Weekly Roundup, 27th June 2022

We begin today’s Weekly Roundup with VCTs.

VCTs

I mentioned last week that Foresight had taken over the Downing VCTs, or at least the technology ones (Downing seems to be hanging on to their healthcare VCT).

- In FT Adviser, Sally Hickey reported that quite a few of the original players are selling out.

Ben Yearsley of Fairview Investing said:

A lot of the original players have all got out, they are all selling out and cashing in. It is turning into a much narrower market where scale is vitally important. Many have been doing it for 20 years or so, and with assets at an all-time high and good performance, it is an ideal time.

I wouldn’t quite go that far, but we did see Northern sell its VCTs to Mercia in 2019, and last year, Gresham House bought the Mobeus VCTs.

- I use eighteen VCT providers (plus one EIS firM) and as long as the market doesn’t shrink by 50%, I should be fine.

Pensions

The Chancellor confirmed that the Triple Lock on the State Pension will be restored for 2022.

- This means that an increase in the area of 10% is likely.

Naturally, lots of people are unhappy with this, since their wages won’t be going up by as much.

- There is a difference, however – pension income is part of the cost of delivery of goods or services.

So, unlike higher wages, higher pensions need not directly feed higher inflation.

- Of course, all spending contributes to inflation in some sense – more money chasing the same amount of goods and services means higher prices.

In this sense, even the energy bill rebates are inflationary, as people will have more money to spend elsewhere.

I find the whole discussion around prices and incomes quite depressing.

- We seem to be a very jealous society with a focus on exceptionalism (see also the windfall tax on energy firms).

When you set rules around an uncertain outcome, you can’t change them when you don’t like the outcome.

It also remains the case that the US State Pension is one of the meanest in the OECD (relative to earnings).

In the FT, Josephine Cumbo reported that the recent rise in the state pension age (to 66) has doubled pensioner poverty rates.

- The change led to around 700K 65-year-olds waiting for another year.

This does save the government money:

The subsequent reduction in the benefits bill – and increase in tax revenues from 9 per cent of 65-year-olds staying in work longer – led to a £4.9bn annual boost to the Treasury coffers.

But at the cost of more poverty:

Absolute income poverty levels, after housing costs, for 65-year-olds rose by 14 percentage points, or nearly 100,000 people, to reach 24 per cent by late 2020.

The state pension makes up just over half of income for middle-income pensioners, and more than 80 per cent of income for the poorest fifth of pensioners. The increase in the SPA pushed down the net income of 65-year-olds by an average of £108 per week.

Former pensions minister Ros Altman said:

The scale of increased poverty caused by the rise in state pension starting age is further evidence that the blunt cost-saving tool of increasing state pension age is creating increased social injustice.

Josephine also reported on calls from the Association of British Insurers to allow early access to pension pots in the event of financial hardship.

- The request was in a paper which also recommended that auto-enrolment contributions should increase from 8% pa to 12% (something that I support).

I can’t see early access ending well – we already have tiny private pensions in the UK, and letting people take money out before age 55 is only likely to make them smaller.

Helen Morrisey from HL agrees:

Tempting as it is to talk about allowing early access to pensions during times of financial crisis it only kicks the can down the road as people won’t be able to retire when they need to because they’ve raided their pensions. This could mean more people are forced to work for longer when they may be in ill health.

CDC pensions

In the FT, John Ralfe wrote against a move to collective defined contribution (CDC) pensions.

- CDCs are a middle ground between DB and DC schemes – contributions are defined but pooled, and the scheme declares a target payout rate, which varies in line with the scheme’s assets.

UK pensions minister Guy Opperman appears to be a fan:

CDC could transform the UK pensions landscape and deliver better retirement

outcomes for millions of pension savers.

There is a consultation at the moment on how to operate multi-employer CDCs.

The only existing scheme is from Royal Mail (RM), covering 140K staff.

- Joint contributions total 15.2% of salary and the target payout is 1/80th of salary per year, starting at age 67 and increasing at inflation plus 1%.

The payout beats that of the average DC scheme, but that’s because of the asset allocation.

- The RM scheme will be 100% in stocks, which sounds risky.

And if a regular DC saver wanted this allocation, they could choose it for themselves.

The theory is that CDC benefits from “intergenerational risk sharing”, but it’s hard to see how all generations can come out ahead.

- In an individual DC account, if the pot shrinks by 20%, so does the forecast pension.

In the CDC, all of the forecast pensions also shrink by 20%, even though the retirement dates of the members might vary from 30 years in the future to 20 years in the past.

Individual DC has the killer advantage that each saver can choose their own asset allocation, to suit their personal risk preferences, which probably changes as they get older. But CDC asset allocation is identical for all members, regardless of age or risk preference, so will be “suboptimal” for virtually all of them.

I can’t see the attraction of CDC myself.

Mortgage stress test

The Bank of England has decided to withdraw its mortgage affordability stress test, just as it might become useful (because interest rates are rising).

The Financial Policy Committee (FPC) introduced two tests back in 2014:

- An affordability test that checks whether borrowers could afford a 3% pa increase in their mortgage rate during the first five years of the loan.

- A limit on how many mortgages a lender can issue at a loan to income rate (LTI) of more than 4.5 times.

This second test will remain.

The FPC said:

[The LTI flow limit] will deliver the appropriate level of resilience to the UK financial system, but in a simpler, more predictable and more proportionate way. The additional insurance provided by the affordability test is small. A framework without the affordability test recommendation would therefore be simpler and more predictable.

This may all be true, but the timing of the announcement – in the teeth of a cost of living crisis with high inflation and rising borrowing rates, plus soaring property prices – is strange.

Care costs

In FT Adviser, Jane Matthews said that retirees could lose 56% of their home’s value to pay for care costs.

- In 12 out of 20 UK cities analysed, average care costs were more than half of average house prices.

Care home residents typically spend at least four years in care homes, costing individuals on average £113,000.00 – £161,000.00 depending on where they live in the UK.

There is a means test, but:

Individuals have to self-fund 100 per cent of their care home fees if their total capital is worth more than £23,250. More than a third (36.7 per cent) of people use the value of their home to pay for care.

I think the article greatly understates the risk – my mother-in-law’s care costs are well over double what the research found to be the average cost for London.

Frozen allowances

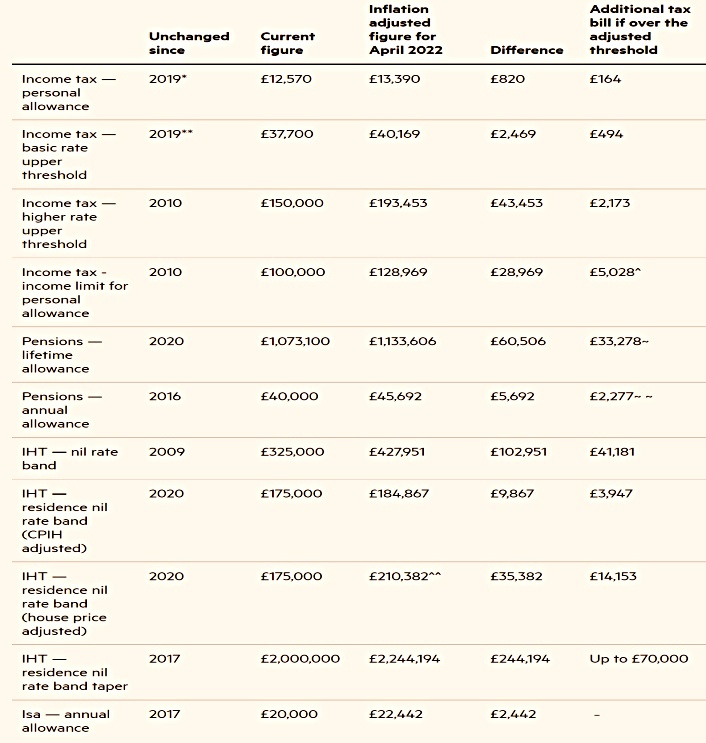

In the FT, James Hambro financial planner Charles Calkin looked at frozen tax allowances.

- Most of the core allowances have been frozen for several years, and many will remain frozen until 2026.

The worst is inheritance tax (IHT). The nil-rate band threshold has been frozen at £325,000 since 2009-10. Had it risen in line with inflation it would be £427,951 now — a difference of £102,951.

The residence nil-rate IHT band has been frozen at £175,000 since 2020-21. Adjusted in line with inflation, it would be £184,867 now. For a couple, the impact of these freezes could be £90,255 extra in IHT.

We should also remember the residence nil-rate band taper, which reduces the allowance by £1 for every £2 an estate is worth over £2mn. Had that risen in line with inflation it would be £2,244,194 today.

The LTA is also frozen, at £1.073M.

- This should be at £1.134 if you start from 2020-21, but 10 years ago it was £1.8M, and should arguably be £2M by now (or even better, abolished entirely).

This adds up to between £15K and £230K more in tax.

Accumulating wealth is hard work. It should not become a burden to us once we have succeeded, causing us to fret anxiously about its preservation.

The Treasury’s IHT take increased by more than 10% to £1.1 bn in the year to May.

- The average bill is now £266K, up 27% over three years.

Quick Links

I have ten for you this week, the first six from The Economist:

- The Economist said that people’s inflation expectations will be hard to bring down

- And that energy security gives nuclear power a new appeal

- And asked whether the eurozone’s doom loop is still to be feared

- And explained how fighting inflation could imperil the eurozone

- And why everyone wants Arm

- And how El Salvador’s government is gambling on bitcoin.

- Alpha Architect looked at using machine learning to identify outperforming active equity funds

- And using institutional investor trading data in factors.

- A Wealth of Common Sense gave the case for owning bonds

- And UK Dividend stocks asked whether you should buy Rio Tinto for its 17% yield.

We’ve run out of space for more on the Fed’s interest rate hike, so I’ll try to come back to that next week.

- Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.