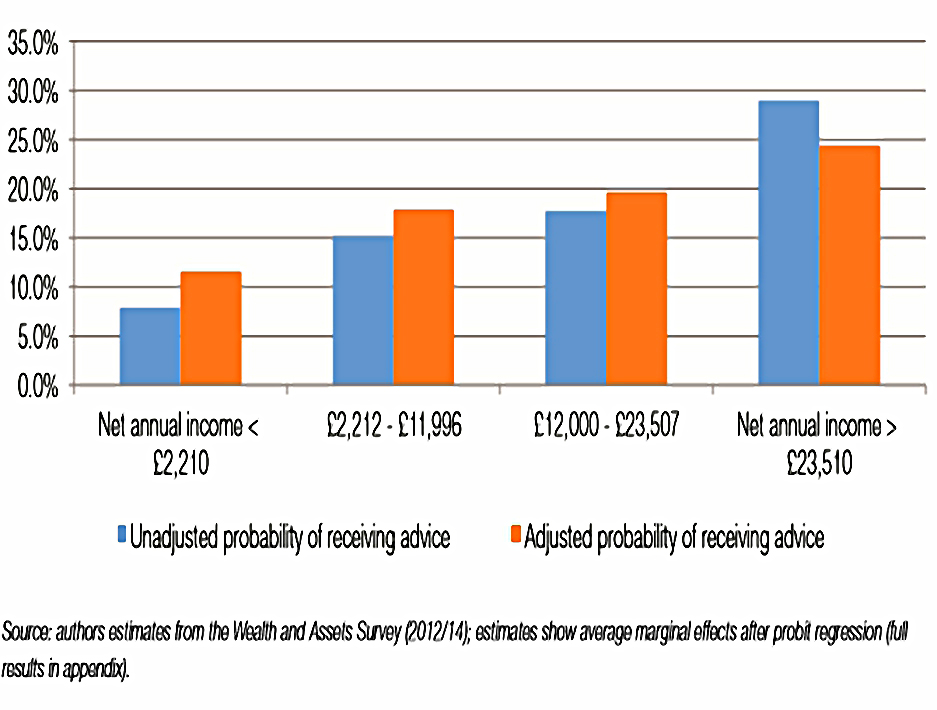

Rich people (whether measured by income or net worth) take more advice than poor people.

Financial capability is also a factor.

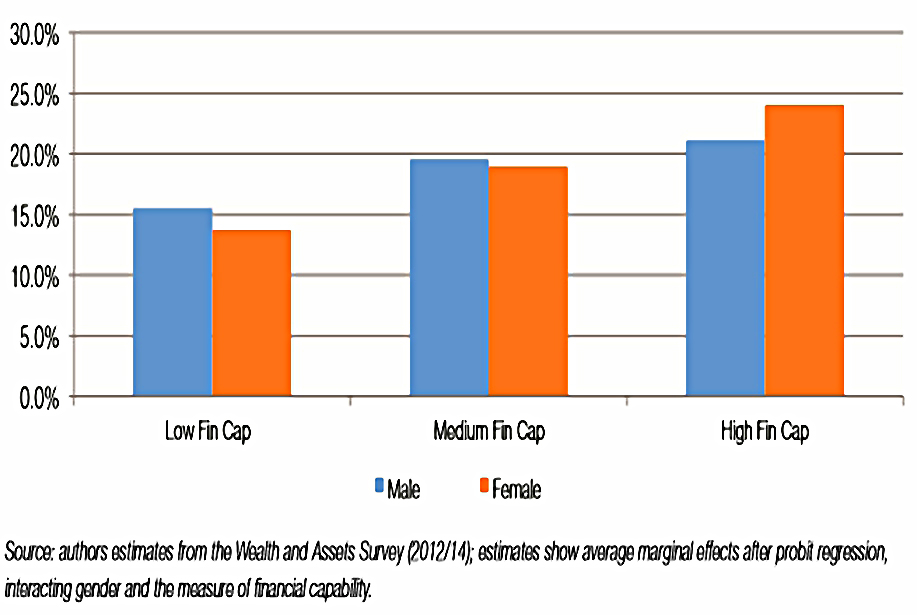

More men took advice than women (18% vs 16%).

But according to the ILC, age, gender and other “socio-demographics” don’t matter much one “everything else” is taken into account.

- for example, financial capability trumps income, and age modifies gender effects

- marital status, age, housing status and employment status have no net effect (apart from the self-employed being more likely to take advice)

Correlation vs causation

As the ILC point out:

Assessing whether advice works poses significant methodological challenges.

Those who take advice may save more, accumulate greater financial and pension assets and have higher pension incomes irrespective of taking financial advice – perhaps because they are wealthier or more psychologically disposed to saving and investing in the first place or prepared to accept more risk.

To get around the problem, the ILC has used:

An advanced statistical technique called propensity score matching which identifies two similar groups of individuals within the data and then assesses the impact of advice on one group (the treatment group) versus the other (the control group) thereby mimicking a scientific experiment.

Later on, I will approach this problem from the opposite direction, by examining the mechanisms by which advisors might help investors.

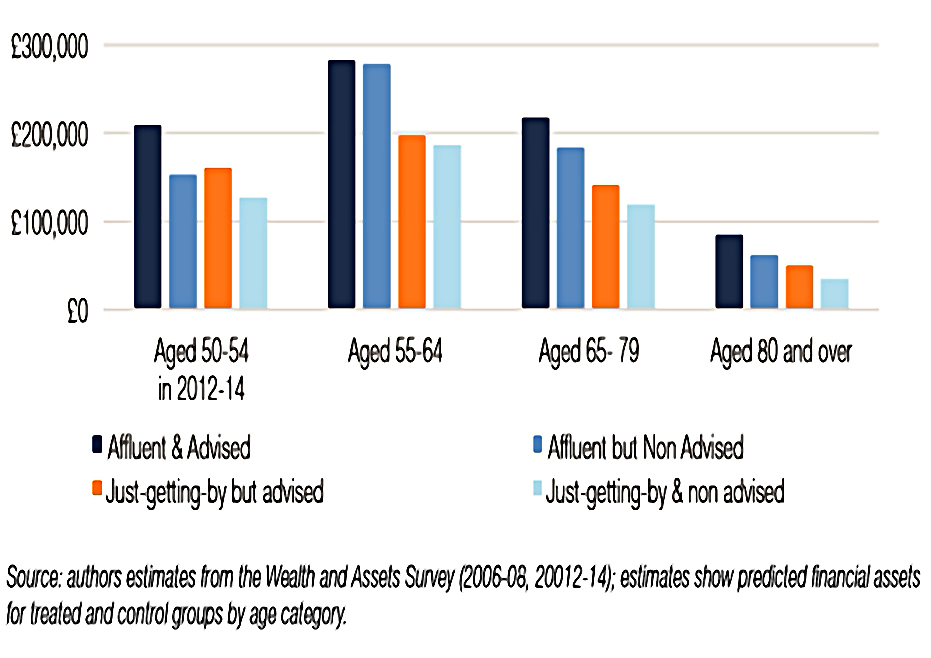

Two tribes

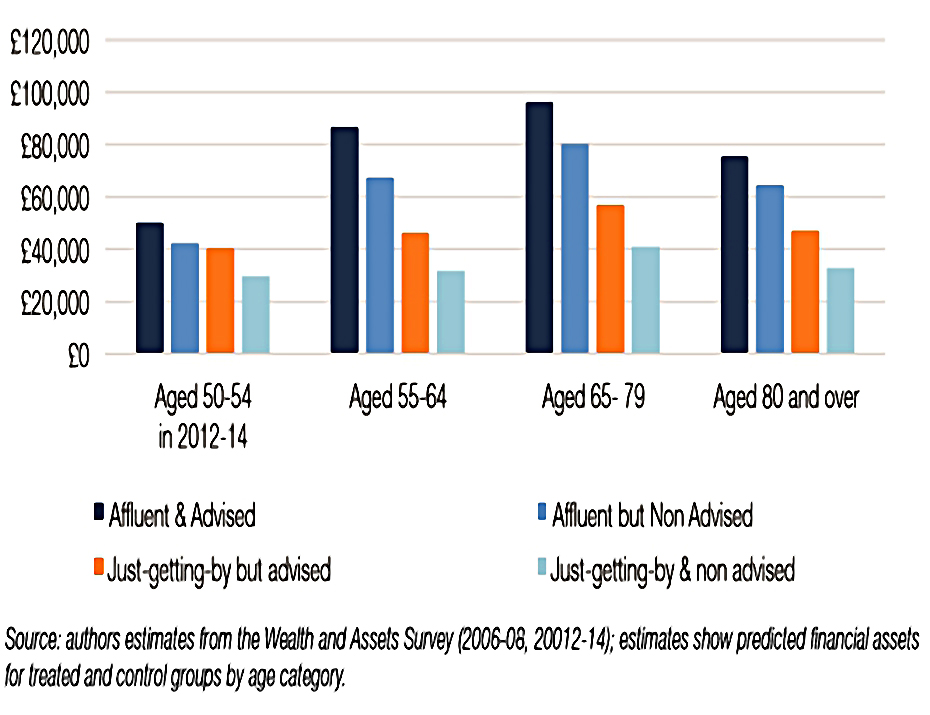

The ILC compared the effect of advice during 2001-07 on outcomes during 2012-14, using two groups:

- the “affluent”, and

- the “just getting by”

The affluent group includes those with a degree, couples, the self-employed, homeowners, those who saved in 2006-08 (and the wealthy).

- The just-getting-by group includes those without educational qualifications, the single, divorced or widowed, employees, renters (and the less wealthy).

These two groups have respectively a high or low a priori probability of receiving advice.

- They are then subdivided into those who did and did not receive advice, to form four groups who can be compared.

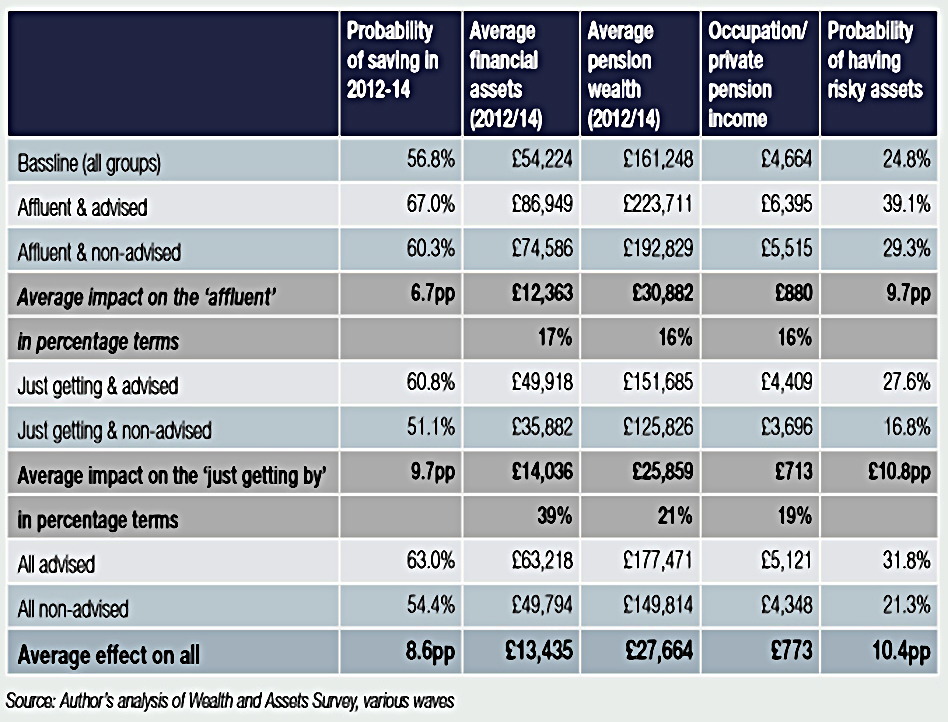

Here’s what the ILC found:

The “affluent but advised” group was 6.7% more likely to save and 9.7% more likely to invest in the equity market than the equivalent non-advised group.

The “just getting by group” was 9.7% more likely to save and 10.8% more likely to invest in the equity market than the equivalent non-advised group.

When looking at the results, the ILC separated “liquid financial assets” from “pension wealth”:

- the affluent advised had £13K (17%) more in liquid assets and £31K (16%) more in pension pots

- the getting by advised has £14K (39%) more in liquid assets and £26K (21%) more in pension pots

Economic behaviours

The ILC looked at six “economic behaviours”:

- The probability of saving any income (2012-14)

- The probability of owning equities

- The probability of retiring before age 65 (by wealth)

- The amount of financial (non-pension) wealth (2012-14)

- The amount of pension wealth (2012-14)

- Private pension income

Here are the results:

- Only 57% of people managed to save some income

- 25% hold equities

- Average financial wealth is £54K (median £16K)

- Average pension wealth is £161K (median £57K)

- Average pension income is £4.6K (median £720 pa).

Depressing stuff.

Why no advice?

The report finds that the two main reasons why people don’t take advice are:

- they don’t trust IFAs

- they have low levels of financial capability

Trust is certainly an issue, given the history in the UK of mis-selling by IFAs, which has led to investigations of the financial advice market by the FCA.

- The FCA is not convinced that advisors offer value for money, or place investors into the most suitable funds.

The ILC see opportunities for auto-enrolment, decumulation, robo advice and the pensions dashboard to be used as triggers to increase financial capability and the provision of advice.

- They don’t say how such advice would be funded.

I think that the main reason people don’t take advice is that it is too expensive to be cost-effective on the small pots that most people in the UK have.

- After a free initial meeting, the typical adviser will charge between several hundred and several thousand pounds.

- Ongoing advice will average £150 an hour with fees ranging between £75 and £350 an hour.

Which makes funding a key question.

The bigger picture

This ILC result is not new.

- A previous study by Vanguard found that financial advisers can boost investors’ returns by up to 3% pa.

- And Morningstar also carried out a similar study.

If we accept that those who receive advice prosper, why should that be?

Mechanisms

The traditional view of advisors was that they could provide “alpha” – beating the index.

- This could be achieved through superior market timing and / or superior stock selection.

So long as the alpha was bigger than the advisor’s fee, the investor would come out ahead.

The rise of low cost passive investing (index funds, then ETFs) has brought to investor’s attention the fact that most asset managers do not , in fact, provide alpha.

- They typically underperform their benchmarks in proportion to their fees.

And those managers who do out-perform are difficult to identify in advance.

- Investment is now a commoditised industry, though the industry itself is fighting hard to prevent its customers from noticing.

How, then, can an advisor add value to an individual client?

- In one sense they cannot, assuming constant behaviour from the client.

The benefits identified by the ILC appear when you compare two groups of people, some who saw an advisor, and some who did not.

- This is an education effect – the advisor is introducing his clients to techniques and products with which they are not familiar.

So the same results are likely to be achieved via free education, which is widely available these days.

The Vanguard study stressed the value of defining strategy and goals, the discipline to stick to a plan and tax planning.

- The biggest benefit came from keeping clients invested during volatility (a downturn).

- Other components of what they called “advisor’s alpha” included lowering costs, rebalancing and tax strategy.

Each of these measures can be achieved without an advisor.

Conclusions

I can’t claim to be familiar with the statistical methods used by the ILC to dig out these results.

- But I find it plausible that those who receive advice will profit from it.

The real question is whether they could achieve the same results without paying for advice.

The basic recipe for financial success is:

- work out where you are now

- work out where you want to get to

- investigate your risk tolerance

- work out how much you need to save at that risk level to reach your goal

- implement a diversified, low-cost, tax-efficient portfolio

- regularly review and rebalance

There are no secrets here, and each of these steps can be mastered by the average individual.

- Delegating some or all of this work to an advisor makes things easier, but more expensive.

Cost is the main barrier to most people taking advice, and if we want more people to get advice we need to make it cheaper.

- This in turn requires re-regulation, since that is what keeps the cost of advice high.

We need to make it clear that the point of regulated advice is that you can sue the advisor if things go wrong.

- If you are happy to do without that legal recourse, there should be cheaper options available.

We need to define a level of support (currently known as guidance, but poorly-described) that can be supplied by unregulated individuals at low cost.

- This would fall short of recommending specific products, and leave the investor free to choose the most suitable course of action after discussing a range of options.

Of course, industry-sponsored reports are unlikely ever to recommend this.

It is, of course, entirely plausible that advisors provide psychological support to investors, and encourage good habits that lead to long-term improvements in outcomes.

- But you don’t need an advisor for that – you need a coach, which can work out much cheaper.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.