Weekly Roundup, 25th April 2017

We begin today’s Weekly Roundup in the FT, with the Chart That Tells A Story. This week it was about Gold.

Contents

Gold price

Lucy Warwick-Ching looked at the gold price, which is up 11% in 2017 (in dollar terms).

- Lucy puts this down to increased global geopolitical tensions, which seems as likely an explanation as any.

- North Korea is the current flashpoint, though it looks to me that the US and China will sort something out.

The prospect of a Le Pen victory in France may also have contributed, though this seems unlikely after the voting in Sunday’s first round.

- And there has also been a spot of dollar weakness in recent weeks.

I can rarely see the point of these articles looking at price changes over a few months, but the mainstream media seems obsessed with this week, last week and next week.

As someone very clever once said:

The single greatest edge an investor can have is a long-term orientation.

Is £70K pa rich?

Lucy’s second article of the week was about whether £70K pa makes you rich.

The eagle-eyed amongst you will have noticed that a General Election has been called for June 8th.

- My plan is to keep my powder dry on this until something interesting happens.

The nearest we came to this was Labour’s John McDonnell suggesting that a fair tax system would make those on over £70K pa (“the rich”) pay more.

So does £70K pa make you rich?

- In one sense, yes – only 0.1% of the world’s population has this income.

- And even in the UK, only 5.2% of people earn £70K.

But as we know, these things are relative rather than absolute.

- It’s what you can do with the money that counts.

Everyone will have their own definition of what constitutes rich – usually based around having a bit more than you do personally, so let’s approach the problem from the opposite direction.

I would argue that you can’t be rich if you still need to work for a living.

- Financial independence (FI) – or the prospect of it in the future – is the minimum target.

Depending on where you live in the UK, you’ll need to put together something in the order of £850K to £1.5M to get there.

- Note that whilst the dysfunctional property market in the UK inflates that target somewhat, even here in central London it only represents 50% of the pot. (( The rest is the £750K needed to safely withdraw £25K each year to live on ))

Assuming five years to save a house deposit, and 25 years to pay it off, most people would want to accumulate this over 30 years.

- Others will be more patient, and be happy to take 40 years.

On the current tax system, someone on £70K will pay:

- 0% on the first £11.5K = £0

- 32% (income tax and NICs) on the next £31.5K = £10K

- 42% on the remaining £25K = £10.5K

So their tax bill is £20.5K, a marginal rate of 29.3%.

- That doesn’t sound too bad.

If they can manage to live on £30K whilst working, they might save close to £20K a year (including house repayments).

The bad news is that saving £20K a year for 30 years, with returns at 2% above inflation (( To me, a reasonable estimate of future UK returns from here )) would only produce a pot of £822K.

- So if you live in Scotland of the far north of England and earn £70K, you might be FI in 30 years.

If we increase the return to a more aggressive 4% above inflation, we still only get to £1.16M.

- You can afford to live in the South now, but not in a property hot-spot.

Those prepared to work for 40 years at £70K (assuming they can find this work for so long) do a bit better:

- £20K pa at 2% above inflation for 40 years provides £1.23M

- £20K pa at 4% above inflation for 40 years provides £1.98M

So although many readers will disagree, I would argue that £70K pa – at least near London, where many high-paying jobs are located – does not really make you rich.

£40 a week is enough?

In the Guardian, Patrick Collinson covered a report from consumer group Which? suggesting that 40-year-olds with no savings could get away with putting aside just £40 a week (£2K pa).

Which? had surveyed 2,700 of its retired and semi-retired members and calculated their spending levels:

- £18K pa (per couple) on essentials (food, heat, transport)

- £26K pa including extras like holidays

- £39K pa for a “luxury” retirement (long-haul holidays, golf clubs and new cars)

A separate survey by Tilney came up with £26.5K as the average.

The underlying maths assumed two full State pensions (£16K pa).

- £40 a week each would then build up a pot of £210K by age 67

- this would then provide £10K a year for the rest of their lives.

That’s a 4.8% withdrawal rate, which is far from safe.

- So I assume they must be eating into the capital as well.

If you assume that you will spend less after age 75 (as most do) then you need even less to bridge the gap.

It makes for a neat headline, and I suppose the plan does provide genuine comfort to those who have saved nothing by age 40.

- But retiring at age 67 and immediately eating into your capital is not a great result.

Equities

Terry Smith wrote about the compounding effect in equities.

- Because companies retain some (usually around half) of their earnings for reinvestment in the business, their value compounds in a way that bonds and property do not.

Of course, as an investor you can manually create this compounding by reinvesting your income from bonds and property, but equities do half of the work for you.

Terry also points out that because companies trade at more than book value (three times book for the S&P 500, for example) each reinvested pound or dollar can create £3 or $3 of market value.

- This is an advantage over the manual compounding of an investor using their dividends to buy more shares.

- Apart from the purchase costs, the new shares must be bought at market value (three times book).

So the reinvestment of earnings within companies provides more growth in value than dividend re-investment.

- This explains why Buffett prefers to reinvest Berkshire Hathaway’s earnings himself, rather than pay a dividend.

We’re previously argued that Dividends Don’t Matter, except perhaps to those in decumulation (and even then you can always sell shares to generate an income).

- Investors who are still looking for growth should be keen on companies reinvesting their earnings and a high rate of return.

Terry therefore prefers companies with high return on capital, though he accepts the risk of mean reversion, where new market entrants are attracted by the high returns and compete them away.

- Where rates of return are in decline, you might want to get your money back.

- Companies that avoid this fate have the “moat” that Buffett looks for.

Value stocks and reflation

John Authers looked at value stocks, and whether the current doubts about the global reflation trade are overdone.

He pointed out that we are approaching the anniversary of peak deflation fears.

- In fact the switch to reflation didn’t happen until July – after the Brexit “low point” – but that’s fairly close.

When it became clear Brexit hadn’t triggered anything serious, people felt able to breathe out.

- Then China started to grow and Trump won.

But in 2017 there has been a gradual move back to “reflation off”.

- The oil price has been weak and there have been no surprises to the upside from economic data.

The Fed had planned three rate rises, in 2017, but since the data weakened, they don’t seem so sure.

- The markets now imply a 40% chance of three rises.

There are two routes back to “reflation on”:

- the oil price breaking up above $50 a barrel

- a funded Trump tax cut being passed by Congress, without too much trade protectionism

So John recommends a focus on value stocks (since bonds are even more expensive than stocks).

- Paradoxically, value stocks do well when growth is high.

- When growth is low, investors pay up for the companies with the strongest growth.

So buy cheap assets and hope for “reflation on” to return.

Too few stocks

Over in the Economist, Schumpeter looked at the decline in the number of US listed firms.

- There were 7,322 in 1996 but today there are only 3,671

- despite this, the stock market is now worth 136% of GDP, compared with 105% in 1996

So now fewer older and bigger firms make up the market.

- The average lifespan of a listed firm is up from 12 years to 18 years.

- But the number of IPOs is down from 300 a year to 100 a year.

- Successful firms like Airbnb, Pinterest, Uber and Lyft are all still private.

In a new paper, Michael Mauboussin of Credit Suisse finds six reasons:

- Red tape and disclosure rules dissuade firms from listing

- Short-termism in listed markets frustrates founders (though Jeff Bezos and Elon Musk seem to cope)

- There is less need for capital in tech firms

- There is better private market supply of capital, including directly from asset managers like Fidelity

- Employee shares can be sold to private investors (no need to list for staff to benefit from increased valuations)

- There are lots of takeovers on the listed markets (lax anti-trust enforcement)

The newspaper sees the decline in the number of listed firms as a symptom of oligopoly, which will harm the economy in the long term.

Comparative advantage

The newspaper also looked at the award of the Clark medal to trade economist Dave Donaldson for his work on comparative advantage.

- He took 10 years to write one of his most famous papers, on the impact of railways on the Indian economy from 1853 to 1930.

- A town connected to the railway typically saw a 16% increase in real local income in one year.

- This compared to a 22% increase for the whole country between 1870 and 1930.

Comparative advantage comes from David Ricardo in a book published in 1817 (two hundred years ago last week).

- The basic point is that trade is not zero-sum and both parties gain.

- Each community can focus on the thing it does best (or least worst) and trade with others who do different things better.

- Ricardo used a simple model of trading English cloth for Portuguese wine.

Donaldson demonstrated that the integration of US agriculture via comparative advantage between 1880 and 1997 added as much to output as did productivity gains.

- This is despite the erosion of flexible labour markets and the replacement of trade in finished goods by trade in components.

Corporate bond markets

The Economist also had two articles (1 and 2) about the archaic corporate bond markets.

- These are big markets compared to the stock markets, but under-reported.

- In 2016, US equity issuance was $200 bn – for corporate bonds it was $1.5 trn.

The corporate bond market has also been growing in recent years.

- Low interest rates explain why issuers would like to grab a piece, but not why there is so much investor appetite.

The focus of the articles is how behind the times bond markets are:

- Price data is difficult to find, phone deals are common, and settlement is slow.

A lot of this stems from a lack of fungibility – each bond issue is unique.

- Liquidity is provided by dealers (historically banks) holding inventory until a buyer shows up.

But capital regulations introduced since the 2008 crisis have made this expensive for banks.

- As QE-inspired buying from central banks comes to an end, this may cause problems.

So “all-to-all” trading (between institutional investors) needs to be introduced.

- Tradeweb has just announced this service for European bonds (MarketAxess has provided a similar services for US bonds since 2012).

- And from 2018, MIFID 2 will require prices and volumes of trades to be recorded properly.

The newspaper can even foresee the algorithmic trading of bonds.

Quickies

- Taxpayers have finally turned a profit on the money that they put into the Lloyds bailout in 2008

- though they remain a long way from this when it comes to RBS

- Good news: the general election means that the probate fee hike has been put on hold for now.

- Hedge funds are betting against Hargreaves Lansdown

- They are worried about the threat from robo advisors, though my personal research into these products (summarised here) has been disappointing – they remain unsophisticated and / or not cheap enough.

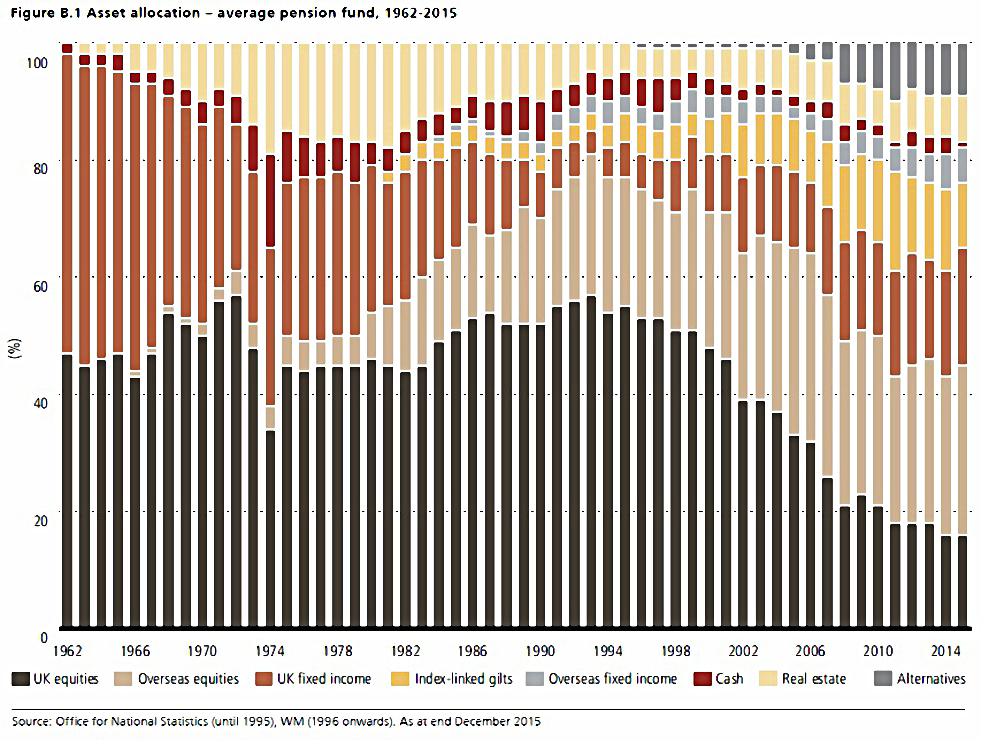

And finally, here’s a nice chart from Pensions Expert showing the changes in asset allocations within UK pension funds over the past 50 years:

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.

Hi Mike, thanks for the round up.

I want to mildly argue about the £70k rich thing (sorry!).

First of all, and I know this is nothing to do with you, “rich” surely relates to wealth, not income, although I can see that there’s some crossover, and from a political and taxation point of view income is easier to work with and talk about.

Second, I’d have to disagree with your £70k retirement calculations though. If the £20k savings goes into a SIPP then it goes in gross rather than net of tax, which I guess would massively improve the final retirement pot.

Third, even if the final tally was £800k then as far as I can see that’s a huge retirement pot. My parents had not even a quarter of that amount and live an entirely reasonable lifestyle, probably better than most pensioners. Their house is bought and paid for so overheads are very small, and are easily covered by their annuity payments and the state pension. So I, along with most people (I expect), would consider an £800k retirement pot “rich”.

Also, from an income point of view, having earned a variety of incomes in the last decade or so from £20k to £90k, I would definitely class £70k as rich. Unless you live in a mansion or somewhere daft like central London, £70k gives you huge discretionary spending power, at least relative to 90% of “normal” non-rich people.

Anyway, sorry for being negative, devils-advocate and all that!

John

Hi John,

Devil’s advocates are always welcome. I agree with you that rich = wealth (at least in so far as you need the wealth to provide an income to live on).

I think the point about tax is debatable. First, up to half of the savings are being used to buy a house, with no tax relief available.

Second, though I personally would use a SIPP and end up with more money, there have been so many changes to the pensions system over the past 12 years that a lot of younger people prefer not to lock their money away for decades. They will use ISAs instead, with no tax relief.

£800K is not a huge retirement pot. At say 3.3% pa withdrawal rate (safe for the UK), it produces an income of £26.4K. That’s not rich.

Income is trickier. Whether £70K pa provides a good lifestyle depends on your lifestyle choices. After tax and savings you are really living on about £30K pa. That’s enough for me these days, but I doubt that I would have been too happy between the ages of 25 and 40.

People will always disagree about what words like “rich” and “equal” and “fair” mean. The real problem with Labour’s policy is that discouraging people on £70K and up isn’t good for the country.

Mike