Tim wrote that our first instinct is often wrong.

When we start to have second thoughts, the second thoughts are usually occurring for a reason. It is better to switch. So why don’t we?

Since Thinking Fast and Slow, most investors will be familiar with the idea that we shouldn’t act on impulse.

- The more interesting question is why so many people do.

Professor Justin Kruger (co-discoverer of the Dunning-Kruger effect) has found that people are good at remembering when we were right by stocking to our first instincts, but better at remembering when we were wrong to switch.

“Experience” tells us switching is a bad idea, but only because we misremember the lessons of previous switches.

Steven Levitt of Freakonomics fame persuaded people who were hesitating over a big life decision to be guided by a coin toss.

Those who had been nudged to act ended up being happier several months on than those who had been nudged to stick with the status quo.

If you are hesitating over whether to leave things as they are, you probably needed to make a change some time ago.

LTA

Merryn Somerset Webb has changed her mind about the Lifetime Allowance (LTA) for pensions, but I still think that it’s a bad thing.

- I don’t have a problem with the concept, or even the the amount – £1.055M will give you an annual income of £34K at a safe withdrawal rate of 3.25% pa.

I just think that’s it’s perverse to measure how much comes out of a pot (which depends on your skill as an investor) rather than how much you put in.

- I think that penalties for success are bad disincentives in general.

And I am also irritated by the 20 times conversion rate for DB pensions (even though I am a beneficiary of this) when 30 times would be much closer to the mark.

Merryn is still angry about the tapers system of annual allowances, and she has a point

Most people who earn over £150,000 will do so for only a couple of years in an entire career. They once saw those years as a magnificent opportunity to build up a retirement pot. No more.

Merryn wants the government to abolish the annual allowance, but I’d much rather that they did away with the LTA.

Inheritance

Jason Butler looked at why so many inheritances fail to help the people that they are intended to.

Evidence suggests that most of the time inherited wealth has been depleted by the second and third generations.

A successful wealth transfer means more than transferring money. It means also transferring your personal values, life lessons and ethics to the next generation.

But as Jason points out, talking about money is very difficult for most people.

Retirement abroad

Hannah Roberts (( The picture is from her Twitter profile )) looked at the tax and visa schemes designed to attract rich pensioners abroad.

We’ve looked at Portugal previously, so let’s start there.

- Portugal offers no tax on foreign income (which includes your pension) for 10 years.

Italy passed a plan in December 2018 that reduces the tax rate to 7% for foreigners who relocate to communities in six southern regions (including Puglia), plus Sicily and Sardinia.

- The snag is that you have to live in a town with a population of less than 20,000.

Dubai was the third location that Hannah mentioned.

- The country has no income tax and offers five-year retirement visas.

You need to own a property worth €480K or have savings of €240K or income of €60K.

Portugal still looks like the best option to me.

- It’s so good that Finland has moved to block its citizens from relocating there.

That sounds dodgy to me, but I wouldn’t put it past a Corbyn government.

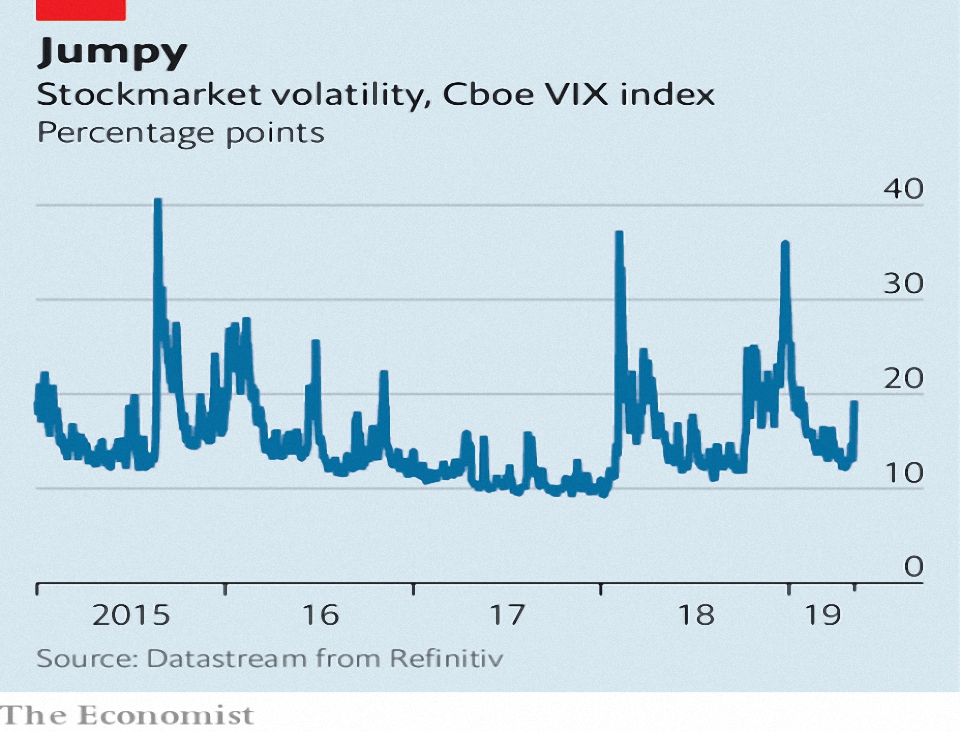

Volatility

In the Economist, Buttonwood looked at the effect of volatility on options prices.

- As you might expect, the jumpier that prices are, the more the right to buy or sell is worth.

The more volatile that prices are, the more likely they are to reach a price where a cheap option (out of the money) becomes a valuable one (in the money).

The Black-Scholes formula is the industry standard for valuation, and has three inputs:

- time

- distance to strike price, and

- volatility

It works the other way, too – options are used to calculate the levels of volatility implied by their prices.

- The famous VIX index is created this way.

The BS formula has flaws (many of which were pointed out by Fischer Black himself).

- A key one is that volatility is assumed to be fixed, whereas in reality, future volatility is unknown.

So you should buy or sell options according to which way you expect volatility to move.

- Or you can hedge your stocks with an ETF that tracks the VIX, and is therefore long volatility (which is unusually bad for stock prices).

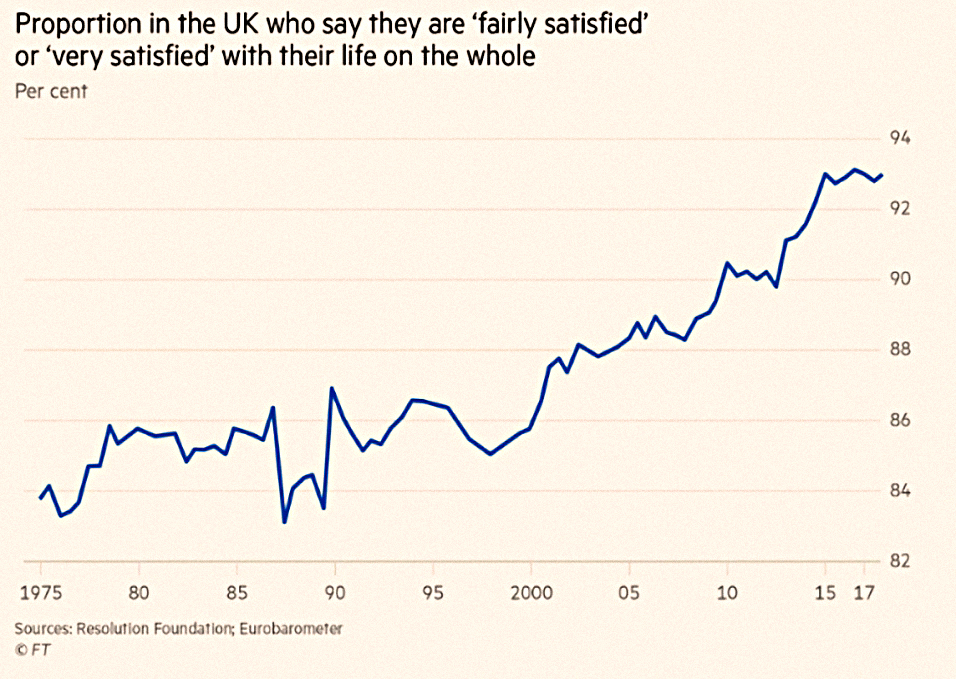

Life is good

Let’s end on a high note.

- Simon Kuper noted that despite all the doom and gloom in the media, more people than ever are satisfied with their lives in the UK.

Close to 93% of Britons are “fairly” or “very” satisfied.

- This undermines the “Brexit is a cry of pain” argument.

Remain-supporting London, often derided as a blissful elite bubble, has the lowest self-reported well-being of any region, says Resolution.

Meanwhile, retired homeowners aged about 70 — overwhelmingly pro-Brexit — are the UK’s most satisfied citizens.

For this particular group, the Leave vote was less a cry of pain than a vote of confidence by very contented people in the country’s ability to go it alone.

Simon notes that unemployment is the biggest preventative of satisfaction, and workforce participation stands at 76%, the highest on record.

- Although many jobs are unfulfilling, this is not a new phenomenon, and workers in the gig economy seem to be happy.

The male suicide rate is also at the lowest level on record, and violent crime has reduced since the 1990s.

- Good news indeed.

Quick links

I have seven for you this week:

- The Chief Investment Officer blog reports that Cliff Asness has no simple answer to his quant strategy losses.

- Flirting with Models has a Country Rotation Strategy based around Growth / Value sentiment.

- The FT reported that PurpleBricks is on shaky foundations.

- And that Uber has a long ride ahead to profitability.

- The Economist had a special report on how phones are shaking up banking.

- UK Value Investor asked whether Reckitt Benckiser is now good value.

- And also sold Compass Group after recent price gains.

Until next time.

Mike,

A plausible explanation for why the LTA is based on current value rather than contributions is given at https://firevlondon.com/2018/04/08/how-many-isa-millionaires-are-there/ See in particular the exchange between Jon & John in the comments to the post.

Hi Al,

Thanks for the link. It’s certainly plausible that HMRC haven’t kept records of pension contributions (though they do go on personal and company tax returns, unlike ISA contributions).

But that doesn’t justify an output cap. The point is that it penalises success – good investors pay more tax. It’s like saying no team is allowed to score more than three goals in a football match.

Mike

From my own experience, it seems pretty clear that any record of contributions is lost on transfer of a DC/SIPP between products/vendors/platforms. With respect to any HMRC records I just do not know.

I understand all your points about applying the cap to the output.

If, however, as the link hints, the inputs are unknown then it would be rather impractical to implement a cap based on those inputs.

The football analogy is rather timely given that Manchester City is now effectively facing such a ban!