Weekly Roundup, 24th November 2015

We begin today’s Weekly Roundup in the FT, with the chart that tells a story.

Contents

Inflation

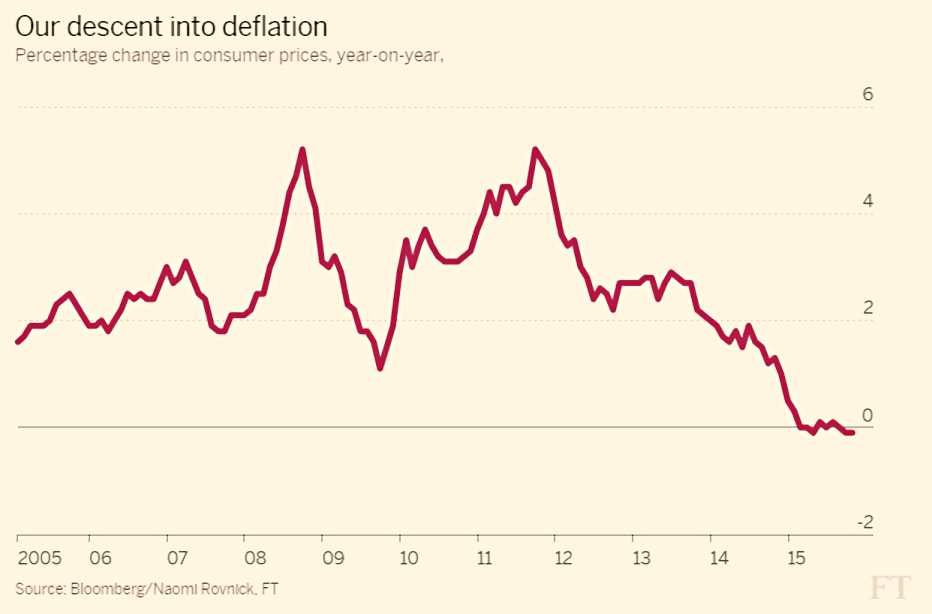

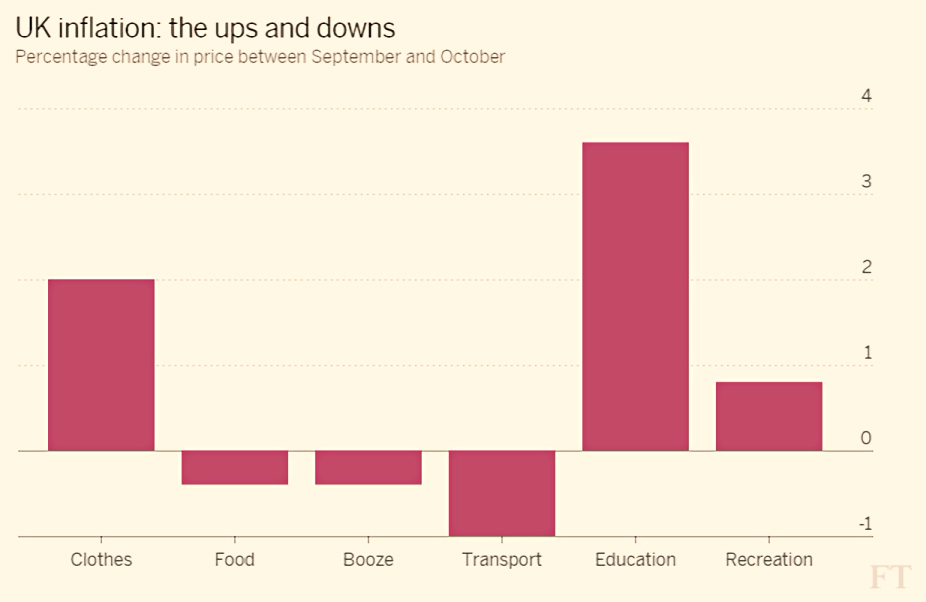

This week we got three charts for the price of one, as Naomi Rovnick took a look at UK inflation or rather, deflation. Consumer goods prices fell by 0.1% in October, the same as in September.

Naomi puts this down to the slowing increase in university tuition fees, plus a fall in the price of food and wine. Clothing and footwear went up largely as a result of fewer items in sales.

Deflation makes a rise in interest rates unlikely, as we are a long way from the BoE’s 2% target.

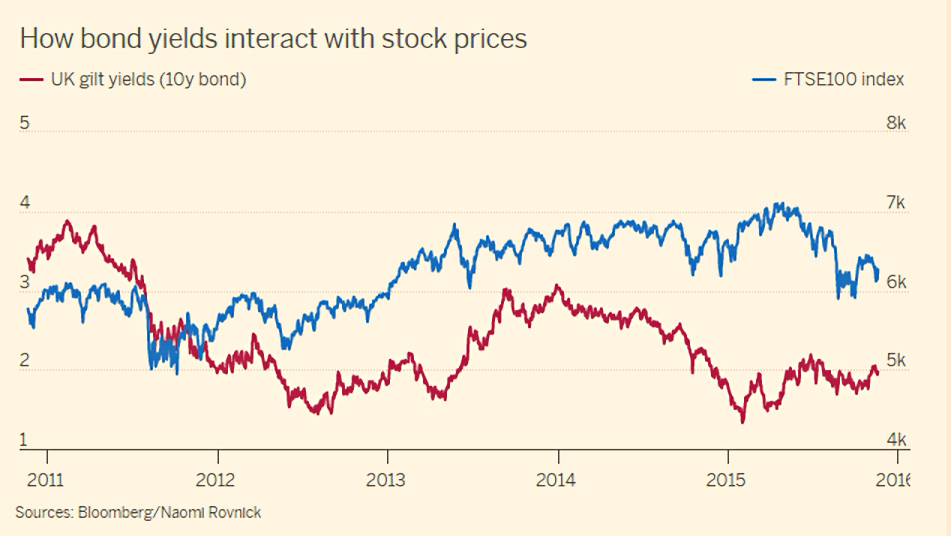

Low inflation and low-interest rates have been good for stocks and property prices, but hold bond yields down. This in turn increases pension deficits at companies with final salary schemes.

Fund costs

Daniel Godfrey, the former CEO of the Investment Association who was forced to resign when the members of the industry lobby group rejected his push for transparency, had an article in the FT on fund costs.

He thinks that they are designed to confuse investors. He begins with the annual management charge (AMC). A 1% charge doesn’t mean that for each £1K you invest, you pay £10.

Instead, 1/220th of 1% of the value of the fund is deducted each day. So your actual cost depends on the fund performance and cannot be known in advance. Nor can the dealing costs (commissions and spreads, driven by portfolio turnover) of the fund.

Additional costs like custody, registration and research vary between funds. They are sometimes included in the AMC but in other cases a separate “administration charge” is added.

Daniel thinks that the AMC should include all costs except the dealing costs, which he describes as “the cost of getting the job done … you’d incur them if you did the job yourself”.

He would also make funds account for the actual costs of the past year (including dealing costs, and in pounds per unit of the fund) as well as providing an estimate of the costs for the forthcoming year.

These two changes would allow investors to make informed choices between funds.

Five years of Fundsmith

Terry Smith wrote about what he had learned during the first five years of Fundsmith:

- He’s not a fan of macro-economics. He thinks that there are no reliable forecasters, and that the link to asset prices is tenuous.

- He prefers simply to invest in good companies. Companies that have “good products or services, strong market share, good profitability, cash flow and product development”.

- Poor and average companies tend to destroy rather than create value for shareholders, so buy and hold doesn’t work. The alternative is active trading, which not many people are good at.

- He’s not very interested in whether companies are “cheap”, either. Over the long run, he thinks that the quality of the companies will dominate the performance of your portfolio, rather than whether the shares were cheap when you bought them.

- I’m not quite convinced by this. There’s a lot of data to show that stock returns are strongly linked to the price that you initially pay. Value investing works.

- I suspect that for someone as skilled as Terry or Warren Buffett, the ability to successfully run a concentrated portfolio outweighs the buying price, but for most of us, it’s better to play the percentages and buy value.

- He also thinks that you have to “stick to your guns and ignore popular opinion”, citing the Tesco collapse as one example of a popular stock he stayed away from, and Microsoft as an example of an unpopular stock that is one of his largest holdings.

- Terry thinks that few people now bother to read company accounts, relying instead on management presentations using “adjusted” numbers that almost always remove negative items.

- The best performing share in Fundsmith’s first five years was Domino’s Pizza Inc, up 600%. Terry thinks that “the best investments are often the most obvious”.

- He’s a big believer in high return on capital as a measure, and franchisers score well here, as most of the capital comes from the franchisees.

- As an ex-private equity-owned firm, Domino’s also was highly leveraged.

- His advice is to run your winners and cut your losses. “Gardeners nurture flowers and pull up weeds, not the other way around”.

Emerging markets

John Authers thought that he could see the bottom for emerging markets. He thinks that the EMs are a good bet on a 5 to 10 year view, but there could be one more downwave to come.

They have been lagging the developed world markets for the past five years, and their currencies have been devalued.

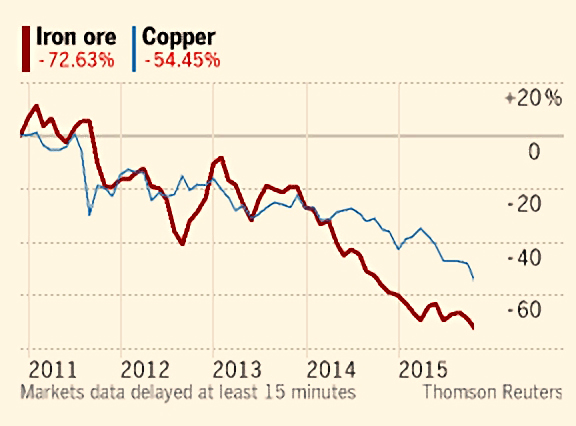

EM economies are dominated by industrial commodities – they both produce and consume them. Prices in these markets may not have much further to go down.

Iron ore in China is down 76% from a 2011 peak. The Baltic Dry index of shipping costs is down 95.5% from a 2008 peak.

The potential US interest rate rise in December could be the catalyst for a recovery, by flushing the last of the spare global capital back from the EMs to the US.

That could be the absolute bottom, and may involve some form of EM devaluation and default crisis.

Taxes

In advance of the Autumn Statement, Tim Harford wrote about an economist’s view of taxes. He began by describing the “three pillars of tax wisdom”:

- Tax things that have unpleasant spillover effects on bystanders – “externalities”

- The classic example is activities that produce pollution.

- We have a high tax on petrol, but a low one on domestic fuel.

- Tax things that are not price sensitive, or else all you will do is kill demand (and not collect any tax)

- This rule is harder to follow – taxes on things like rice or bread are difficult to sell politically.

- Optimal income taxation requires flat or even falling marginal tax rates

- This counter-intuitive result stems from the difference between an individual’s marginal rate of tax and his average rate of tax.

- Here in the UK, someone on salary of £25K has a marginal rate of 20% (more if you include national insurance) but an average rate of less than 15% because the first £10K is tax-free.

- High marginal rates on high incomes are a real discouragement for the rich to earn more money.

- But high marginal rates on low incomes will raise lots of money from lots of people, without discouraging any work.

Don’t expect to hear of any change like this in the Chancellor’s statement this week.

Next Tim looked at modern research on toll booths.

- When tolls were converted cash collections (coins) to electronic collection, drivers forgot about the cost, and toll collectors were able to raising the toll.

Compare this to research on tax credits in the US.

- These appear to encourage work in areas where the potential recipients are well-informed about them (not that surprising).

So the toll was a tax that worked best (raised most) when hidden, while the benefit payment worked best when widely advertised.

This new data driven research is thus producing answers that are more palatable to politicians.

Low yields

The Economist looked at investing in a world of low yields. The focus of the article was the assumptions being made by the final salary pension schemes in the public sector of America, and by college endowments.

When these schemes make their annual payments, they make an assumption about future returns in order to calculate how large the payment should be. Higher returns in the future mean lower payments today.

Endowments have to estimate their future returns to work out how much they can spend each year.

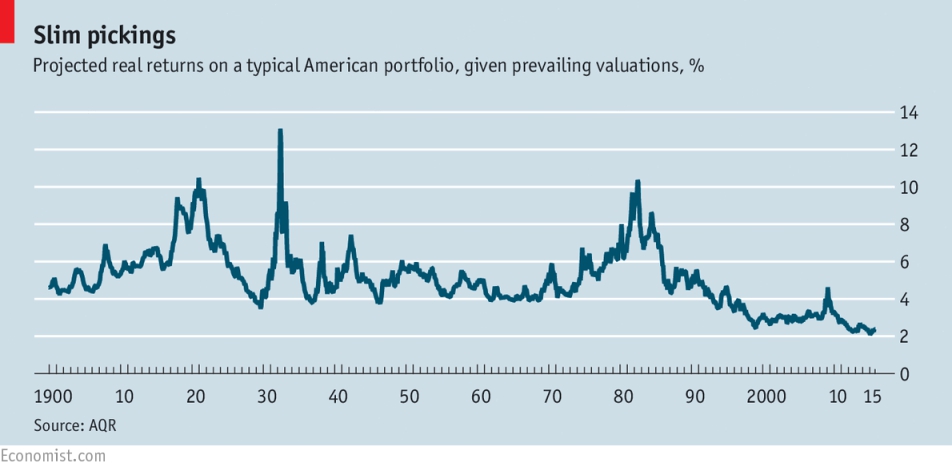

- The average pension fund is currently assuming nominal returns of 7.7% pa. Median returns have been 9.5% pa over 5 years, and 8.5% pa over 25 years.

- Endowments target a return of 7.4%. Actual returns over the 10 years to 2014 have been 7.1%.

- But 25 years ago, 8% yields could be locked in on long-dated Treasury bonds. These now return 2.3%.

- The yield on the S&P 500 in 1990 was 3.7% but now it is 2.1%.

And the low current yields reflect the high prices that result from the capital gains that have already been banked.

For high future returns, investors need even higher prices (valuations) or more corporate profits. Profits are close to a post-war high as a share of GDP.

Elroy Dimson thinks likely future long-term real return on a balanced portfolio (equities and bonds) will be 2% to 2.5%. AQR came up with 2.4%, by assuming 1.5% pa growth in dividends and profits for a 60/40 portfolio.

The current projected return is lower than at any time in the past 100 years. Assuming inflation of 2% pa, nominal returns would be 4% to 4.5%. much less than the pension funds and endowments are assuming.

And the pension funds are on average only 74% funded right now. So contributions – already 18.6% of payroll – need to go up. Either the employer or the employee (or both) needs to pay more, or the benefits need to be reduced.

Endowments will need to cut their spending by perhaps two-thirds if they don’t want to eat into their capital. Luckily, colleges also have access to tuition fees and gifts from donors and alumni.

The pension funds seem to think that alternative assets (property, private equity and hedge funds) might help. Their share of US pension portfolios rose from 16% in 2004 to 29% in 2014.

Returns on private equity in particular have been good, but the industry is too small (by more than a factor of 10) to be the engine of growth for all pensions.

Alternative assets my reduce risk, but they will probably not boost returns overall.

The problem with such long-term problems is that they do not need to be fixed right away. So it is tempting for administrators to leave the problem to their successors.

Which will make it into an even bigger problem in the future.

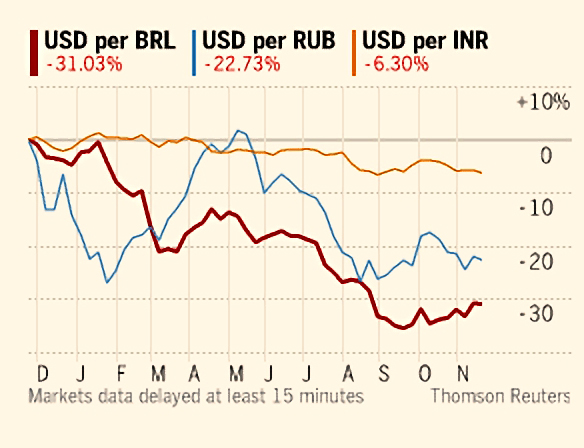

Currency volatility

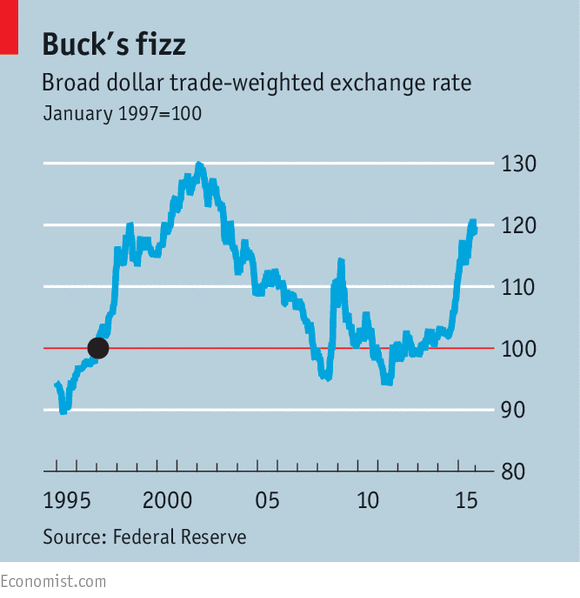

Buttonwood looked at whether the looming divergence in monetary policy could lead to currency volatility.

Next month the US will probably increase its interest rate, while the ECB either cuts its rate, or expands its programme of asset purchases. The Bank of Japan should follow the ECB.

Before the 2008 crisis, the “carry trade” – borrowing in a low-yielding currency to invest in a higher-yielding one – was a popular strategy. With rates flat everywhere it disappeared. Now there could be three years where the US is ahead of Europe on interest rates.

The yield gap between 5-year Treasuries and the equivalent Bund is now a record 1.82%, which should boost the dollar. This in turn will lead to devaluations – both forced and voluntary – in emerging markets currencies.

This would hurt companies that have borrowed in dollars, and capital flight could make refinancing for difficult for local currency borrowers.

In the US, a stronger dollar would reduce import prices (and hence inflation) and cut exports (hitting GDP growth). This is the same effect as monetary tightening, so further rate rises might not be needed.

Thos countries that have tightened rates since 2008 have been forced to cut later on.

It’s also possible that rate expectations are already in the price – the dollar has made big gains over the past year.

War on pensioners

Finally, in the Spectator, Mary Dejevsky reported on the war on pensioners.

Mary thinks that judging by the coverage of elderly, the media must be under the control of 25- to 45-year-olds who believe that their parents and grandparents have stolen their future.

There have been lots of headlines recently suggesting that pensioners now have higher incomes than workers.

It’s true that pensioners’ income has increased more than that of workers since the 2008 crash, but from a lower base.

There is still a gap of around 25% (£28K vs £21K), and the UK state pension remains much lower than in most developed countries.

Mary says that the media reports claimed that pensioners were better off than workers by making assumptions about their lower outgoing, particularly housing and children.

Offsetting this is the effect of low interest rates, which hurt savers (the old) but benefit borrowers (the young).

Mary also objects to the press bundling together the state pension (a contributory system) with benefits (which are free handouts).

There are rich pensioners, and always have been, but there are poor ones too.

Until next time.

Mike Rawson

Mike is the owner of 7 Circles, and a private investor living in London. He has been managing his own money for 40 years, with some success.